No one can predict the future of real estate, but you can prepare. Find out what to prepare for and pick up the tools you’ll need at Virtual Inman Connect on Nov. 1-2, 2023. And don’t miss Inman Connect New York on Jan. 23-25, 2024, where AI, capital and more will be center stage. Bet big on the future and join us at Connect.

Homebuyer demand for mortgages inched up last week, but just barely, as mortgage rates climbed to the highest level in more than two decades, according to a weekly survey of lenders by the Mortgage Bankers Association (MBA).

The MBA’s Weekly Mortgage Applications Survey showed requests for purchase loans were up by a seasonally adjusted 1 percent last week compared to the week before, but down 19 percent from a year ago. Requests to refinance were essentially unchanged from the previous week and down 9 percent from a year ago.

Joel Kan

“The 30-year fixed mortgage rate is at 7.67 percent – the highest level since 2000 and 40 basis points higher than a month ago,” MBA Deputy Chief Economist Joel Kan said in a statement. “Application activity remains depressed and close to multi-decade lows, with purchase applications still almost 20 percent behind last year’s pace. Refinance applications also continue to be limited, and the average loan size has fallen to its lowest level since 2017.”

The average loan size for refinancing applications dipped to $245,100, helping drive refinancing dollar volume down 16 percent from a year ago.

While rates for most types of mortgages increased last week, rates on adjustable-rate mortgage (ARM) loans, driving an increase in ARM volume and an increase in overall applications. Requests for ARM loans were up 15 percent week over week, boosting ARM share to 9.2 percent of all applications, the highest since November 2022, Kan said.

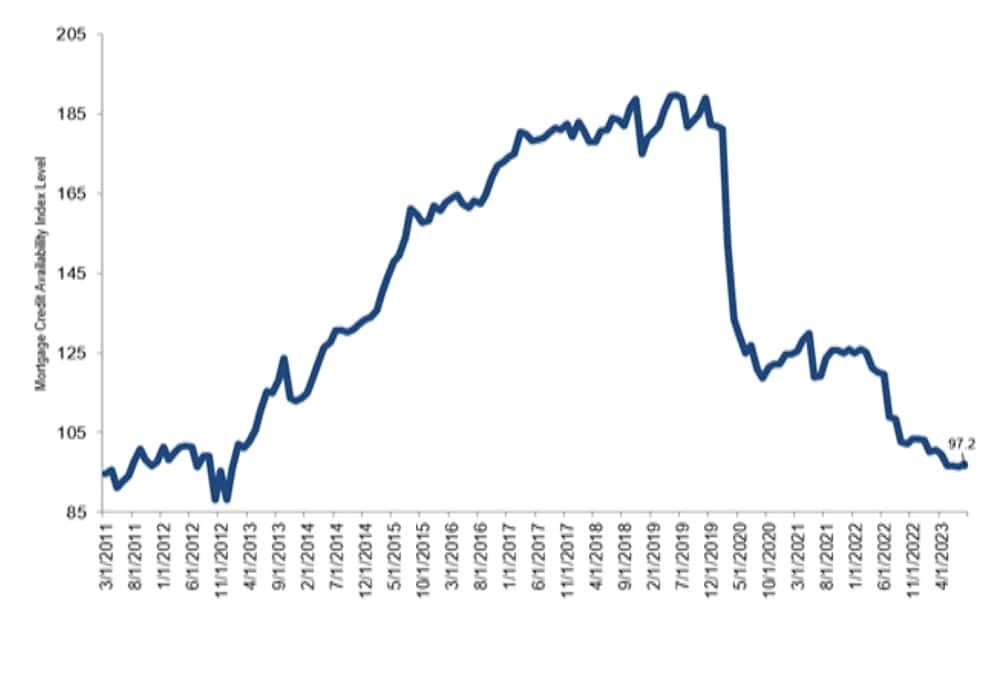

In a separate monthly report, the MBA said mortgage credit availability improved slightly in September, but that lending standards are nearly as tight as they’ve been in a decade.

Mortgage credit availability remains tight

Source: Mortgage Bankers Association, ICE Mortgage Technology.

The MBA’s Mortgage Credit Availability Index (MCAI), which analyzes data from ICE Mortgage Technology, rose by 0.6 percent to 97.2 in September, indicating loosening of credit. The index was benchmarked to 100 in March 2012.

Jumbo mortgages posted the boost in credit availability, increasing by 0.8 percent. It was the second straight monthly increase in the jumbo index, driven by lenders expanding their ARM and non-QM (non-qualified mortgage) offerings, Kan said.

“Credit availability increased slightly in September, as lenders increased their loan offerings marginally to meet the changing needs of borrowers who are facing higher mortgage rates,” Kan said in a statement.

But looking at the big picture, Kan said industry capacity “has declined significantly since the peak originations months in 2021, and MBA expects to see further declines in originations volume, given the high interest rate environment and typical seasonal slowdown.”

For the week ending Oct. 6, the MBA reported average rates for the following types of loans:

- For 30-year fixed-rate conforming mortgages (loan balances of $726,200 or less), rates averaged 7.67 percent, up from 7.53 percent the week before. Although points decreased to 0.75 from 0.80 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans, the effective rate also increased.

