Copyright@http://lchipo.blogspot.com/

Follow us on facebook: https://www.facebook.com/LCH-Trading-Signal-103388431222067/

Follow us on facebook: https://www.facebook.com/LCH-Trading-Signal-103388431222067/

***Important***Blogger is not wrote any recommendation & suggestion. All is personal opinion and reader should take their own risk in investment decision.

Open to apply: 13/12/2022

Close to apply: 21/12/2022

Balloting: 27/12/2022

Listing date: 06/01/2023

Close to apply: 21/12/2022

Balloting: 27/12/2022

Listing date: 06/01/2023

Share Capital

Market cap: 264mil (will depend on final IPO price)

Total Shares: 480mil shares

Industry CARG (2017-2021)

Consumption value of paper cartons: CARG 10.6%

Consumption value of plastic packaging: CARG 11.3%

Competitors comparison (Net profit margin, PE)

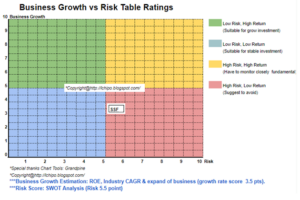

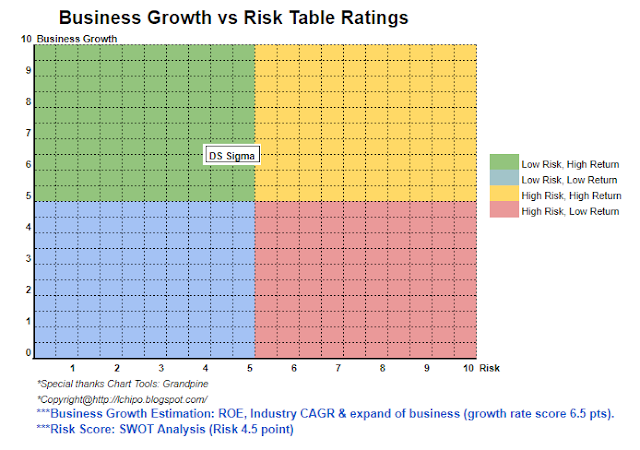

1. DS Sigma Group: 17.7% (PE12.56)

2. Public Packages Holdings Bhd: 12% (PE4.56)

3. Jishan Bhd: 10.8% (PE6.01)

4. HPP Holdings Bhd: 9.9% (PE15.6)

5. Magni-Tech Industries Bhd: 9.3% (PE7.91)

6. Master-Pack Group Bhd: 9.4% (PE7.25%)

7. Others (9company): 8.9% to -19%

Business (FYE 2022)

Manufacturing of corrugated paper packaging products including cartons, protective packaging and paper pallets.

DS Manufacturing: Manufacture of corrugated paper packaging products.

DS Packaging: Manufacture of corrugated paper packaging products and supply of protective packaging products.

Kaisung: Supply of protective packaging products.

Manufacturing of corrugated paper packaging products including cartons, protective packaging and paper pallets.

DS Manufacturing: Manufacture of corrugated paper packaging products.

DS Packaging: Manufacture of corrugated paper packaging products and supply of protective packaging products.

Kaisung: Supply of protective packaging products.

Fundamental

1.Market: Ace Market

2.Price: RM0.55

3.P/E: 12.56 @ RM0.0438

4.ROE(Pro Forma III): 22.36%

5.ROE: 42.69% (FYE2022), 73.27%(FYE2021), 43.51%(FYE2020), 74.72%(FYE2019)

6.NA after IPO: RM0.20

7.Total debt to current asset after IPO: 0.3829 (Debt: 23.204mil, Non-Current Asset: 58.647mil, Current asset: 60.596mil)

8.Dividend policy: no formal dividend policy.

9. Shariah starus: Yes

1.Market: Ace Market

2.Price: RM0.55

3.P/E: 12.56 @ RM0.0438

4.ROE(Pro Forma III): 22.36%

5.ROE: 42.69% (FYE2022), 73.27%(FYE2021), 43.51%(FYE2020), 74.72%(FYE2019)

6.NA after IPO: RM0.20

7.Total debt to current asset after IPO: 0.3829 (Debt: 23.204mil, Non-Current Asset: 58.647mil, Current asset: 60.596mil)

8.Dividend policy: no formal dividend policy.

