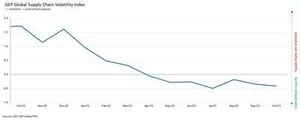

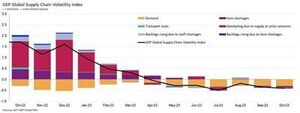

The GEP Global Supply Chain Volatility Index — the indicator tracking demand conditions, shortages, transportation costs, inventories and backlogs based on a monthly survey of 27,000 businesses — decreased again in October to -0.41, from -0.35 in September, indicating a 7th successive month of rising spare capacity across the world’s supply chains.

Additionally, the extent to which supplier capacity went underutilised was even greater than in September and August. Coupled with October’s downturn in demand for raw materials, components and commodities, this shows rising slack in global supply chains.

“While the shrinking of global suppliers’ order books is not worsening, there are no signs of improvement,” explained Jamie Ogilvie-Smals, vice president, consulting, GEP. “The notable increase in supplier capacity in Asia, which was driven by China, provides global manufacturers with greater leverage to drive down prices and inventories in 2024.”

A key finding from October’s report was the strongest rise in excess capacity across Asian supply chains since June 2020. Sustained weakness in demand, coupled with falling pressures on factories in Asia, indicates that the global manufacturing recession has further to run. With the exception of India, which continues to perform strongly, large economies in the region, such as Japan and China, are losing momentum.

Suppliers in Europe continue to report the largest level of spare capacity. In fact, the lower levels in GEP’s supply chain index for the continent have only been seen during the global financial crisis between 2008 and 2009. They highlight sustained weakness in economic conditions across the continent. Western Europe, particularly Germany’s manufacturing industry, is a key driver behind the region’s deterioration.

Відносно яскравою плямою є Північна Америка, де ланцюжки поставок мають надлишок потужностей, але набагато меншим, ніж деінде, оскільки економіка США продовжує демонструвати свою стійкість, на відміну від Європи.

Жовтень 2023 Ключові висновки

Demand: Demand for raw materials, components and commodities remains depressed, although the downturn seems to have stabilised. There are still no signs of conditions improving, however, as global purchasing activity fell again in October at a pace similar to what we’ve seen since around mid-year.

Demand: Demand for raw materials, components and commodities remains depressed, although the downturn seems to have stabilised. There are still no signs of conditions improving, however, as global purchasing activity fell again in October at a pace similar to what we’ve seen since around mid-year.- Товарні запаси: в умовах падіння попиту наші дані показують ще один місяць скорочення запасів глобальними компаніями, що свідчить про зусилля щодо збереження грошових потоків.

- Дефіцит матеріалів: звіти про дефіцит товарів залишаються на найнижчому рівні з січня 2020 року.

- Labour shortages: Shortages of workers are not impacting global manufacturers’ capacity to produce, with reports of backlogs due to inadequate labour supply running at historically typical levels.

- Transportation: Global transportation costs held steady with September’s level, although oil prices have declined in recent weeks.

Нестабільність регіонального ланцюжка поставок

-

Північна Америка: індекс впав до -0.34 з -0.30. Це залишається набагато м’якшим, ніж середній світовий показник, і продовжує припускати США. економіка готова до м'якої посадки.

- Європа: індекс піднявся до -0.90 з -1.01, але все ще залишається на рівні, який свідчить про значну крихкість економіки.

- ВЕЛИКОБРИТАНІЯ: Індекс трохи підвищився до -0.93 з -0.98. Тим не менш, дані вказують на значне зростання надлишкових потужностей у постачальників на ринки Великобританії.

- Asia: Notably, the index dropped to -0.38, from -0.20, highlighting the biggest rise in spare supplier capacity in Asia since June 2020 as the region’s resilience fades.

- Розповсюдження контенту та PR на основі SEO. Отримайте посилення сьогодні.

- PlatoData.Network Vertical Generative Ai. Додайте собі сили. Доступ тут.

