Countries with deeper, more inclusive and more competitive banking systems are exhibiting lower levels of fintech activity than countries with less developed and less competitive banking systems, a phenomenon which could be in part explained by higher barriers to entry and fewer opportunities for digital financial services in countries with advanced banking ecosystems, a research by the World Bank reveals.

In a paper titled “Global Patterns of Fintech Activity and Enabling Factors: Fintech and the Future of Finance Flagship Technical Note”, the organization shares findings of a study which sought to document patterns of fintech activity across the world and help identify enabling factors.

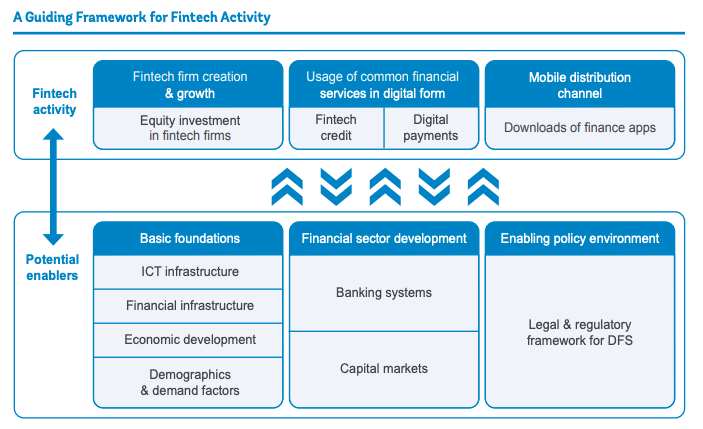

Results from the study reveal that fintech activity is closely related to a country’s economic and institutional development, and that there is significant fintech credit and digital payment usage in several low- and middle-income countries. Factors like financial sector development, information and communications technology (ICT) infrastructure, and fintech-relevant policies are influencing fintech activity levels in different countries.

In particular, the report notes the strong negative correlation between fintech activity and banking system development, possibly relating to the potential demand for new fintech providers as well as supply-side constraints.

In countries with less developed and less competitive banking systems, there are greater opportunities for digital financial services to develop owing to these markets’ relatively larger underbanked and unbanked population, and higher costs of financial services, the report says.

High demand in these countries dominates supply-side constraints associated with anti-competitive behavior by incumbents such as barriers to entry, the study found.

While fintech activity is negatively correlated with banking system development, the research shows that it is, on the contrary, positively correlated with capital market development.

This trend suggests that well-developed equity and bond market, which reflect in part a more favorable investment climate, might foster the emergence of fintech companies by providing the funding startups need to develop, the report says.

Findings of the World Bank research are consistent with other studies which show that fast-growing young economies are the biggest adopters of fintech products.

The EY Global Fintech Adoption Index, a survey of 27,000 digitally active consumers in 27 markets, reveals that Asia is the global leader in fintech adoption, with China (87%) and India (87%) ranking at the top of the list.

High levels of fintech development and adoption in emerging markets are oftentimes driven by an unmet demand for financial services, and the high cost of traditional finance. Demographics also play an important role, as younger cohorts, which are prevalent in emerging markets, are more likely to trust and adopt fintech services.

ICT infrastructure, legal environment among key enablers

In addition to the degree of development of the local banking system, the World Bank report notes that fintech development also depends on the availability of a supportive ICT and financial infrastructures.

Countries witness more fintech startups when the latest technological infrastructure is readily available, and people have more mobile phone subscriptions, the report notes. Additionally, better access to ICT infrastructure, measured by the availability of the internet and mobile phones, is often associated with higher usage of digital financial services.

In particular, the report states that ICT payment infrastructure is playing a critical role in the usage of digital payments services. This finding is evidenced by the popularity of real-time payment systems like the United Payments Interface (UPI) in India and PromptPay in Thailand, which are now among the preferred payment methods of consumers.

The report also notes that although a stricter regulatory environment for the financial sector might increase compliance costs and therefore deter financial innovation, it could also foster fintech adoption by promoting a safe, sound, and efficient financial system.

Stronger consumer protection rules, for example, might encourage greater usage of digital financial services by building the necessary trust and confidence in fintech providers. Similarly, the existence of e-money laws, which typically offer legal certainty, predictability, and transparency regarding the issuance of e-money, could facilitate the emergence of a new, innovative and secure payment instrument.

Finally, the report stresses that while a high-quality policy environment is a necessity for fintech development, it is an insufficient condition and other factors must be put in place for the industry to flourish.

This conclusion was drawn from the mixed patterns observed in the study’s results. While, the degree of fintech activity is consistently on the low end of the distribution in countries scoring poorly on policy indices, activity does vary widely across countries scoring high on these indices. In addition to that, several countries with supportive and enabling policy environments were found to be ranking relatively low on fintech activity despite their regulatory efforts.

