UPCOMING EVENTS:

- Monday: US NAHB Housing Market Index.

- Tuesday: RBA Meeting Minutes, BoJ Policy Decision, Canada

CPI, US Building Permits and Housing Starts. - Wednesday: PBoC LPR, UK CPI, US Consumer Confidence, BoC

Summary of Deliberations. - Thursday: Canada Retail Sales, US Q3 GDP Final, US Jobless

Claims. - Friday: Japan CPI, UK Retail Sales, Canada GDP, US PCE,

University of Michigan Consumer Sentiment Final.

Tuesday

The BoJ is expected to keep everything

unchanged with rates at -0.10% and YCC to target the 10yr JGBs at 0% with 1% as

a reference cap. The latest Japanese

CPI showed a slight easing in inflation rates

although they remain well above the 2% target. The central bank is mainly

focused on wage growth as it doesn’t foresee sustainable price increases.

The wages

data picked up recently and the BoJ might

want to wait for some more months before considering a tweak in its monetary

policy. The latest big development was a speech

a couple of weeks ago by BoJ Governor Ueda where, if you read between the

lines, he hinted to an end to the NIRP in 2024 and triggered a huge rally

in the Japanese Yen.

BoJ

The Canadian CPI Y/Y is expected at 2.9%

vs. 3.1% prior,

while the M/M figure is seen at -0.2% vs. 0.1% prior. The BoC is focused on

the underlying inflation measures (common, median and trimmed-mean), so

those will be the figures to pay attention to. BoC

Governor Macklem last Friday said that

the 2% inflation target is now in sight, which reaffirmed the central bank’s

neutral approach. The major central banks have ended their tightening cycles,

so the market is now pricing in rate cuts in 2024. Strong data might just

trim the amount of rate cuts expected but not erase them.

Canada Inflation Measures

Wednesday

The PBoC is expected to keep the LPR rates

unchanged at 3.45% for the 1 year and 4.20% for the 5 years. Such expectations

come from the PBoC leaving the MLF

rate unchanged recently which generally

acts as a precursor to a change in the LPR rates. Chinese officials have

been promising forceful and precise actions to spur growth although we haven’t

seen much of that with the deflationary

forces continuing to weigh on the economy.

PBoC

The UK CPI Y/Y is expected at 4.4% vs.

4.6% prior,

while the M/M figure is seen at 0.2% vs. 0.0% prior. The Core CPI Y/Y is

expected at 5.5% vs. 5.7% prior, while the M/M reading is seen at 0.2% vs. 0.3%

prior. Last week, the BoE

kept interest rates unchanged

and maintained its neutral stance in stark divergence with the surprisingly

dovish FOMC decision. Again, the market’s reaction function is now “strong

data equals less rate cuts while weak data equals more rate cuts”.

UK Core CPI YoY

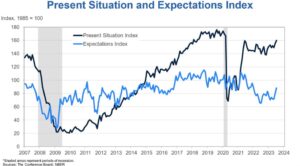

The US Consumer Confidence has been

falling steadily in the past few months as the labour market started to weaken.

In fact, compared to the University of Michigan Consumer Sentiment, which shows

more how the consumers see their personal finances, the Consumer Confidence

shows how the consumers see the labour market.

The consensus sees the index rising to 104.3 in December vs. 102.0 in November.

US Consumer Confidence

Thursday

The US Jobless Claims continue to be one

of the most important releases every week as it’s a more timely indicator on

the state of the labour market. Initial Claims keep on hovering around cycle

lows, which shows us that layoffs have not yet picked up notably, but

Continuing Claims have been rising and that’s indicative of people finding it

harder to get another job after being laid off. This week the consensus

sees Initial Claims at 218K vs. 202K prior,

while there’s no estimate at the time of writing for Continuing Claims,

although the last week’s number was 1876K vs. 1856K prior.

US Jobless Claims

Friday

The Japanese Core CPI Y/Y is expected at

2.5% vs. 2.9% prior,

while there’s no consensus on the other measures at the time of writing

although the Headline CPI Y/Y was 3.3% in October and the Core-Core CPI Y/Y was

4.0%. This inflation report comes on the last day before Christmas holidays and

after the BoJ Policy Decision, so the market’s reaction is likely to be

muted unless we get big surprises.

Japan Core-Core CPI YoY

The US PCE Y/Y is expected at 2.8% vs.