- PlatoAiStream. Web3 Intelligence. Розширення знань. Доступ тут.

- ПлатонЕСГ. вуглець, CleanTech, Енергія, Навколишнє середовище, Сонячна, Поводження з відходами. Доступ тут.

- PlatoHealth. Розвідка про біотехнології та клінічні випробування. Доступ тут.

- джерело: https://www.logisticsit.com/articles/2023/11/21/supply-chains-worldwide-remain-significantly-underutilised-gep-global-supply-chain-volatility-index

- : має

- :є

- : ні

- :де

- 000

- 01

- 121

- 20

- 2008

- 2020

- 2023

- 2024

- 27

- 30

- 300

- 35%

- 41

- 7th

- 90

- 98

- a

- через

- діяльність

- знову

- хоча

- Америка

- та

- Інший

- ЕСТЬ

- навколо

- AS

- Азія

- азіатський

- At

- Серпня

- середній

- заснований

- було

- за

- між

- найбільший

- книги

- Яскраво

- підприємства

- але

- by

- потужність

- ланцюг

- ланцюга

- Китай

- Commodities

- Компоненти

- Умови

- значний

- консалтинг

- континент

- продовжувати

- триває

- контрастність

- витрати

- з'єднаний

- криза

- дані

- знизився

- Попит

- дисплей

- вниз

- ЗНИЖЕННЯ

- управляти

- керований

- водій

- впав

- два

- під час

- Економічний

- Економічні умови

- економія

- економіка

- зусилля

- в іншому місці

- Ефір (ETH)

- Європа

- Навіть

- виняток

- надлишок

- пояснені

- ступінь

- факт

- заводи

- Зникає

- Падіння

- фінансовий

- фінансова криза

- виявлення

- для

- крихкість

- від

- далі

- Німеччина

- Глобальний

- глобальні фінансові

- Глобальна фінансова криза

- великий

- Мати

- Герой

- вище

- Виділіть

- виділивши

- історично

- Однак

- HTTPS

- впливає

- поліпшення

- поліпшення

- in

- Augmenter

- індекс

- Індію

- вказує

- вказуючи

- показовий

- індикатор

- промисловість

- ЙОГО

- Джеймі

- січня

- Japan

- JPG

- червень

- ключ

- Праці

- посадка

- великий

- найбільших

- менше

- рівень

- рівні

- Важіль

- програш

- знизити

- найнижчий

- Виробники

- виробництво

- обробної промисловості

- ринки

- Матеріали

- Імпульс

- місяць

- щомісячно

- багато

- немає

- На північ

- Північна Америка

- Помітний

- особливо

- жовтень

- of

- Нафта

- on

- тільки

- порядок

- книги замовлень

- наші

- алюр

- особливо

- виконувати

- plato

- Інформація про дані Платона

- PlatoData

- точка

- готовий

- збереження

- президент

- ціни

- виробляти

- забезпечує

- покупка

- Сировина

- останній

- спад

- регіон

- відносний

- залишатися

- залишається

- звітом

- Звіти

- пружність

- Зростання

- підвищення

- ROSE

- прогін

- біг

- s

- Здається,

- бачив

- Вересень

- дефіцит

- Шоу

- істотно

- Ознаки

- аналогічний

- з

- слабкий

- М'який

- Spot

- різко

- стійкий

- Як і раніше

- найсильніший

- сильно

- істотний

- такі

- пропонувати

- постачальник

- постачальники

- поставка

- ланцюжка поставок

- Ланцюги постачання

- Огляд

- стійким

- ніж

- Що

- Команда

- світ

- їх

- Там.

- вони

- це

- до

- Відстеження

- транспорт

- типовий

- Uk

- us

- Економіка США

- Ve

- віце

- Віцепрезидент

- Volatility

- було

- we

- слабкість

- тижня

- пішов

- Western

- Західна Європа

- Що

- який

- в той час як

- з

- робочі

- світ

- світовий

- зефірнет