Copyright@http://lchipo.blogspot.com/

Follow us on facebook: https://www.facebook.com/LCH-Trading-Signal-103388431222067/

Open to apply: 09/03/2021

Close to apply: 16/03/2021

Listing date: 30/03/2021

Close to apply: 16/03/2021

Listing date: 30/03/2021

Share Capital

Market Cap: RM56.778mil

Total Shares: 283mil shares (Public apply: 14.1 mil, Company Insider/Miti/Private Placement/other: 61.036mil)

Market Cap: RM56.778mil

Total Shares: 283mil shares (Public apply: 14.1 mil, Company Insider/Miti/Private Placement/other: 61.036mil)

Industry (Revenue)

Flexidynamic: RM31.31mil

Polydamic Group Bhd: RM11.78mil

Ripcol Industries S/B: RM17.2mil

Business

Design, engineering, installation, & commissioning of glove chlorination system.

M’sia: 86.28%

Vietnam: 4.38%

Thailand: 8.74%

Indonesia: 0.07%

Sri Lanka 0.53%

Flexidynamic: RM31.31mil

Polydamic Group Bhd: RM11.78mil

Ripcol Industries S/B: RM17.2mil

Business

Design, engineering, installation, & commissioning of glove chlorination system.

M’sia: 86.28%

Vietnam: 4.38%

Thailand: 8.74%

Indonesia: 0.07%

Sri Lanka 0.53%

Fundamental

1.Market: Ace Market

2.Price: RM0.20 (EPS:RM0.0162)

3.P/E: PE12.35

4.ROE(Pro Forma III): 10.1%

5.ROE: 21.4%(2019), 24.8%(2018), 33%(2017)

6.Cash & fixed deposit after IPO: RM0.059 per shares

7.NA after IPO: RM0.12

8.Total debt to current asset after IPO: 0.708 (Debt: 31.832mil, Non-Current Asset: 21.998mil, Current asset: 44.976mil)

9.Dividend policy: Did not have formal dividend policy.

1.Market: Ace Market

2.Price: RM0.20 (EPS:RM0.0162)

3.P/E: PE12.35

4.ROE(Pro Forma III): 10.1%

5.ROE: 21.4%(2019), 24.8%(2018), 33%(2017)

6.Cash & fixed deposit after IPO: RM0.059 per shares

7.NA after IPO: RM0.12

8.Total debt to current asset after IPO: 0.708 (Debt: 31.832mil, Non-Current Asset: 21.998mil, Current asset: 44.976mil)

9.Dividend policy: Did not have formal dividend policy.

Past Financial Performance (Revenue, Earning Per shares)

2022: ***Remaining order book to be billed 2022 RM17.48mil

2021: ***order book to be billed Dec 2021 RM62.3mil

2020 (9mths): RM35.007 mil (EPS:0.0095)

2019: RM49.839 mil (EPS:0.0162)

2018: RM48.322 mil (EPS:0.0151)

2017: RM29.902 mil (EPS:0.0155)

2022: ***Remaining order book to be billed 2022 RM17.48mil

2021: ***order book to be billed Dec 2021 RM62.3mil

2020 (9mths): RM35.007 mil (EPS:0.0095)

2019: RM49.839 mil (EPS:0.0162)

2018: RM48.322 mil (EPS:0.0151)

2017: RM29.902 mil (EPS:0.0155)

Net Profit Margin

2020 (9mths): 7.62%

2019: 9.22%

2018: 9.14%

2017: 14.79%

2020 (9mths): 7.62%

2019: 9.22%

2018: 9.14%

2017: 14.79%

After IPO Sharesholding

Tan Kong Leong: 41.53%

Liew Heng Wei: 18.74%

Phitchaya Arsangku: 2.21%

Tan Kong Leong: 41.53%

Liew Heng Wei: 18.74%

Phitchaya Arsangku: 2.21%

Directors & Key Management Remuneration for FYE2021 (from gross profit 2019)

Total director remuneration: RM1.168mil or 8.37%

key management remuneration: RM0.4mil- 0.5mil or 2.87%-3.58%

total (max): RM1.668mil or 11.95%

Total director remuneration: RM1.168mil or 8.37%

key management remuneration: RM0.4mil- 0.5mil or 2.87%-3.58%

total (max): RM1.668mil or 11.95%

Use of fund

Repayment bank borrowing: 42.40% (purchase of 2 new factories 2019)

Renovation of new factories: 2.80%

Aquisition of machinery and equitment: 10.83%

Working capital: 24.03%

Listing Expenses: 19.94%

Repayment bank borrowing: 42.40% (purchase of 2 new factories 2019)

