Copyright@http://lchipo.blogspot.com/

Follow us on facebook: https://www.facebook.com/LCH-Trading-Signal-103388431222067/

Follow us on facebook: https://www.facebook.com/LCH-Trading-Signal-103388431222067/

***Important***Blogger is not wrote any recommendation & suggestion. All is personal opinion and reader should take their own risk in investment decision.

Open to apply: 30/08/2022

Close to apply: 12/09/2022

Balloting: 15/09/2022

Listing date: 27/09/2022

Close to apply: 12/09/2022

Balloting: 15/09/2022

Listing date: 27/09/2022

Share Capital

Market cap: RM192.6072 mil

Total Shares: 535.020mil shares

Industry CARG (2016-2021)

Frozen seafood sales volume in Asia Pacific CAGR: 1.7%

Frozen seafood sales value in Asia Pacific CAGR: 5.7%

Frozen seafood sales volume in Midlle East CAGR: 0.8%

Frozen seafood sales value in Middle East CAGR: 5.6%

Competitor Comparison (PAT %)

PT Resources: 9.68%

Piau Kee Live & Frozen Seafoods Sdn Bhd: 7.6%

Mayfresh Frozen Sea Product S/B: 5.33%

FisherGold S/B: -0.72%

Aiki Century Sdn Bhd: -10.77%

Market cap: RM192.6072 mil

Total Shares: 535.020mil shares

Industry CARG (2016-2021)

Frozen seafood sales volume in Asia Pacific CAGR: 1.7%

Frozen seafood sales value in Asia Pacific CAGR: 5.7%

Frozen seafood sales volume in Midlle East CAGR: 0.8%

Frozen seafood sales value in Middle East CAGR: 5.6%

Competitor Comparison (PAT %)

PT Resources: 9.68%

Piau Kee Live & Frozen Seafoods Sdn Bhd: 7.6%

Mayfresh Frozen Sea Product S/B: 5.33%

FisherGold S/B: -0.72%

Aiki Century Sdn Bhd: -10.77%

Business (FYE 2022)

Processing and trading of frozen seafood products, and trading of other products.

1. Frozen seafood (Wholesales): 83.4%

2. Frozen seafood (Retail): 8.7%

3. Retail trading of other products: 7.9%

Revenue by Geo

Msia: 42.8%

China: 44.2%

Saudi Arabia: 12.2%

others: 0.8%

Processing and trading of frozen seafood products, and trading of other products.

1. Frozen seafood (Wholesales): 83.4%

2. Frozen seafood (Retail): 8.7%

3. Retail trading of other products: 7.9%

Revenue by Geo

Msia: 42.8%

China: 44.2%

Saudi Arabia: 12.2%

others: 0.8%

Fundamental

1.Market: Ace Market

2.Price: RM0.36

3.P/E: 9.23 @ RM0.039 (we don't accept prospecture book pg19 use EPS before diluted to calculate PE).

4.ROE(Pro Forma III): 17.87%

5.ROE: 28.79%(FYE2022), 30.74%(FYE2021), 33.9%(FYE2020), 51.92%(FYE2019)

6.NA after IPO: RM0.22

7.Total debt to current asset after IPO: 0.5065 (Debt: 65.3267mil, Non-Current Asset: 54.4986mil, Current asset: 128.9688mil)

8.Dividend policy: 20% PAT dividend policy.

9. Shariah starus: -

1.Market: Ace Market

2.Price: RM0.36

3.P/E: 9.23 @ RM0.039 (we don't accept prospecture book pg19 use EPS before diluted to calculate PE).

4.ROE(Pro Forma III): 17.87%

5.ROE: 28.79%(FYE2022), 30.74%(FYE2021), 33.9%(FYE2020), 51.92%(FYE2019)

6.NA after IPO: RM0.22

7.Total debt to current asset after IPO: 0.5065 (Debt: 65.3267mil, Non-Current Asset: 54.4986mil, Current asset: 128.9688mil)

8.Dividend policy: 20% PAT dividend policy.

9. Shariah starus: -

Past Financial Performance (Revenue, Earning Per shares, PAT%)

2022 (FPE 30Apr): RM349.144 mil (Eps: 0.039),PAT: 6.0%

2021 (FYE 30Apr): RM186.447 mil (Eps: 0.030),PAT: 8.6%

2020 (FYE 30Apr): RM161.310 mil (Eps: 0.023),PAT: 7.6%

2019 (FYE 30Apr): RM116.396 mil (Eps: 0.028),PAT: 13.1%

Major customer (2022)

