The 2024 US presidential election could end up a second Biden-Trump contest, with former President Donald Trump the front runner for the Republican party nomination after securing a win in the Iowa caucus this week and President Joe Biden currently the front runner for the Democratic party nomination.

Regardless of which party wins, the 2024 US presidential election may affect the automotive industry profoundly. A shift in the White House or Congressional majority could impact environmental policy and the regulatory environment, and lead to changes in the federal tax and incentive support for the EV transition. That could have massive downstream repercussions on the entire automotive supply chain, by triggering changes in capital allocation and timing for planned and future automaker and supplier investments.

Two key pieces of Democratic-led legislation passed under President Joe Biden have significant impact on the development of a US EV market, the Inflation Reduction Act (IRA) and the Bipartisan Infrastructure Law (BIL). If the 2024 US presidential election results in a Republican-led White House and/or Congress, the new administration may look to curb these laws and change or eliminate federal funding. A reversal or reduction of federal subsidies could cause OEMs, suppliers, and battery companies to rethink their product and investment strategy, particularly as it relates to North American sourcing.

The election also has the potential to impact greenhouse gas emissions and fuel economy regulations. Under the previous Trump administration, less aggressive regulatory policy was enacted, and the mechanism that allows California to set its own emissions regulations was ended. Under President Biden, more aggressive targets were finalized covering regulations through the 2026 model year, and California's waiver was reinstated. <span/>Proposed EPA and NHTSA rules for the 2027 to 2032 model years are expected to be finalized before the election.

If the election results in a shift to a Republican administration, regulations could be pulled back and that California's waiver again revoked. NHTSA is required by US law to set standards at least 18 months before a model year; with a new president taking office in January 2025, a regulatory change would have to be passed nearly immediately to impact the 2027 model year. However, the process for change simply does not happen that fast. Given the time that it takes for regulation to work through the system, the earliest model year to be affected by a new change may be the 2028 model year.

Investment implications

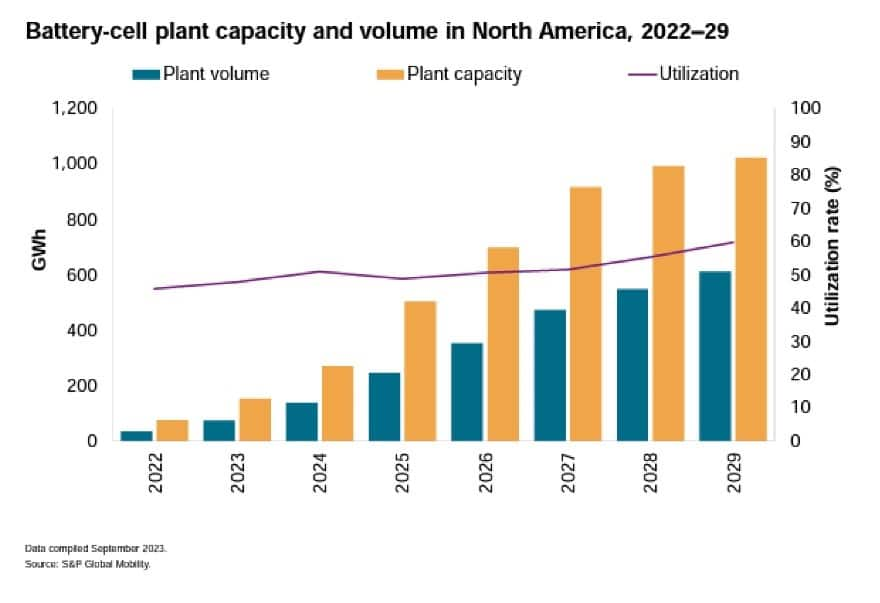

S&P Global Mobility estimates that, in the year following the enactment of the IRA in August 2022, an investment exceeding $100 billion was announced for US battery and electric vehicle manufacturing initiatives. Of particular concern are projects which have already started construction. S&P Global Mobility estimates that in 2022, the US will have seven operational battery plants, with an annual capacity of 75-gigawatt hours (GWh); after the IRA, we see as many as 24 battery plants currently planned or under construction, which could increase capacity to 732 GWh. We also expect that this investment could exceed medium-term demand.