3.0% prior,

while the M/M figure is seen at 0.0% vs. 0.0% prior. The Core PCE Y/Y, which is

the Fed’s preferred inflation measures, is expected at 3.4% vs. 3.5% prior,

while the M/M reading is seen at 0.2% vs. 0.2% prior. Unless we get big

surprises, it’s unlikely to see the market react to this report given that we

already saw the more timely CPI data. If the Core PCE M/M prints at 0.2%,

the 6-month annualised rate would fall to 2.4%, which is basically at the Fed’s 2%

target.

US Core PCE YoY

- SEO Powered Content & PR Distribution. Get Amplified Today.

- PlatoData.Network Vertical Generative Ai. Empower Yourself. Access Here.

- PlatoAiStream. Web3 Intelligence. Knowledge Amplified. Access Here.

- PlatoESG. Carbon, CleanTech, Energy, Environment, Solar, Waste Management. Access Here.

- PlatoHealth. Biotech and Clinical Trials Intelligence. Access Here.

- Source: https://www.forexlive.com/news/weekly-market-outlook-18-22-december-20231217/

- :has

- :is

- :not

- :where

- $UP

- 1

- 102

- 2%

- 2% Inflation

- 2024

- 26

- a

- above

- actions

- acts

- After

- again

- ago

- already

- Although

- amount

- an

- and

- Another

- approach

- around

- AS

- At

- attention

- Bank

- Banks

- Basically

- BE

- been

- before

- being

- between

- Big

- BoC

- boj

- BOJ policy decision

- Building

- but

- by

- Canada

- Canada GDP

- Canada retail Sales

- Canadian

- cap

- central

- Central Bank

- Central Banks

- change

- Christmas

- claims

- come

- comes

- Common

- compared

- confidence

- Consensus

- considering

- consumer

- consumer sentiment

- Consumers

- continue

- continuing

- Core

- Couple

- CPI

- CPI data

- cuts

- cycle

- cycles

- data

- day

- December

- decision

- Development

- Divergence

- Doesn’t

- Dovish

- easing

- economy

- end

- ended

- Equals

- estimate

- Every

- everything

- expectations

- expected

- fact

- Fall

- Falling

- few

- Figure

- Figures

- final

- Finances

- finding

- focused

- FOMC

- For

- foresee

- Friday

- from

- function

- GDP

- generally

- get

- given

- Governor

- Growth

- harder

- Have

- he

- headline

- hinted

- holidays

- housing

- housing market

- How

- HTTPS

- huge

- important

- in

- Increases

- index

- indicative

- Indicator

- inflation

- Inflation Rates

- initial

- interest

- Interest Rates

- IT

- ITS

- Japan

- Japan CPI

- Japanese

- Japanese Yen

- Job

- jobless claims

- jpg

- just

- Keep

- kept

- Labour

- Last

- latest

- layoffs

- leaving

- less

- likely

- lines

- Lows

- LPR

- mainly

- major

- Market

- market outlook

- measures

- meeting

- Michigan

- might

- minutes

- Monetary

- months

- more

- most

- much

- Neutral

- no

- notably

- now

- number

- october

- of

- officials

- on

- ONE

- Other

- Outlook

- past

- Pay

- PBOC

- pce

- People

- permits

- personal

- picked

- plato

- Plato Data Intelligence

- PlatoData

- policy

- precise

- precursor

- preferred

- price

- pricing

- prints

- Prior

- promising

- Q3

- rally

- Rate

- Rates

- RBA

- React

- reaction

- Read

- Reading

- reaffirmed

- recently

- reference

- Releases

- remain

- report

- retail

- Retail Sales

- rising

- Said

- sales

- saw

- see

- seen

- sees

- sentiment

- showed

- Shows

- Sight

- So

- some

- stance

- stark

- started

- starts

- State

- steadily

- such

- SUMMARY

- surprises

- sustainable

- Target

- that

- The

- The State

- their

- Them

- they

- this

- this week

- those

- tightening

- time

- timely

- to

- triggered

- tweak

- Uk

- UK CPI

- UK Retail Sales

- underlying

- university

- University of Michigan

- University of Michigan Consumer Sentiment

- unlikely

- us

- US Building Permits

- US Jobless Claims

- US NAHB Housing Market Index

- vs

- wage

- wait

- want

- was

- we

- week

- weekly

- Weeks

- weigh

- WELL

- which

- while

- will

- with

- would

- writing

- year

- years

- Yen

- yet

- you

- zephyrnet