Fuzhou Ding Sheng Yuan Trade Co., Ltd: 15.4%

Fujian Jia He Yuan Aquatic Product Co., Ltd: 13.1%

KBT Food Supply Sdn Bhd: 10.7%

Fitkar For International Trading: 7.4%

China National Township: 6.6%

***total 53.2%

2022 (FPE 30Apr): RM349.144 mil (Eps: 0.039),PAT: 6.0%

2021 (FYE 30Apr): RM186.447 mil (Eps: 0.030),PAT: 8.6%

2020 (FYE 30Apr): RM161.310 mil (Eps: 0.023),PAT: 7.6%

2019 (FYE 30Apr): RM116.396 mil (Eps: 0.028),PAT: 13.1%

Major customer (2022)

Fuzhou Ding Sheng Yuan Trade Co., Ltd: 15.4%

Fujian Jia He Yuan Aquatic Product Co., Ltd: 13.1%

KBT Food Supply Sdn Bhd: 10.7%

Fitkar For International Trading: 7.4%

China National Township: 6.6%

***total 53.2%

Major Sharesholders

Heng Chang Hooi: 71%

Directors & Key Management Remuneration for FYE2023 (from Revenue & other income 2022)

Total director remuneration: RM0.643573 mil

key management remuneration: RM0.300 mil - 0.450mil

total (max): RM1.094 mil or 2.83%

Use of funds

1. Capital expenditure for new cold storage warehouse: 36.3%

2. Working capital: 55.9%

3. Listing Expenses: 7.8%

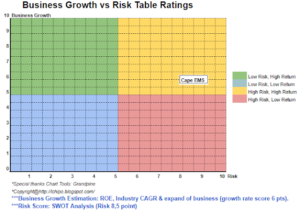

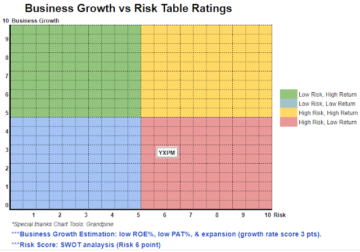

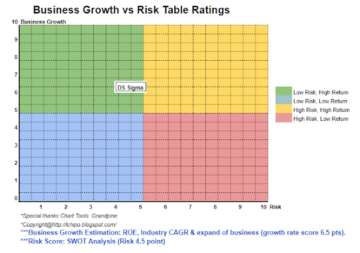

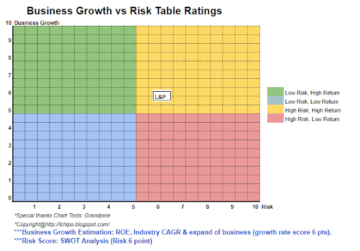

Conclusions (Blogger is not wrote any recommendation & suggestion. All is personal opinion and reader should take their own risk in investment decision)

Overall is a attractive IPO. The company is growing fast, however the industry they involve is low PAT margin profit, this part will limit the company growing opportunities in PAT% margin.

Overall is a attractive IPO. The company is growing fast, however the industry they involve is low PAT margin profit, this part will limit the company growing opportunities in PAT% margin.

*Valuation is only personal opinion & view. Perception & forecast will change if any new quarter result release. Reader take their own risk & should do own homework to follow up every quarter result to adjust forecast of fundamental value of the company.

- SEO Powered Content & PR Distribution. Get Amplified Today.

- Platoblockchain. Web3 Metaverse Intelligence. Knowledge Amplified. Access Here.

- Source: http://lchipo.blogspot.com/2022/08/pt-resources-holdings-berhad.html

- 1

- 10

- 2022

- 28

- 7

- 9

- a

- Accept

- After

- All

- and

- Apply

- asia

- asia pacific

- asset

- attractive

- before

- book

- CAGR

- cap

- capital

- Center

- Century

- change

- clear

- Cold Storage

- color

- company

- comparison

- Current

- customer

- Date

- Debt

- decision

- Director

- dividend

- Earning

- East

- Ether (ETH)

- expenses

- FAST

- financial

- financial performance

- follow

- food

- food supply

- Forecast

- from

- frozen

- fundamental

- Growing

- Holdings

- homework

- However

- HTTPS

- in

- Income

- industry

- International

- investment

- involve

- IPO

- Key

- LIMIT

- listing

- live

- Low

- Ltd

- management

- Margin

- Market

- max

- Middle

- Middle East

- National

- New

- Opinion

- opportunities

- Other

- own

- Pacific

- part

- perception

- performance

- personal

- plato

- Plato Data Intelligence

- PlatoData

- policy

- price

- Pro

- Product

- Products

- Profit

- Quarter

- Reader

- Recommendation

- Red

- release

- remuneration

- Resources

- result

- retail

- Retail Trading

- revenue

- Risk

- sales

- Sales Volume

- SEA

- seafood

- Shares

- Shariah

- should

- storage

- supply

- Take

- The

- their

- to

- Total

- trade

- Trading

- us

- use

- value

- View

- volume

- Warehouse

- will

- working

- Yuan

- zephyrnet