Welcome back to The SaaS Playbook, a bi-weekly rundown of the top articles, tactics, and thought leadership in B2B SaaS. Not a subscriber yet?

🎨 Just last week, Adobe shocked the software world by announcing their plan to acquire competitor Figma for a whopping $20b, representing a 50x ARR valuation. And if you read the fine print, it was likely north of 50x given the report states 400m is where Figma plans to end 2022. So how can the Adobe finance team justify paying WAY above market value and making CEO Dylan Field a 30 year old billionaire? Well, as Hunter Walk points out, what Adobe is really thinking about is protecting their precious market cap (~134b, -51% over the TTM), so paying a fraction of that number to wipe out a competitor who is stealing their customers makes loads of sense. The real question is if the FTC will attempt to block the transaction for antitrust reasons, given their recent tightening on anti-competitive behavior.

🏀 Upfront Ventures partner Mark Suster doesn't believe the current market dip is going to be a small blip and V-shaped recovery, instead, writing that current valuations will represent how the market prices venture for the long term. Now that’s not the spiciest take we’ve ever heard, but more interestingly, he covers what could happen to the current $290b of VC dried powder (Pitchbook estimation) waiting to get thrown into the game. Investors’ jobs are to deploy, and they will find ways to do it, but Suster thinks we will see a bit of a lag until founders’ valuation expectations come down. This will make investing in companies which raised during the peak of valuations in late 2020-2021 especially tricky.