Regardless of party affiliation, congressional representatives will need to continue to support funding for projects bringing investments and jobs to their states and districts. While on the national stage, Republicans may object to any subsidy that conjures imagery of the Green New Deal, but lawmakers in states already benefitting will need to protect those projects. This situation could create more tension than already exists between federal and state authority on a number of issues.

How will industry respond?

A reversal or reduction of subsidies could have substantial impact on for OEMs, suppliers and battery companies in terms of product and investment strategy. Without national incentives for local investment, less expensive supply sources for key materials outside of the region may become more attractive. The credits often offset the higher costs of local sourcing; without them, an already unprofitable situation can become more of a challenge.

However, S&P Global Mobility also sees potential for currently known investment plans to create more battery capacity than demand projections expect would be needed. We are also seeing some automakers and suppliers delay planned EV and battery manufacturing capacity plans for 2024. However, that is more related to changing expectations for demand rather than increased risk for the IRA subsidies to change. With planned investment likely to be higher than demand, both sides of the party aisle have pointed arguments for and against maintaining the credits.

The baseline S&P Global Mobility forecasts assume that current emissions and fuel economy regulation proposals are finalized and the IRA law remains in place and unchallenged. However, if the situation does change, we see potential for automaker reactions in several general categories:

- Automakers focused solely on EVs already;

- Those who are poised to stay flexible;

- Those who will hold a course toward electrification (or EVs) but may adjust timing and sourcing; and,

- Those who have been marching to their own timing already.

Any change to emissions regulations also has the potential to change the picture; lowering compliance requirements can enable automakers and the market to move more slowly to ZEVs but puts medium-term investment plans into question. In the longer term, continued progress to a ZEV future is supported by global policies and regulations.

Electric anyway, stay the course

The automakers who are already fully electric will, of course, continue that path. This will include Tesla, Rivian, Fisker, and Lucid.

Tesla's North American production footprint is expected to grow beginning in 2025 or 2026 when its Mexico plant is finally constructed and online. Tesla has slowed development of its Mexico plant because of concerns CEO Elon Musk has over the economy and interest rates, rather than potential changes in the political landscape. Rivian is committed to a Georgia plant under construction. Lucid's production capacity expansion plans for the US are likely to be more affected by real demand for the new Gravity SUV. If consumer acceptance trails company expectations, expansion could slow regardless of tax incentives. Meanwhile, Fisker aims for contract manufacturing and is therefore in less control over its supply chain.

2025 Lucid Gravity / Stephanie Brinley for S&P Global Mobility

Stay flexible to market demand and regulatory forces

Stellantis and BMW have focused on developing platforms that can accept ICE, EV or PHEV solutions, and potentially fuel-cell EV solutions. Mercedes-Benz is in this camp as well, with public statements that it will increasingly move to BEV, but maintain ICE vehicle production so long as consumers demand it.

Though BMW is poised to launch its Neue Klasse BEV platform in 2025, to date it has been offering EV counterparts to most of its product lineup - including expectations it will launch the X2 and iX2 in March 2024 as well as the latest Mini Cooper seeing ICE and EV versions.

2023 RAM BEV Concept / Stephanie Brinley for S&P Global Mobility

Stellantis has not yet jumped into the electrification market in the US significantly, aside from PHEV versions of Chrysler Pacifica and several Jeep products. However, in Europe, it is much more aggressive with its BEV efforts. Stellantis' electrification profile in North America is expected to change in late 2024 and 2025. In early January, the company confirmed it plans to introduce seven EVs for North America in 2024, including Jeep Recon and Wrangler S, Ram 1500 REV, Dodge Charger Daytona, and Fiat 500e. Stellantis is also expected to expand the use of its range-extender solution, which comes first in early 2025 in the Ramcharger; in that vehicle, a V6 engine generates power for an electric battery but has no connection to the drive wheels. Although Alfa Romeo is expected to blend PHEV and EV offerings, the Maserati brand is poised to go all-electric first.

