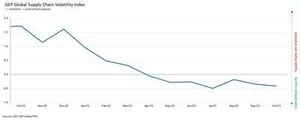

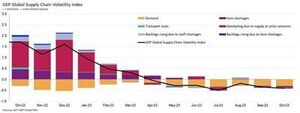

The GEP Global Supply Chain Volatility Index — the indicator tracking demand conditions, shortages, transportation costs, inventories and backlogs based on a monthly survey of 27,000 businesses — decreased again in October to -0.41, from -0.35 in September, indicating a 7th successive month of rising spare capacity across the world’s supply chains.

Additionally, the extent to which supplier capacity went underutilised was even greater than in September and August. Coupled with October’s downturn in demand for raw materials, components and commodities, this shows rising slack in global supply chains.

“While the shrinking of global suppliers’ order books is not worsening, there are no signs of improvement,” explained Jamie Ogilvie-Smals, vice president, consulting, GEP. “The notable increase in supplier capacity in Asia, which was driven by China, provides global manufacturers with greater leverage to drive down prices and inventories in 2024.”

A key finding from October’s report was the strongest rise in excess capacity across Asian supply chains since June 2020. Sustained weakness in demand, coupled with falling pressures on factories in Asia, indicates that the global manufacturing recession has further to run. With the exception of India, which continues to perform strongly, large economies in the region, such as Japan and China, are losing momentum.

Suppliers in Europe continue to report the largest level of spare capacity. In fact, the lower levels in GEP’s supply chain index for the continent have only been seen during the global financial crisis between 2008 and 2009. They highlight sustained weakness in economic conditions across the continent. Western Europe, particularly Germany’s manufacturing industry, is a key driver behind the region’s deterioration.

Viszonylag fényes folt Észak-Amerika, ahol az ellátási láncok többletkapacitással rendelkeznek, de sokkal kisebb mértékben, mint másutt, mivel az Egyesült Államok gazdasága továbbra is rugalmasságát mutatja, éles ellentétben Európával.

2023. október Főbb megállapítások

Demand: Demand for raw materials, components and commodities remains depressed, although the downturn seems to have stabilised. There are still no signs of conditions improving, however, as global purchasing activity fell again in October at a pace similar to what we’ve seen since around mid-year.

Demand: Demand for raw materials, components and commodities remains depressed, although the downturn seems to have stabilised. There are still no signs of conditions improving, however, as global purchasing activity fell again in October at a pace similar to what we’ve seen since around mid-year.- Készletek: A kereslet csökkenése miatt adataink azt mutatják, hogy a globális vállalkozások újabb hónapja szüntettek meg készleteket, jelezve a cashflow megőrzésére irányuló erőfeszítéseket.

- Anyaghiány: A cikkek hiányáról szóló jelentések továbbra is a legalacsonyabb szinten állnak 2020 januárja óta.

- Labour shortages: Shortages of workers are not impacting global manufacturers’ capacity to produce, with reports of backlogs due to inadequate labour supply running at historically typical levels.

- Transportation: Global transportation costs held steady with September’s level, although oil prices have declined in recent weeks.

Regionális ellátási lánc volatilitása

-

Észak-Amerika: Az index -0.34-re esett, -0.30-ról. Ez továbbra is sokkal lágyabb, mint a globális átlag, és továbbra is az Egyesült Államokra utal. a gazdaság puha landolásra készül.

- Európa: Az index -0.90-ről -1.01-re emelkedett, de továbbra is azon a szinten marad, amely jelentős gazdasági törékenységet jelez.

- Egyesült Királyság: Az index valamivel feljebb, -0.93-ra emelkedett -0.98-ról. Ennek ellenére az adatok a többletkapacitás jelentős növekedésére utalnak a brit piacok beszállítóinál.

- Asia: Notably, the index dropped to -0.38, from -0.20, highlighting the biggest rise in spare supplier capacity in Asia since June 2020 as the region’s resilience fades.

- SEO által támogatott tartalom és PR terjesztés. Erősödjön még ma.

- PlatoData.Network Vertical Generative Ai. Erősítse meg magát. Hozzáférés itt.

- PlatoAiStream. Web3 Intelligence. Felerősített tudás. Hozzáférés itt.

