Copyright@http://lchipo.blogspot.com/

Follow us on facebook: https://www.facebook.com/LCH-Trading-Signal-103388431222067/

Follow us on facebook: https://www.facebook.com/LCH-Trading-Signal-103388431222067/

***Important***Blogger is not wrote any recommendation & suggestion. All is personal

opinion and reader should take their own risk in investment decision.

opinion and reader should take their own risk in investment decision.

Open to apply: 16/02/2023

Close to apply: 27/02/2023

Price determination: 27/02/2023

Balloting: 01/03/2023

Listing date: 10/03/2023

Share Capital

Market cap: RM830.7mil

Total Shares: 923mil shares

Market cap: RM830.7mil

Total Shares: 923mil shares

Industry CARG (2017-2021)

Global exports of E&E products: 7.5%

Global import of E&E products: 7.2%

Industry competitors comparison (net profit%)

Cape Group: 7.6% (PE25.28 is use FYE2022 PAT)

JHM: 11.5% (PE14.66)

Plexus Manufacturing S/B: 11.1%

Benchmark Electronics (M) S/B: 12.8%

NationGate Holdings Bhd: 7.8% (PE21.22)

SKP Resources Bhd: 7.5% (PE14.34)

P.I.E. Industrial Bhd: 5.9% (PE18.62)

Others: -4.6% to 5.7%

Business (FYE 2021)

EMS provider on contract manufacturing services for end-to-end manufacturing services which entail parts and components sourcing and procurement, production, assembly, testing, packaging up to direct shipment fulfilment

Revenue by Segment

1. Industrial electronic products: 58.8%

2. Consumer electronic products: 38.0%

3. Supporting services: 3.2%

Revenue by Geo

1. Asia Pacific: 37.8% (Singapore: 30.7%)

2. USA: 55.1%

3. Europe: 7.1%

1. Industrial electronic products: 58.8%

2. Consumer electronic products: 38.0%

3. Supporting services: 3.2%

Revenue by Geo

1. Asia Pacific: 37.8% (Singapore: 30.7%)

2. USA: 55.1%

3. Europe: 7.1%

Fundamental

1.Market: Main Market

2.Price: RM0.90 (will follow final insti price@27/02/2023)

3.P/E: 25.28 @ RM0.0285 (prospecture pg27 use FYE21 PE31.6, we use EPS RM0.0356 @ FYE22)

4.ROE(Pro Forma III): 10.06%

5.ROE: 18.07%(FYE2022), 15.49%(FYE2021), 24.86%(FYE2020), 18.17%(FYE2019)

6.Net asset: RM0.35

7.Total debt to current asset after IPO: 0.75 (Debt: 282.094mil, Non-Current Asset: 230.615mil, Current asset: 377.704mil)

8.Dividend policy: 30% PAT dividend policy.

9. Shariah status: -

Past Financial Performance (Revenue, Earning Per shares, PAT%)

2022 (FPE 30sep, 6mths): RM319.750 mil (Eps: 0.0267),PAT: 7.7%

2021 (FYE 31Dec): RM344.334 mil (Eps: 0.0285),PAT: 7.6%

2020 (FYE 31Dec): RM168.261 mil (Eps: 0.0219),PAT: 12.0%

2019 (FYE 31Dec): RM43.157 mil (Eps: 0.0041),PAT: 8.8%

Operating cashflow (before tax) vs PBT

2022: 14.66% (trade receivable: RM122mil)

2021: 135% (trade receivable: RM82mil)

2020: -7.74% (trade receivable: RM80mil)

2019: 405% (trade receivable:RM54mil)

Major customer (2022)

Customer A (USA): 27.1%

Tastar Electronics (SG): 19.8%

Airspan group of companies: (USA & UK): 18.4%

NextCentury (USA): 12.6%

K&Q (SG): 10.9%

***total 88.8%

Major Sharesholders

Tee Kim Chin: 40.6% (direct)

Tee Kim Yok: 13.8% (direct)

Fortress: 16.6% (direct)

