Copyright@http://lchipo.blogspot.com/

Follow us on facebook: https://www.facebook.com/LCH-Trading-Signal-103388431222067/

Follow us on facebook: https://www.facebook.com/LCH-Trading-Signal-103388431222067/

***Important***Blogger is not wrote any recommendation & suggestion. All is personal opinion and reader should take their own risk in investment decision

Open to apply: 14/06/2022

Close to apply: 24/06/2022

Balloting: 29/06/2022

Listing date: 07/07/2022

Close to apply: 24/06/2022

Balloting: 29/06/2022

Listing date: 07/07/2022

Share Capital

Market cap: RM389.220 mil

Total Shares: 518.960 mil shares

Industry & Competitor (PAT%)

Export volume of block rubber (Malaysia 2018-2021): 1.03-1.09 mil MTS

Seng Fong Group: 4.51%

Tiong Huat Rubber: 4.27%

FGV rubber: -1.93%

Seng Hin Rubber: 1.62%

MARDEC Processing: -7.45%

Hock Hin Rubber: 0.52%

Others: -1.54% to 1.72%

Business (2021)

Processing of cup lump rubber into block rubber

Revenue by Geo

China: 46.5%

HK: 20.3%

S'pore: 31%

Taiwan: 0.8%

Others: 1.4%

Fundamental

1.Market: Main Market

2.Price: RM0.75

3.P/E: 11.2 @ EPS0.067

4.ROE(Pro Forma III): 22.99% (ProForma)

5.ROE: 39.41%(FYE2021), 16.8%(FYE2020), 14.5%(FYE2019)

6.NA after IPO: RM0.45

7.Total debt to current asset after IPO: 0.409 (Debt: 108.203mil, Non-Current Asset: 50.386mil, Current asset: 264.387mil)

8.Dividend policy: 50% PAT dividend policy.

Past Financial Performance (Revenue, Earning Per shares, PAT%)

2021 (FPE 31Dec, 6mths): RM400.490 mil (Eps: 0.0350),PAT: 4.5%

2021 (FYE 30Jun): RM768.177 mil (Eps: 0.0670),PAT: 4.5%

2020 (FYE 30Jun): RM616.435 mil (Eps: 0.0260),PAT: 2.1%

2019 (FYE 30Jun): RM636.834 mil (Eps: 0.0280),PAT: 2.3%

Major customer (2021)

1. R1 International Pte Ltd : 29.3%

2. Jiangsu General Science Technology Co., Ltd: 21.7%

3. Shandong Xinghongyuan Tyre Co.Ltd: 15.2%

4. Westwater Group: 14.1%

5. Wanli Groupp: 10.7%

total top 5 customer is 91% (2021)

Major Sharesholders:

Sumber Panji: 59.3% (Direct)

Er Hock Lai: 59.3% (Indirect)

Er Tak Bin: (Direct)

Directors & Key Management Remuneration for FYE2022 (from Revenue & other income 2021)

Total director remuneration: RM3.374 mil

key management remuneration: RM0.60 mil - RM0.80 mil

total (max): RM4.174 mil or 0.565%

Use of fund

1. Working capital: 28.9%

2. Repayment bank borrowing: 55.6%

3. Install of Biomass system: 9.2%

6. Listing Expenses: 6.3%

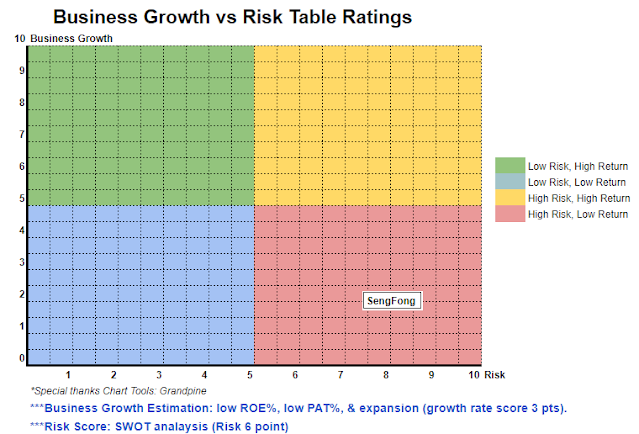

Conclusions (Blogger is not wrote any recommendation & suggestion. All is personal opinion and reader should take their own risk in investment decision)

Overall is not a good IPO. More info refer to the SWOT analysis above.

Overall is not a good IPO. More info refer to the SWOT analysis above.

*Valuation is only personal opinion & view. Perception & forecast will change if any new quarter result release. Reader take their own risk & should do own homework to follow up every quarter result to adjust forecast of fundamental value of the company.

- SEO Powered Content & PR Distribution. Get Amplified Today.

- Platoblockchain. Web3 Metaverse Intelligence. Knowledge Amplified. Access Here.

- Source: http://lchipo.blogspot.com/2022/06/seng-fong-holdings-berhad.html

- 1

- 10

- 11

- 2021

- 28

- 39

- 9

- a

- above

- After

- All

- analysis

- and

- Apply

- asset

- Bank

- biomass

- Block

- Borrowing

- cap

- capital

- Center

- change

- clear

- color

- company

- competitor

- Cup

- Current

- customer

- Date

- Debt

- decision

- direct

- Director

- dividend

- Earning

- Ether (ETH)

- expenses

- financial

- financial performance

- follow

- Forecast

- from

- fundamental

- General

- good

- Group

- Holdings

- homework

- HTTPS

- in

- Income

- info

- install

- International

- investment

- IPO

- Key

- listing

- Ltd

- Main

- Malaysia

- management

- Market

- max

- more

- New

- Opinion

- Other

- own

- perception

- performance

- personal

- plato

- Plato Data Intelligence

- PlatoData

- policy

- price

- Pro

- processing

- Quarter

- Reader

- Recommendation

- Red

- release

- remuneration

- repayment

- result

- revenue

- Risk

- rubber

- Science

- Shares

- should

- system

- Take

- Technology

- The

- their

- to

- top

- top 5

- Total

- us

- value

- View

- volume

- will

- working

- zephyrnet