Copyright@http://lchipo.blogspot.com/

Follow us on facebook: https://www.facebook.com/LCH-Trading-Signal-103388431222067/

***Important***Blogger is not wrote any recommendation & suggestion. All is personal

opinion and reader should take their own risk in investment decision.

Open to apply: 9 May 2023

Close to apply: 15 May 2023

Balloting: 18 May 2023

Listing date: 29 May 2023

Follow us on facebook: https://www.facebook.com/LCH-Trading-Signal-103388431222067/

***Important***Blogger is not wrote any recommendation & suggestion. All is personal

opinion and reader should take their own risk in investment decision.

Open to apply: 9 May 2023

Close to apply: 15 May 2023

Balloting: 18 May 2023

Listing date: 29 May 2023

Share Capital

Market cap: RM202.008 mil

Total Shares: 531.6 mil shares

Industry CARG (2017-2022)

Networking solutions industry size in Malaysia: 23.1%

Cybersecurity solutions industry size in Malaysia: 13.8%

Industry competitors comparison (PAT%)

Cloudpoint: 14.5% (PE14.5)

Infoline: 16.6% (PE32)

Sarawak Information Systems Sdn Bhd: 15.2%

Bridgenet Solutions Sdn Bhd: 7.9%

NTT Malaysia Solutions Sdn Bhd: 7.5%

Mesiniaga Berhad: 2.3% (PE12.91)

Others companies: 0.3% to 6.3% (pg154)

Dataprep Holdings Berhad: Losses

Business (FYE 2022)

IT solutions comprising enterprise and data centre networking, and cybersecurity solutions as well as professional IT services.

Provide services to companies in the financial services, insurance, telecommunications industries and other technology service providers

Fundamental

1.Market: Ace Market

2.Price: RM0.38

3.Forecast P/E: 15.38 @ RM0.0247

4.ROE(Pro Forma III): 63.24%

5.ROE: 65.49%(FYE2021), 39.01%(FYE2020), 31.05%(FYE2019)

6.Net asset: RM0.27

7.Total debt to current asset IPO: 0.48 (Debt: 45.782mil, Non-Current Asset: 9.075mil, Current asset: 95.331mil)

8.Dividend policy: no formal dividend policy.

9. Shariah status: Yes

Past Financial Performance (Revenue, Earning Per shares, PAT%)

2022 (FYE 31Dec): RM90.595 mil (Eps: 0.0247),PAT: 14.5%

2021 (FYE 31Dec): RM59.541 mil (Eps: 0.0193),PAT: 17.2%

2020 (FYE 31Dec): RM51.230 mil (Eps: 0.0157),PAT: 16.3%

2019 (FYE 31Dec): RM50.634 mil (Eps: 0.0123),PAT: 12.9%

Order Book

One-off project-based income model

2025: RM-

2024: RM9.739 mil

2023: RM32.073 mil

Recurring income model

2025: RM7.681mil

2024: RM8.950mil

2023: RM6.893 mil

Operating cashflow vs PBT

2022: 49.40%

2021: 24.17%

2020: 57.05%

2019: 77.08%

Major customer (2022)

Customer G: 35.3% (financial services industry)

Customer D: 28.5% (financial services industry)

Customer B: 8,3% (financial services industry)

Customer F: 7.8% (telecommunication industry)

Customer H: 3.4% (financial services industry)

***total 83.3%

Major Sharesholders

Era Jasakita: 52% (direct)

Choong Wai Hoong: 8.1% (direct), 52% (indirect)

Yew Choong Cheong: 8.1% (direct), 52% (indirect)

Directors & Key Management Remuneration for FYE2023

(from Revenue & other income 2022)

Total director remuneration: RM1.869mil

key management remuneration: RM0.75mil – RM0.85mil

total (max): RM2.719 mil or 11%

Use of funds

Business expansion: 32.9%

Relocation of corporate office: 19.3%

Working capital requirements: 39.1%

Estimated listing expenses: 8.7%

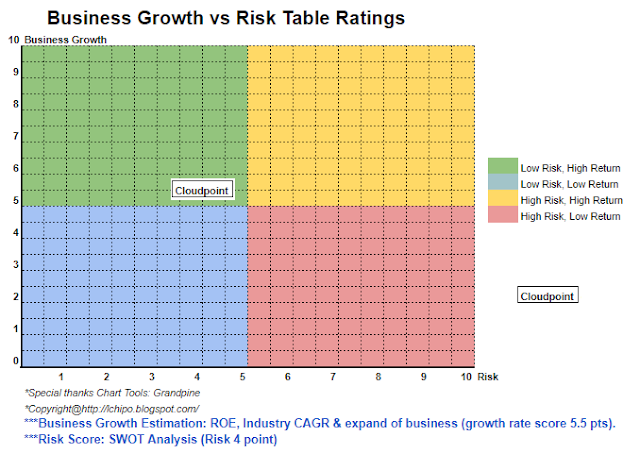

Conclusions (Blogger is not wrote any recommendation & suggestion. All is personal opinion and reader should take their own risk in investment decision)

Overall is a good IPO with discount value.

*Valuation is only personal opinion & view. Perception & forecast will change if any new quarter result release. Reader take their own risk & should do own homework to follow up every quarter result to adjust forecast of fundamental value of the company.

Overall is a good IPO with discount value.

*Valuation is only personal opinion & view. Perception & forecast will change if any new quarter result release. Reader take their own risk & should do own homework to follow up every quarter result to adjust forecast of fundamental value of the company.

- SEO Powered Content & PR Distribution. Get Amplified Today.

- PlatoAiStream. Web3 Data Intelligence. Knowledge Amplified. Access Here.

- Minting the Future w Adryenn Ashley. Access Here.

- Buy and Sell Shares in PRE-IPO Companies with PREIPO®. Access Here.

- Source: http://lchipo.blogspot.com/2023/05/cloudpoint-techology-berhad.html

- :is

- :not

- $UP

- 1

- 12

- 13

- 14

- 15%

- 2022

- 23

- 24

- 28

- 39

- 49

- 7

- 710

- 77

- 8

- 9

- 91

- a

- All

- and

- any

- Apply

- AS

- asset

- both

- cap

- capital

- capital requirements

- Center

- centre

- change

- clear

- color

- Companies

- company

- comparison

- competitors

- comprising

- Corporate

- Current

- customer

- Cybersecurity

- data

- data centre

- Date

- Debt

- decision

- direct

- Director

- Discount

- dividend

- do

- Earning

- Enterprise

- Ether (ETH)

- Every

- expansion

- expenses

- financial

- financial performance

- financial services

- follow

- For

- Forecast

- formal

- from

- fundamental

- good

- Holdings

- homework

- HTTPS

- if

- in

- Income

- industries

- industry

- information

- Information Systems

- insurance

- investment

- IPO

- IT

- Key

- left

- listing

- Malaysia

- management

- Market

- max

- May..

- net

- networking

- New

- no

- of

- Office

- on

- only

- Opinion

- or

- Other

- own

- perception

- performance

- personal

- plato

- Plato Data Intelligence

- PlatoData

- policy

- price

- Pro

- professional

- project-based

- Quarter

- Reader

- Recommendation

- Red

- release

- remuneration

- Requirements

- result

- revenue

- Risk

- service

- Services

- Shares

- Shariah

- should

- Size

- Solutions

- Status

- Systems

- Take

- Technology

- telecommunication

- telecommunications

- The

- their

- to

- Total

- us

- value

- View

- vs

- WELL

- will

- with

- zephyrnet