For North America, the automakers in this camp may extend internal combustion engine programs or place higher emphasis on hybrid and PHEV solutions through the rest of this decade. Expectations are for EV programs to continue to be developed, however. By 2030 or so, the EV programs should be in full swing, as the investments do need to be realized.

Without the IRA subsidies, however, there is risk that these companies make different sourcing decisions. According to some late 2023 reports, Mercedes-Benz may change sourcing for the EQS SUV from the US to Germany, Though the EQS is too expensive to qualify for US consumer tax credits, it is unclear if the company had been eligible for the manufacturing credits under the IRA.

Toyota is almost a case unto itself, but fits in the "flexible" category - albeit for more philosophical reasons -- driving its forward product plan than US regulatory conditions or incentives. Though Toyota waited until 2022 to get aggressive with a BEV future, the company maintains that reaching carbon neutrality is the goal, rather than electrification for its own sake. Toyota steadfastly maintains that the number of batteries it has deployed into hybrid and PHEV products has had a greater impact on reducing overall fleet emissions than if those same batteries were deployed in a much smaller number of EVs. The result is that Toyota has a propulsion system formula that could enable the company to lean in whichever direction is required from the blend of customer and regulatory forces, including the availability of subsidies in any given region.

Stick to the strategy, with some timing changes

2025 Chevrolet Silverado EV / Stephanie Brinley for S&P Global Mobility

While a change in IRA or emissions and fuel economy requirements could cause this group of OEMs to change timing for their transition from ICE to BEV, we expect they will largely stick to their plans to move to all EV or ZEV by the about the middle or end of the next decade. Automakers in this category include GM, Volkswagen, and Hyundai Motor Group (including Hyundai, Kia and Genesis brands in the US).

Automakers potentially best positioned to modulate production and vehicle offerings throughout a murky situation include Hyundai Motor Group, and to a lesser extent, Ford Motor Company.

Hyundai Motor Group has dedicated BEV platforms and plans to grow those offerings, but most of the existing Hyundai and Kia products currently offer ICE, hybrid and PHEV solutions, with some also offering BEV on the same platform. If there is a loosening of regulations, Hyundai Motor Group has hybrids and PHEV solutions available. Presumably, they could extend and make moderate improvements to keep the products fresh if regulations and consumer demand make that the more profitable path to the end of the decade.

Ford also has more hybrid and PHEV solutions available to extend vehicle programs if they need to. Ford's plans to offer fewer models on its EV platforms and focus on higher volume for a more limited range of products could be a benefit here as well, as delaying planned capacity means delaying fewer vehicle programs.

GM is expected to be revising its EV product plan and eliminating some products, ideally shifting that capacity to other vehicles and holding down build complexity. A challenge for GM in this case may be that it has more brands to feed than Ford.

US policy agnostic

Nissan, Honda and Mazda have all indicated plans for increasing electrification and BEVs, though in the early part of this decade, none was moving quickly to address the need for the US market.

2025 Honda Prologue / Stephanie Brinley for S&P Global Mobility

Nissan executives speaking at the Japan Mobility Show in October 2023 said their plan to develop US electrified offerings will land at just the right time. Nissan has confirmed US EV production for 2025 and is also working to develop the e-Power range extender solution for US consumer demands.

Mazda was expected to lean on partner Toyota for EVs, though recent CEO remarks suggest the automaker is looking to keep this development in-house and has set an aggressive target for the 2026-27 timeframe. Mazda's North American BEV production investment is not final, but as a mainstream brand, its vehicles may be more sensitive to pricing; and being ineligible for the consumer tax credit could pose a higher risk.