- Rates for 30-year fixed-rate jumbo mortgages (loan balances greater than $726,200) averaged 7.70 percent, up from 7.51 percent the week before. Although points dereased to 0.57 from 0.74 (including the origination fee) for 80 percent LTV loans, the effective rate also increased.

- For 30-year fixed-rate FHA mortgages, rates averaged 7.40 percent, up from 7.29 percent the week before. With points increasing to 1.08 from 1.01 (including the origination fee) for 80 percent LTV loans, the effective rate also increased.

- Rates for 15-year fixed-rate mortgages popular with homeowners who are refinancing averaged 6.51 percent, up from 6.39 percent the week before. With points increasing to 0.92 from 0.78 (including the origination fee) for 80 percent LTV loans, the effective rate also increased.

- For 5/1 adjustable-rate mortgages (ARMs), rates averaged 6.33 percent, down from 6.49 percent the week before. With points decreasing to 0.90 from 1.21 (including the origination fee) for 80 percent LTV loans, the effective rate also decreased.

On Monday, the MBA, National Association of Realtors and National Association of Home Builders urged Fed policymakers to calm bond investors who fund most mortgages by promising that the Fed is done hiking rates, and has no plans to sell trillions of dollars of mortgage bonds that the central bank bought during the pandemic.

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

Email Matt Carter

- SEO Powered Content & PR Distribution. Get Amplified Today.

- PlatoData.Network Vertical Generative Ai. Empower Yourself. Access Here.

- PlatoAiStream. Web3 Intelligence. Knowledge Amplified. Access Here.

- PlatoESG. Carbon, CleanTech, Energy, Environment, Solar, Waste Management. Access Here.

- PlatoHealth. Biotech and Clinical Trials Intelligence. Access Here.

- Source: https://www.inman.com/2023/10/12/mortgage-rates-hit-20-year-high-as-demand-close-to-multi-decade-low/

- :has

- :is

- :where

- $UP

- 01

- 08

- 1

- 100

- 15%

- 16

- 19

- 20

- 200

- 2000

- 2012

- 2017

- 2021

- 2022

- 2023

- 2024

- 29

- 33

- 39

- 40

- 49

- 51

- 53

- 67

- 7

- 70

- 75

- 8

- 80

- 9

- 90

- 97

- a

- According

- activity

- Adjusted

- ago

- AI

- All

- almost

- also

- Although

- an

- analyzes

- and

- applications

- ARE

- ARM

- arms

- AS

- Association

- At

- availability

- average

- balances

- Bank

- bankers

- basis

- BE

- been

- before

- behind

- benchmarked

- Bet

- Big

- Big Picture

- Biggest

- bond

- Bonds

- boost

- boosting

- borrowers

- bought

- builders

- but

- by

- CAN

- Capacity

- capital

- Center

- center stage

- central

- Central Bank

- changing

- chief

- Climbed

- Close

- COM

- compared

- Connect

- continue

- credit

- data

- decade

- decades

- Declines

- decreased

- delivered

- Demand

- deputy

- Dollar

- dollars

- done

- Dont

- down

- dramatically

- drive

- driven

- driving

- during

- Economist

- Effective

- ending

- Environment

- essentially

- estate

- Every

- expanding

- expects

- facing

- Fallen

- Falls

- Fed

- fee

- Find

- fixed

- following

- For

- from

- fund

- further

- future

- given

- greater

- helping

- here

- High

- higher

- highest

- hiking

- Hit

- Home

- HTTPS

- ICE

- improved

- in

- Including

- Increase

- increased

- increasing

- index

- indicating

- industry

- interest

- INTEREST RATE

- Investors

- IT

- ITS

- Jan

- join

- Join us

- jpg

- just

- Last

- lenders

- lending

- less

- Level

- Limited

- loan

- Loans

- looking

- lowest

- lowest level

- Lows

- LTV

- March

- matt

- max-width

- MBA

- Meet

- miss

- Monday

- Month

- monthly

- MONTHLY REPORT

- months

- more

- Mortgage

- Mortgages

- most

- National

- nearly

- Need

- needs

- New

- news

- no

- November

- Oct

- of

- Offerings

- on

- ONE

- or

- origination

- originations

- out

- over

- overall

- Pace

- pandemic

- Peak

- percent

- pick

- picture

- plans

- plato

- Plato Data Intelligence

- PlatoData

- points

- Popular

- posted

- predict

- Prepare

- previous

- promising

- purchase

- Rate

- Rates

- ratio

- real

- real estate

- remains

- report

- Reported

- requests

- right

- ROSE

- roundup

- Said

- seasonal

- Second

- see

- sell

- separate

- September

- Share

- showed

- significantly

- since

- Size

- Slowdown

- Stage

- standards

- Still

- straight

- subscribe

- Survey

- Technology

- than

- that

- The

- the Fed

- The Future

- the world

- their

- to

- tools

- trillions

- two

- types

- typical

- us

- volume

- was

- Wednesday

- week

- weekly

- were

- What

- which

- WHO

- will

- with

- world

- year

- you

- Your

- zephyrnet