Directors & Key Management Remuneration for FYE2022 (from Revenue & other income 2021)

Total director remuneration: RM5.098mil

key management remuneration: RM1.250mil - RM1.450mil

total (max): RM7.998mil or 19.09%

Use of funds

1. Construction of New Senai 226 Warehouse and installation of automated storage facilities: 34.1%

2. Setting-up of new cleanroom facility and purchase of new automated production lines for EMS operations: 40.3%

3. Installation of energy saving cooling system: 2.4%

4. Purchase of new machinery and equipment for die cast manufacturing related services: 3%

5. Working capital: 13.2%

5. Listing Expenses: 7.0%

Conclusions (Blogger is not wrote any recommendation & suggestion. All is personal opinion and reader should take their own risk in investment decision)

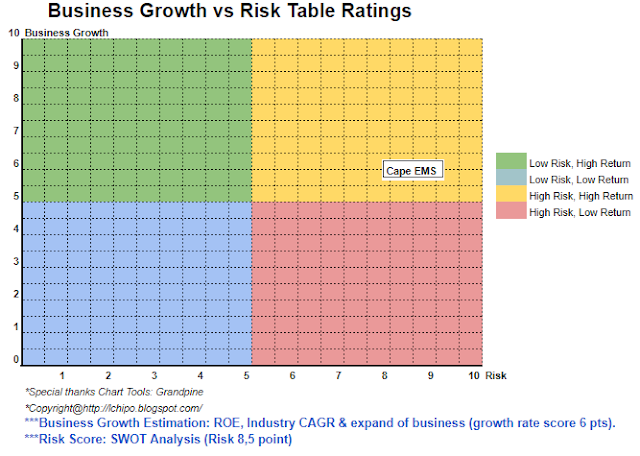

Overall slightly expensive IPO with the PE above industry average. However, with the new production line will encourage the grow of their revenue.

*Valuation is only personal opinion & view. Perception & forecast will change if any new quarter

result release. Reader take their own risk & should do own homework to follow up every quarter

result to adjust forecast of fundamental value of the company.

- SEO Powered Content & PR Distribution. Get Amplified Today.

- Platoblockchain. Web3 Metaverse Intelligence. Knowledge Amplified. Access Here.

- Source: http://lchipo.blogspot.com/2023/02/cape-ems-berhad.html

- 10

- 11

- 2021

- 2022

- 28

- 7

- a

- above

- After

- All

- and

- Apply

- asia

- asia pacific

- Assembly

- asset

- Automated

- average

- before

- cap

- capital

- Center

- change

- chin

- clear

- color

- Companies

- company

- comparison

- competitors

- components

- construction

- consumer

- contract

- cooling system

- Current

- customer

- Date

- Debt

- decision

- determination

- Die

- direct

- Director

- dividend

- Earning

- Electronic

- Electronics

- encourage

- end-to-end

- energy

- equipment

- Ether (ETH)

- Europe

- Every

- expenses

- expensive

- exports

- facilities

- Facility

- final

- financial

- financial performance

- follow

- Forecast

- from

- fundamental

- Group

- Grow

- Holdings

- homework

- However

- HTTPS

- import

- in

- Income

- industrial

- industry

- investment

- IPO

- Key

- Kim

- Line

- lines

- listing

- machinery

- Main

- management

- manufacturing

- Market

- max

- net

- New

- Operations

- Opinion

- Other

- own

- Pacific

- packaging

- parts

- perception

- performance

- personal

- plato

- Plato Data Intelligence

- PlatoData

- policy

- price

- Pro

- Production

- Products

- provider

- purchase

- Reader

- Recommendation

- Red

- related

- release

- remuneration

- Resources

- revenue

- Risk

- saving

- Services

- SG

- Shares

- Shariah

- should

- Singapore

- Sourcing

- Status

- storage

- Supporting

- system

- Take

- tax

- Testing

- The

- their

- to

- Total

- trade

- Uk

- us

- USA

- use

- value

- View

- Warehouse

- which

- will

- working

- zephyrnet