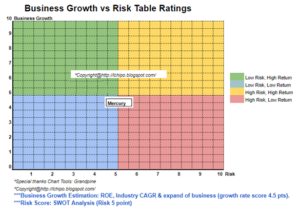

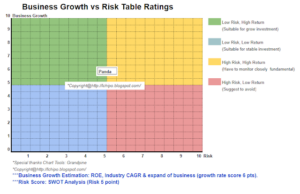

IPO Rating (1.75/5.0 Stars)

Copyright@http://lchipo.blogspot.com/

ہمیں فیس بک پر فالو کریں: https://www.facebook.com/LCH-Trading-Signal-103388431222067/

تاریخ

درخواست دینے کے لیے کھلا ہے: 29/06/2020

اپلائی کرنے کے لیے بند ہے: 10/07/2020

فہرست سازی کی تاریخ: 23/07/2020

دارالحکومت اشتراک کریں

مارکیٹ کیپ: RM46.944 ملین

Total Shares: mil shares (Public apply:10.8 mil, Company Insider/Miti/Private Placement/other: 97.2mil)

صنعت

Property & construction segment have been in slow growth phase in Malaysia for this few years. However it still cannot category as sunset industry. I will be in temporary sleeping mode for industry growth.

**CAGR posted in Prospectus book using forecase 2019-2024, we decided do not take this as reference as it did not reflect true CAGR 5 year average of previous year result.

Competitor (Profit before tax margin)

TCS: 6.1% (PE5.75)

Gagasan: 15.2% (PE9.31)

GDB: 11.7% (PE12.92)

انتا بینا: 7.2% (PE5.9)

بزنس

Construction services for buildings, infrastructure, civil and structural works in Malaysia.

بنیادی

مارکیٹ: اککا بازار

قیمت: RM0.23 (EPS:0.04)

P/E: PE5.75

ROE: 26.5 (IPO پرو فارما III)

ROE: 26.5 (2019), 16.6 (2018), 10.5(2017), 8.6 (2016)

IPO کے بعد کیش اور فکسڈ ڈپازٹ: RM0.0899 فی حصص

IPO کے بعد NA: RM0.16

Total debt to current asset after IPO: 0.86 (Debt:119.484 mil, Non-Current Asset: 39.607mil, Current asset: 138.962mil)

ڈیویڈنڈ پالیسی: کوئی فکس ڈیویڈنڈ پالیسی نہیں۔

ماضی کی مالی کارکردگی (آمدنی، EPS)

2019: RM358.424 mil (EPS: 0.0435)

2018: RM146.266 mil (EPS: 0.0269)

2017: RM71.718 mil (EPS: 0.0172)

2016: RM103.628 mil (EPS: 0.0141)

خالص منافع کا مارجن

2019: 4.37٪

2018: 6.71٪

2017: 8.63٪

2016: 4.91٪

IPO شیئر ہولڈنگ کے بعد

Dato’ Ir Tee Chai Seng: 59.07%

Datin Koh Ah Nee: 10.42%

FYE2021 کے لیے ڈائریکٹرز کا معاوضہ (مجموعی منافع 2019 سے)

Dato’ Ir Tee Chai Seng: RM1.004 mil

Datin Koh Ah Nee: RM367k

Tan Sri Dato’ Sri Izzuddin bin Dali: RM75k

Dato’ Seri Ir Mohamad Othman Bin Zainal Azim: RM63k

Ooi Guan Hoe: RM63k

مجموعی منافع سے ڈائریکٹر کا کل معاوضہ: RM1.572 ملین یا 4.17%

FYE2021 کے لیے کلیدی انتظامی معاوضہ (مجموعی منافع 2019 سے)

Ooi Kee An: RM200k-250k

Yap Choo Cheng: RM200k-250k

Liew Kok Yoong: RM100k-150k

Ho Chee Woei: RM150k-200k

Koo Yoke Ping: RM50k-100k

Ng Lee Foong: RM50k-100k

key management remuneration from gross profit: RM1.05 mil or 2.78%

فنڈ کا استعمال

Purchase of new construction machinery and equipment: 62.80%

ورکنگ کیپٹل: 20.29%

فہرست سازی کے اخراجات: 16.91%

اچھی بات یہ ہے:

1. Low PE, ROE26.5

2. ROE increase over pass few years.

3. Use 83.09% IPO fund to expand business.

4. Revenue have growth for pass 4 year.

5. Low interest environment will encourage property industry.

بری چیزیں:

1. Compare to other competitor, profit margin not high & net profit margin less than 10%.

2. Direcrtor fee have a bit expensive.

3. Listing Expenses is expensive.

4. Unable to know the true industry CAGR for past 5 years.

5. کوئی فکسڈ ڈیویڈنڈ پالیسی نہیں۔

Conclusions (Blogger is not wrote any recommedation & suggestion. All is personal opinion)

The industry of their business is on sleeping mode. As property & construction is growing slow in Malaysia for past few years. We still have many other good opportunities to allocate properly our capital for investment.

IPO قیمت: RM0.23

اچھا وقت: RM0.32 (PE8)

برا وقت: RM0.16 (PE4)

*تقسیم صرف ذاتی رائے اور نقطہ نظر ہے۔ اگر کوئی نیا سہ ماہی نتیجہ جاری ہوتا ہے تو تاثر اور پیشن گوئی بدل جائے گی۔ قارئین کو اپنا خطرہ مول لینا چاہیے اور کمپنی کی بنیادی قدر کی پیشن گوئی کو ایڈجسٹ کرنے کے لیے ہر سہ ماہی کے نتائج کو فالو اپ کرنے کے لیے اپنا ہوم ورک کرنا چاہیے۔

Source: http://lchipo.blogspot.com/2020/07/tcs-group-holdings-berhad.html

- اثاثے

- بٹ

- BP

- کاروبار

- CAGR

- دارالحکومت

- تبدیل

- کمپنی کے

- تعمیر

- موجودہ

- قرض

- DID

- ڈائریکٹر

- لابحدود

- ماحولیات

- کا سامان

- توسیع

- اخراجات

- فیس بک

- مالی

- درست کریں

- پر عمل کریں

- فنڈ

- اچھا

- گروپ

- بڑھتے ہوئے

- ترقی

- ہائی

- گھر کا کام

- HTTPS

- اضافہ

- صنعت

- انفراسٹرکچر

- دلچسپی

- سرمایہ کاری

- IPO

- IT

- لسٹنگ

- ملائیشیا

- انتظام

- خالص

- رائے

- دیگر

- پی اینڈ ای

- کارکردگی

- پنگ

- پالیسی

- قیمت

- فی

- منافع

- جائیداد

- عوامی

- ریڈر

- آمدنی

- رسک

- سروسز

- حصص

- غروب آفتاب

- ٹیکس

- عارضی

- وقت

- us

- قیمت

- لنک

- کام کرتا ہے

- سال

- سال