Honda took an expedient course to get BEVs for both Honda and Acura brands in the US in 2024 by leveraging its work with GM. But its plan to build an affordable EV platform with General Motors was canceled in 2023. Honda's BEV development for the US will now be internal. As the product plans have changed, Honda is also increasing its reliance on hybrid offerings in the US, aiming to see half of its Accord, Civic, and CR-V sales be hybrid models.

What to watch

A Republican in the White House - combined with Congressional control - has the potential to create challenges to the regulatory structure as well as both the BIL and IRA.

All of these policies are predicated on the Biden Administration having set a soft target of seeing 50% of US light vehicle sales being zero emissions in 2030. This target is also part of Biden having the US re-join the Paris Climate Accord and targeting broader, aggressive carbon neutrality targets.

But even if a Republican candidate wins the Presidency, changes to the EV-friendly laws may be impossible without Republican control of both the House and the Senate; the IRA and BIL are simply too large to change from the present course.

In addition, several of the states in which large battery manufacturing investments are being made and where construction is already underway are swing states that are vitally important to the result of the Presidential race, with Georgia, Michigan and the Carolinas leading the way. However, there has also been pushback from residents in both Georgia and Michigan to these manufacturing investments, showing that the divide over the path to a ZEV future is playing out on the local as well as national level.

If the Republican party pushes a target of modifying the laws providing for federal funding of green-manufacturing development under the guise of fiscal discipline, investment commitments could be scaled back or delayed. The potential for ensuing lost manufacturing investment could see the Democratic party positioning itself as the party supporting business and workers regarding the country's automotive industry.

In addition, regardless of campaign promises and rhetoric, changing the law will require Congressional input and votes. With a potentially split or opposition Congress, the elected president could have a more difficult time delivering on the changes promised on the campaign trail. For industry, these factors create uncertainty, which is the most disruptive of elements. With billions of dollars and the future of these companies at stake, the industry has time and again said that certainty related to regulations and policy is what they need most in executing a forward path.

Implications for EV share

Against the backdrop of the next US election, S&P Global Mobility presents potential top-line scenarios to our baseline EV adoption forecast for the US. Today's baseline forecast includes possibility for US EV market share to be closer to 45% in 2030 and assumes that OEMs succeed in lobbying efforts to move away from EPA emissions aspirations and lean heavier on the latest NHTSA proposal, which may enable use of more alternative powertrains.

However, in the context of this discussion, if there are drastic changes to the IRA or BIL and incentives for manufacturers and consumers are reduced, we could expect to see the potential for EV share to be closer to 37% in 2030.

Should the EPA and NHTSA proposals of 2023 be finalized and unchanged, the law of the land would push electrification north of 50% in 2030.

The result is a hugely complex political and business environment, with numerous interwoven and discrete variables.

TO DISCUSS POTENTIAL ELECTION OUTCOMES WITH OUR ADVISORY TEAM

FOR MORE ON AUTOMOTIVE PLANNING AND FORECASTING

This article was published by S&P Global Mobility and not by S&P Global Ratings, which is a separately managed division of S&P Global.

- SEO Powered Content & PR Distribution. Get Amplified Today.

- PlatoData.Network Vertical Generative Ai. Empower Yourself. Access Here.

- PlatoAiStream. Web3 Intelligence. Knowledge Amplified. Access Here.

- PlatoESG. Carbon, CleanTech, Energy, Environment, Solar, Waste Management. Access Here.

- PlatoHealth. Biotech and Clinical Trials Intelligence. Access Here.