9. Shariah starus: Yes

Past Financial Performance (Revenue, Earning Per shares, PAT%)

2022 (FYE 30Jun): RM121.218 mil (Eps: 0.0438),PAT: 17.71%

2021 (FYE 30Jun): RM127.858 mil (Eps: 0.0423),PAT: 16.52%

2020 (FYE 30Jun): RM85.891 mil (Eps: 0.0202),PAT: 11.55%

2019 (FYE 30Jun): RM105.682 mil (Eps: 0.0312),PAT: 14.13%

2022 (FYE 30Jun): RM121.218 mil (Eps: 0.0438),PAT: 17.71%

2021 (FYE 30Jun): RM127.858 mil (Eps: 0.0423),PAT: 16.52%

2020 (FYE 30Jun): RM85.891 mil (Eps: 0.0202),PAT: 11.55%

2019 (FYE 30Jun): RM105.682 mil (Eps: 0.0312),PAT: 14.13%

Operating cashflow vs PBT

2022: 94.09%

2021: 66.14%

2020: 70.23%

2019: 86.71%

Major customer (2022)

1. Samsung Electronics: 20%

2. SOEM (Sony): 18.86%

3. SSCSM (Sony): 17.8%

4. PAACM (Panasonic): 14.97%

5. YH Precision (M) Sdn Bhd: 5.11%

***total 75.64%

Major Sharesholders

Lucille Teoh Soo Lien: 61% (indirect)

Beh Seng Lee: 61% (indirect)

DS Kaizen: 61% (direct)

Directors & Key Management Remuneration for FYE2023 (from Revenue & other income 2022)

Total director remuneration: RM7.454mil

key management remuneration: RM0.90 mil - RM1.10 mil

total (max): RM8.554mil or 19.89%

Use of funds

1. Expansion of operations to Penang: 2.39%

2. Establishment of Klang Factory 2: 31.91%

3. Purchase of Automated and robotic packing machines: 14.16%

4. Purchase of Honeycomb board machines: 6.38%

5. Purchase of 6-colour flexographic printing machine: 11.37%

6. Establish packaging design and innovation centre: 2.27%

7. Repayment of bank borrowings: 11.96%

8. Working capital: 10.79%

9. Listing Expenses: 8.77%

Conclusions (Blogger is not wrote any recommendation & suggestion. All is personal opinion and reader should take their own risk in investment decision)

Overall is a good IPO. Just worries part is IPO PE offer is above the average of the same industry competitors. In other meaning is good IPO with no discount offer compare to competitors.

Overall is a good IPO. Just worries part is IPO PE offer is above the average of the same industry competitors. In other meaning is good IPO with no discount offer compare to competitors.

*Valuation is only personal opinion & view. Perception & forecast will change if any new quarter result release. Reader take their own risk & should do own homework to follow up every quarter result to adjust forecast of fundamental value of the company.

- SEO Powered Content & PR Distribution. Get Amplified Today.

- Platoblockchain. Web3 Metaverse Intelligence. Knowledge Amplified. Access Here.

- Source: http://lchipo.blogspot.com/2022/12/ds-sigma-holdings-berhad.html

- 1

- 10

- 11

- 2022

- 70

- 9

- a

- above

- After

- All

- and

- Apply

- asset

- Automated

- average

- Bank

- board

- cap

- capital

- Center

- centre

- change

- clear

- color

- company

- compare

- comparison

- competitors

- Current

- customer

- Date

- Debt

- decision

- Design

- direct

- Director

- Discount

- Earning

- Electronics

- establish

- establishment

- Ether (ETH)

- expansion

- expenses

- factory

- final

- financial

- financial performance

- follow

- Forecast

- formal

- from

- fundamental

- good

- Group

- Holdings

- HTTPS

- in

- In other

- Including

- Income

- industries

- industry

- Innovation

- investment

- IPO

- Key

- Lee

- listing

- machine

- Machines

- management

- manufacturing

- Margin

- Market

- max

- meaning

- net

- New

- offer

- Operations

- Opinion

- Other

- Others

- own

- packages

- packaging

- Paper

- part

- perception

- performance

- personal

- plastic

- plato

- Plato Data Intelligence

- PlatoData

- policy

- Precision

- price

- Pro

- Products

- Profit

- Protective

- public

- purchase

- Quarter

- Reader

- Recommendation

- Red

- release

- remuneration

- repayment

- result

- revenue

- Risk

- same

- Samsung

- Shares

- Shariah

- should

- Sigma

- Sony

- supply

- Take

- The

- their

- to

- Total

- us

- value

- View

- will

- working

- zephyrnet