- PlatoESG. Carbon, CleanTech, Energia, Környezet, Nap, Hulladékgazdálkodás. Hozzáférés itt.

- PlatoHealth. Biotechnológiai és klinikai vizsgálatok intelligencia. Hozzáférés itt.

- Forrás: https://www.logisticsit.com/articles/2023/11/21/supply-chains-worldwide-remain-significantly-underutilised-gep-global-supply-chain-volatility-index

- :van

- :is

- :nem

- :ahol

- 000

- 01

- 121

- 20

- 2008

- 2020

- 2023

- 2024

- 27

- 30

- 300

- 35%

- 41

- 7th

- 90

- 98

- a

- át

- tevékenység

- újra

- Bár

- Amerika

- és a

- Másik

- VANNAK

- körül

- AS

- Ázsia

- ázsiai

- At

- Augusztus

- átlagos

- alapján

- óta

- mögött

- között

- Legnagyobb

- Könyvek

- Fényes

- vállalkozások

- de

- by

- Kapacitás

- lánc

- láncok

- Kína

- Commodities

- alkatrészek

- Körülmények

- tekintélyes

- tanácsadó

- kontinens

- folytatódik

- tovább

- kontraszt

- kiadások

- összekapcsolt

- válság

- dátum

- csökkent

- Kereslet

- kijelző

- le-

- LE

- hajtás

- hajtott

- gépkocsivezető

- csökkent

- két

- alatt

- Gazdasági

- Gazdasági feltételek

- gazdaságok

- gazdaság

- erőfeszítések

- máshol

- Eter (ETH)

- Európa

- Még

- kivétel

- többlet

- magyarázható

- mérték

- tény

- gyárak

- elhalványul

- Eső

- pénzügyi

- pénzügyi válság

- megtalálása

- A

- törékenység

- ból ből

- további

- Németország

- Globális

- globális pénzügyi

- Globális pénzügyi válság

- nagyobb

- Legyen

- hős

- <p></p>

- Kiemel

- kiemelve

- történelmileg

- azonban

- HTTPS

- ütköztető

- javulás

- javuló

- in

- Növelje

- index

- India

- jelzi

- jelezve

- jelző

- Mutató

- ipar

- ITS

- Jamie

- január

- Japán

- jpg

- június

- Kulcs

- Munkaügyi

- leszállási

- nagy

- legnagyobb

- kevesebb

- szint

- szintek

- Tőkeáttétel

- vesztes

- alacsonyabb

- legalacsonyabb

- Gyártók

- gyártási

- feldolgozó ipar

- piacok

- anyagok

- Lendület

- Hónap

- havi

- sok

- nem

- Északi

- Észak Amerika

- figyelemre méltó

- nevezetesen

- október

- of

- Olaj

- on

- csak

- érdekében

- előrendelések

- mi

- Béke

- különösen

- teljesít

- Plató

- Platón adatintelligencia

- PlatoData

- pont

- lebeg

- megőrzés

- elnök

- Áraink

- gyárt

- biztosít

- beszerzési

- Nyers

- új

- recesszió

- vidék

- relatív

- marad

- maradványok

- jelentést

- Jelentések

- rugalmasság

- Emelkedik

- felkelő

- ROSE

- futás

- futás

- s

- Úgy tűnik,

- látott

- szeptember

- hiány

- Műsorok

- jelentősen

- Jelek

- hasonló

- óta

- laza

- Puha

- Spot

- merev

- állandó

- Még mindig

- legerősebb

- erősen

- lényeges

- ilyen

- javasol

- szállító

- szállítók

- kínálat

- ellátási lánc

- Ellátási láncok

- Felmérés

- kitartó

- mint

- hogy

- A

- a világ

- azok

- Ott.

- ők

- ezt

- nak nek

- Csomagkövetés

- szállítás

- tipikus

- Uk

- us

- Az amerikai gazdaság

- Ve

- vice

- Alelnök

- Illékonyság

- volt

- we

- gyengeség

- Hetek

- ment

- Nyugati

- Nyugat-Európa

- Mit

- ami

- míg

- val vel

- dolgozók

- világ

- világszerte

- zephyrnet