- Source: http://www.spglobal.com/mobility/en/research-analysis/2024-us-presidential-election-and-the-auto-industry.html

- :has

- :is

- :not

- :where

- ][p

- $UP

- 2022

- 2023

- 2024

- 2025

- 2026

- 2028

- 2030

- 24

- a

- About

- Accept

- acceptance

- accord

- According

- Act

- addition

- address

- adjust

- administration

- Adoption

- advisory

- affect

- affected

- affordable

- After

- again

- against

- aggressive

- Aiming

- aims

- All

- all-electric

- allocation

- allows

- almost

- already

- also

- alternative

- Although

- america

- American

- an

- and

- announced

- annual

- any

- ARE

- arguments

- article

- AS

- aside

- assume

- assumes

- At

- attractive

- AUGUST

- authority

- auto

- automakers

- automotive

- automotive industry

- availability

- available

- away

- back

- backdrop

- Baseline

- batteries

- battery

- BE

- because

- become

- been

- before

- Beginning

- being

- benefit

- benefitting

- BEST

- between

- biden

- Biden Administration

- Billion

- billions

- bipartisan

- Blend

- BMW

- both

- Both Sides

- brand

- brands

- Bringing

- broader

- build

- business

- but

- by

- california

- Camp

- Campaign

- CAN

- canceled

- candidate

- Capacity

- capital

- carbon

- Carbon Neutrality

- case

- categories

- Category

- Cause

- ceo

- certainty

- chain

- challenge

- challenges

- change

- changed

- Changes

- changing

- Chevrolet

- chrysler

- Civic

- Climate

- closer

- combined

- comes

- commitments

- committed

- Companies

- company

- complex

- complexity

- compliance

- concept

- Concern

- Concerns

- conditions

- CONFIRMED

- Congress

- Congressional

- connection

- construction

- consumer

- Consumers

- contest

- context

- continue

- continued

- contract

- control

- cooper

- Costs

- could

- counterparts

- country

- course

- covering

- create

- credit

- Credits

- Current

- Currently

- customer

- Date

- deal

- decade

- decisions

- dedicated

- delay

- Delayed

- delaying

- delivering

- Demand

- demands

- democratic

- democratic party

- deployed

- develop

- developed

- developing

- Development

- different

- difficult

- direction

- discipline

- discuss

- discussion

- disruptive

- divide

- Division

- do

- Dodge

- does

- dollars

- donald

- Donald Trump

- down

- drive

- driving

- earliest

- Early

- economy

- efforts

- elected

- Election

- Electric

- electric vehicle

- electrification

- elements

- eligible

- eliminate

- eliminating

- Elon

- Elon Musk

- Emissions

- emphasis

- enable

- end

- ended

- Engine

- Entire

- Environment

- environmental

- Environmental policy

- EPA

- estimates

- Europe

- EV

- Even

- evs

- exceed

- executing

- executives

- existing

- exists

- Expand

- expansion

- expect

- expectations

- expected

- expensive

- extend

- extent

- factors

- FAST

- Federal

- fewer

- Fiat

- final

- finalized

- Finally

- First

- Fiscal

- FLEET

- flexible

- Focus

- focused

- following

- Footprint

- For

- Forces

- Ford

- Ford Motor Company

- Forecast

- forecasts

- Former

- formula

- Forward

- fresh

- from

- front

- Fuel

- full

- fully

- funding

- future

- GAS

- General

- General Motors

- generates

- Genesis

- Georgia

- Germany

- get

- given

- Global

- GM

- Go

- goal

- gravity

- greater

- Green

- greenhouse gas

- Group

- Grow

- had

- Half

- happen

- Have

- having

- here

- higher

- hold

- holding

- HOURS

- House

- However

- HTML

- HTTPS

- Hugely

- Hybrid

- Hyundai

- ICE

- ideally

- if

- immediately

- Impact

- important

- impossible

- improvements

- in

- Incentive

- Incentives

- include

- includes

- Including

- Increase

- increased

- increasing

- increasingly

- indicated

- industry

- inflation

- Infrastructure

- initiatives

- input

- interest

- Interest Rates

- internal

- into

- introduce

- investment

- Investment strategy

- Investments

- Iowa

- IRA

- issues

- IT

- ITS

- itself

- January

- Japan

- jeep

- Jobs

- joe

- Joe Biden

- jpg

- just

- Keep

- Key

- Kia

- known

- Land

- landscape

- large

- largely

- Late

- latest

- launch

- Law

- lawmakers

- Laws

- lead

- leading

- least

- Legislation

- less

- lesser

- Level

- leveraging

- light

- likely

- Limited

- lineup

- lobbying

- local

- Long

- longer

- Look

- looking

- lost

- lowering

- lucid

- made

- Mainstream

- maintain

- maintaining

- maintains

- Majority

- make

- managed

- Manufacturers

- manufacturing

- many

- March

- March 2024

- Market

- Maserati

- massive

- materials

- May..