Renovation of new factories: 2.80%

Aquisition of machinery and equitment: 10.83%

Working capital: 24.03%

Listing Expenses: 19.94%

Good thing is:

1. Revenue increasing over 3 years.

2. Debt ratio not too dangerous level.

1. Revenue increasing over 3 years.

2. Debt ratio not too dangerous level.

3. Two purchased new factories, estimated renovation completed by Aug-Sep 2021,

4. Major customer Hartalega, contribute to Flexidyamic revenue 2017-2020 (range 31.78%-40.91%).

4. Major customer Hartalega, contribute to Flexidyamic revenue 2017-2020 (range 31.78%-40.91%).

The bad things:

1. Director fees & key managemnent remuneration already cost 11.95% from the company gross profit.

2. Net profit percentage dropping since 2017.

3. No fixed dividend policy.

4. ROE continue to fall over 3 years.

5. Industry player for top 2 & top 3 revenue RM17mil & RM11mil, showing this industry is not generate high revenue (possible less demand of the project needed).

1. Director fees & key managemnent remuneration already cost 11.95% from the company gross profit.

2. Net profit percentage dropping since 2017.

3. No fixed dividend policy.

4. ROE continue to fall over 3 years.

5. Industry player for top 2 & top 3 revenue RM17mil & RM11mil, showing this industry is not generate high revenue (possible less demand of the project needed).

Conclusions (Blogger is not wrote any recommendation & suggestion. All is personal opinion)

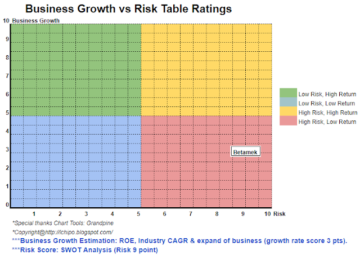

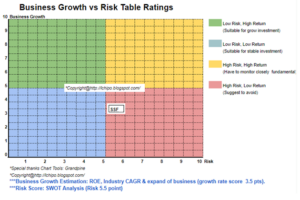

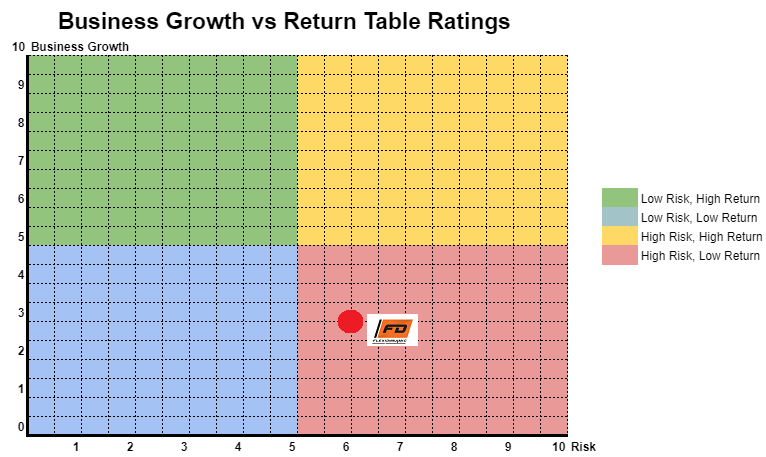

2020 is the high demand for glove, however did not see large improvement in net margin. The company secure RM62mil order book to be billed in 2021. We should see revenue able double at 2021 due to one off high demand order book due to the pandemic. After 2021, business revenue should back to normal phase. For business growth vs risk table please refer as below chart.

2020 is the high demand for glove, however did not see large improvement in net margin. The company secure RM62mil order book to be billed in 2021. We should see revenue able double at 2021 due to one off high demand order book due to the pandemic. After 2021, business revenue should back to normal phase. For business growth vs risk table please refer as below chart.

*Valuation is only personal opinion & view. Perception & forecast will change if any new quarter result release. Reader take their own risk & should do own homework to follow up every quarter result to adjust forecast of fundamental value of the company.

Source: http://lchipo.blogspot.com/2021/03/flexidynamic-holdings-berhad.html

- asset

- Bank

- Borrowing

- BP

- business

- capital

- Cash

- change

- company

- continue

- Current

- Debt

- Demand

- DID

- Director

- dividend

- Engineering

- expenses

- Fees

- financial

- follow

- Group

- Growth

- High

- homework

- HTTPS

- industries

- industry

- IPO

- Key

- large

- Level

- major

- management

- Market

- net

- Opinion

- order

- pandemic

- performance

- player

- policy

- price

- Pro

- Profit

- project

- public

- purchase

- range

- Reader

- revenue

- Risk

- Shares

- system

- top

- us

- value

- View

- years