Featured image credit: Edited from freepik

- SEO Powered Content & PR Distribution. Get Amplified Today.

- PlatoData.Network Vertical Generative Ai. Empower Yourself. Access Here.

- PlatoAiStream. Web3 Intelligence. Knowledge Amplified. Access Here.

- PlatoESG. Automotive / EVs, Carbon, CleanTech, Energy, Environment, Solar, Waste Management. Access Here.

- PlatoHealth. Biotech and Clinical Trials Intelligence. Access Here.

- ChartPrime. Elevate your Trading Game with ChartPrime. Access Here.

- BlockOffsets. Modernizing Environmental Offset Ownership. Access Here.

- Source: https://fintechnews.sg/77947/fintech/world-bank-study-reveals-key-factors-enabling-fintech-growth/

- :is

- 000

- 27

- a

- access

- across

- active

- activity

- addition

- Additionally

- adopt

- adopters

- Adoption

- advanced

- also

- Although

- among

- an

- and

- ARE

- AS

- asia

- associated

- At

- availability

- available

- Bank

- Banking

- banking system

- Banking systems

- barriers

- BE

- Better

- between

- Biggest

- bond

- bond market

- Building

- by

- capital

- caps

- certainty

- China

- Climate

- closely

- Communications

- Companies

- competitive

- compliance

- conclusion

- condition

- confidence

- consistent

- consistently

- constraints

- consumer

- Consumer Protection

- Consumers

- contrary

- correlated

- Correlation

- Cost

- Costs

- could

- countries

- country’s

- credit

- critical

- deeper

- Degree

- Demand

- Demographics

- depends

- Despite

- develop

- developed

- Development

- different

- digital

- Digital Payment

- Digital Payments

- digitally

- distribution

- document

- does

- dominates

- drawn

- driven

- e-Money

- Economic

- economies

- Ecosystems

- efficient

- efforts

- emergence

- emerging

- emerging markets

- enabling

- encourage

- end

- entry

- Environment

- environments

- equity

- Ether (ETH)

- evidenced

- example

- Exhibiting

- explained

- facilitate

- factors

- false

- favorable

- fewer

- finance

- financial

- financial innovation

- Financial sector

- financial services

- financial system

- finding

- findings

- fintech

- Fintech Companies

- fintech startups

- flagship

- flourish

- For

- Foster

- found

- friendly

- from

- funding

- future

- Global

- greater

- Growth

- Have

- help

- High

- high-quality

- higher

- HTTPS

- ICT

- identify

- image

- important

- in

- Inclusive

- Increase

- india

- Indices

- industry

- influencing

- information

- information and communications

- Infrastructure

- infrastructures

- Innovation

- innovative

- Institutional

- instrument

- Interface

- Internet

- investment

- issuance

- IT

- Key

- larger

- latest

- Laws

- leader

- Legal

- less

- levels

- like

- likely

- List

- local

- Low

- lower

- Market

- Markets

- max-width

- measured

- methods

- might

- mixed

- Mobile

- mobile phone

- mobile phones

- more

- must

- necessary

- necessity

- Need

- negative

- negatively

- New

- Notes

- now

- observed

- of

- offer

- often

- oftentimes

- on

- opportunities

- organization

- Other

- Paper

- part

- particular

- patterns

- payment

- payment methods

- Payment Systems

- payments

- People

- phenomenon

- phone

- phones

- Place

- plato

- Plato Data Intelligence

- PlatoData

- Play

- playing

- policies

- policy

- popularity

- population

- possibly

- potential

- preferred

- prevalent

- Products

- promoting

- protection

- providers

- providing

- put

- Ranking

- real-time

- reflect

- regarding

- regulatory

- related

- relatively

- report

- research

- Results

- return

- reveal

- Reveals

- Role

- rules

- safe

- says

- scoring

- sector

- secure

- Services

- several

- Shares

- show

- Shows

- significant

- Similarly

- Singapore

- sought

- Sound

- Startups

- States

- stricter

- strong

- studies

- Study

- subscriptions

- such

- Suggests

- supply-side

- supportive

- Survey

- system

- Systems

- Technical

- technological

- Technology

- Thailand

- than

- that

- The

- The Future

- the world

- their

- There.

- therefore

- These

- this

- to

- top

- traditional

- traditional finance

- Transparency

- Trend

- Trust

- typically

- unbanked

- unbanked population

- underbanked

- unmet

- UPI

- Usage

- was

- WELL

- were

- when

- which

- while

- widely

- window

- with

- witness

- world

- World Bank

- young

- Younger

- zephyrnet