- means

- Meanwhile

- mechanism

- Mexico

- Michigan

- Middle

- mobility

- model

- models

- moderate

- months

- more

- most

- Motor

- Motors

- move

- moving

- much

- Musk

- National

- nearly

- Need

- needed

- neutrality

- New

- next

- Nissan

- no

- nomination

- None

- North

- north america

- now

- number

- numerous

- object

- october

- of

- offer

- offering

- Offerings

- Office

- offset

- often

- on

- online

- operational

- opposition

- or

- Other

- our

- out

- outcomes

- outside

- over

- overall

- own

- paris

- part

- particular

- particularly

- partner

- party

- passed

- path

- picture

- pieces

- Place

- plan

- planned

- planning

- plans

- plant

- plants

- platform

- Platforms

- plato

- Plato Data Intelligence

- PlatoData

- playing

- poised

- policies

- policy

- political

- positioned

- positioning

- possibility

- potential

- potentially

- power

- present

- presents

- presidency

- president

- president biden

- President Donald Trump

- president joe biden

- presidential

- presidential election

- previous

- pricing

- process

- Product

- Production

- Products

- Profile

- profitable

- profoundly

- Programs

- Progress

- projections

- projects

- Prologue

- promised

- promises

- proposal

- Proposals

- propulsion

- protect

- providing

- public

- published

- Push

- pushes

- Puts

- qualify

- question

- quickly

- Race

- RAM

- range

- Rates

- rather

- ratings

- reaching

- reactions

- real

- realized

- reasons

- recent

- Reduced

- reducing

- reduction

- regarding

- Regardless

- region

- Regulation

- regulations

- regulatory

- related

- relates

- reliance

- remains

- repercussions

- Reports

- Representatives

- Republican

- Republicans

- require

- required

- Requirements

- residents

- Respond

- REST

- result

- Results

- Reversal

- right

- Risk

- rivian

- rules

- runner

- s

- S&P

- S&P Global

- Said

- sake

- sales

- same

- scenarios

- Second

- securing

- see

- seeing

- sees

- Senate

- sensitive

- set

- seven

- several

- Share

- shift

- SHIFTING

- should

- show

- showing

- Sides

- significant

- significantly

- simply

- situation

- slow

- Slowly

- smaller

- So

- Soft

- solely

- solution

- Solutions

- some

- Sourcing

- speaking

- split

- Stage

- stake

- standards

- started

- State

- statements

- States

- stay

- Stick

- Strategy

- structure

- subsidy

- substantial

- succeed

- suggest

- supplier

- suppliers

- supply

- supply chain

- support

- Supported

- Supporting

- Swing

- system

- takes

- taking

- Target

- targeting

- targets

- tax

- term

- terms

- Tesla

- than

- that

- The

- The Future

- the Law

- their

- Them

- There.

- therefore

- These

- they

- this

- this week

- those

- though?

- Through

- throughout

- time

- timeframe

- timing

- to

- today

- too

- took

- toward

- toyota

- trail

- transition

- triggering

- trump

- Uncertainty

- unclear

- under

- Underway

- until

- us

- US election

- use

- vehicle

- Vehicles

- volkswagen

- volume

- votes

- was

- Way..

- we

- week

- WELL

- were

- What

- when

- which

- while

- white

- White House

- WHO

- will

- win

- Wins

- with

- without

- Work

- workers

- working

- would

- year

- years

- yet

- zephyrnet

- zero