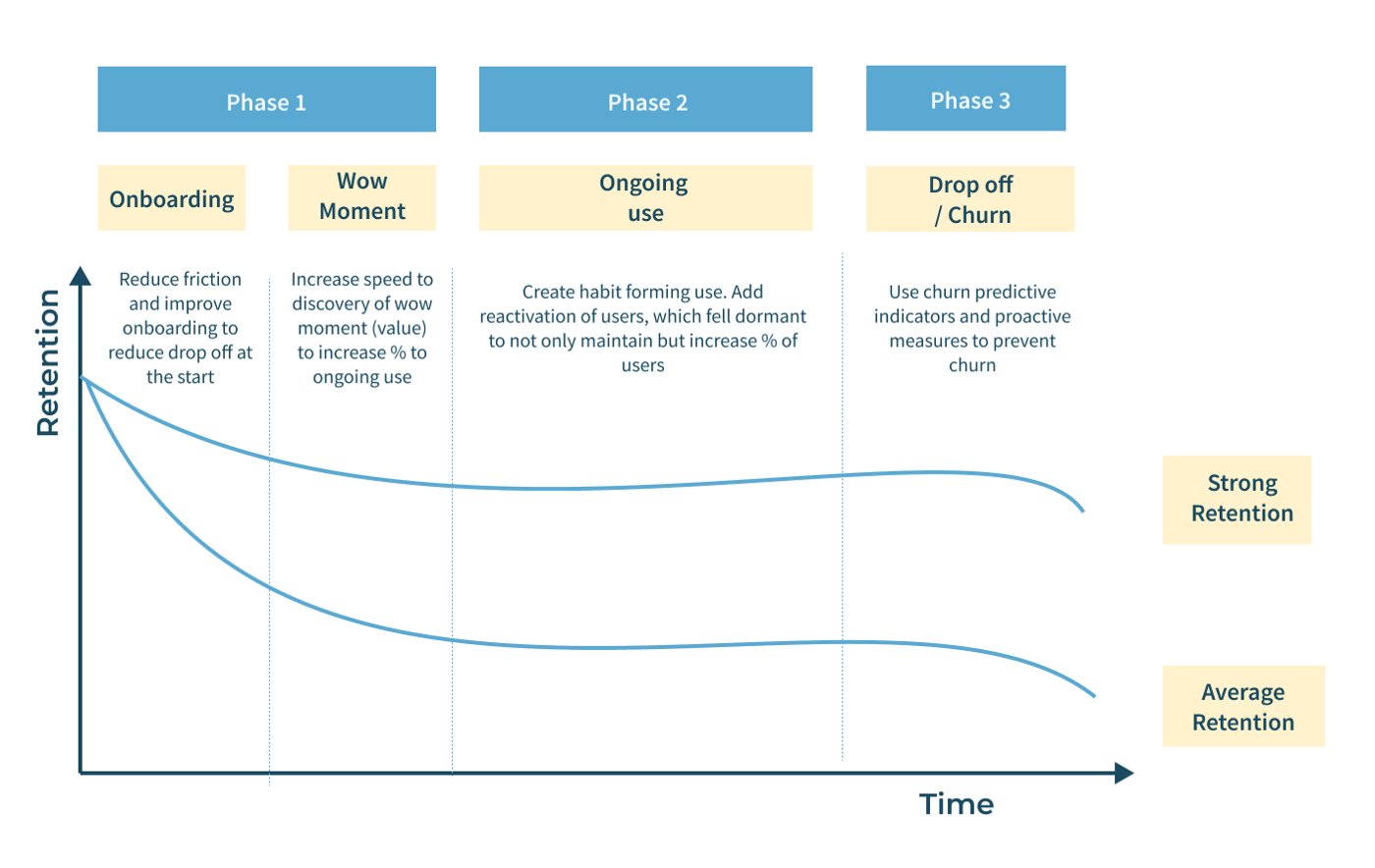

➰ Growth is priority #1 for most companies, so much to the point that they undervalue the impact of retention. You can think about retention in two ways, design (before use, meaning things which are built into your product) and analysis (after use, so methods like cohort analysis, customer segmentation, etc.). Design is what inform your analysis, so once you have meaningful data to glean insights from, you can really start to iterate on your design. This piece by Hello Growth lays out 3 phases of retention (see below) and how you can improve your numbers at each stage via product changes. The general idea is to create habitual loops by adding triggers to an existing behavior, then rewarding users in hopes of creating a new habit for them.

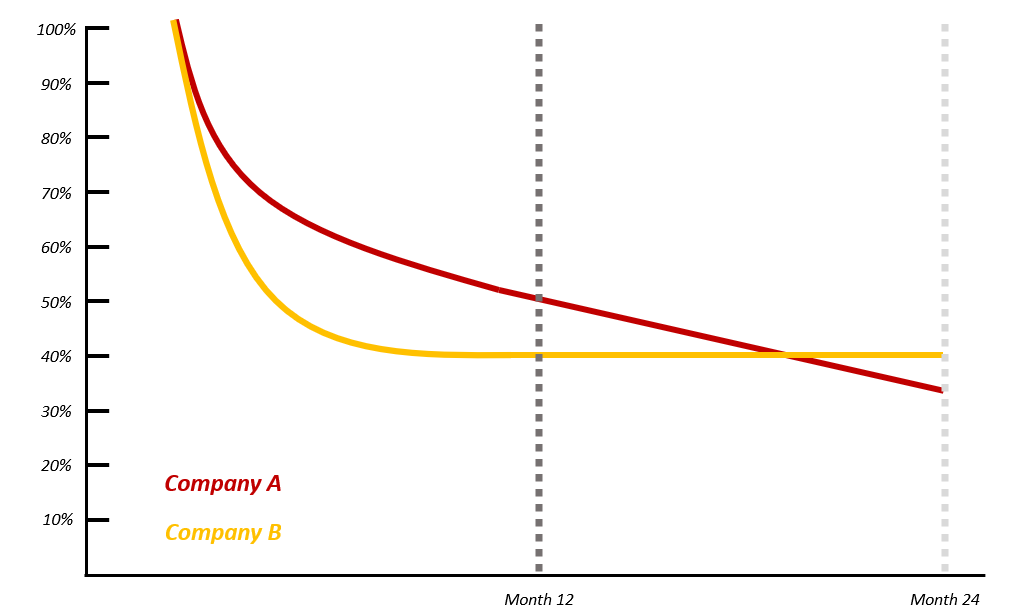

📉 Now to move to the analysis side of retention. A mistake you’ll sometimes see with founders’ retention analysis is that they focus on static annual retention (12 month retention, for example) without looking at the slope of their retention curve. Parsa Saljoughian, Whoop’s VP of Strategic Finance, compares two companies in this post to illustrate why that’s a mistake. You’ll see that just because his “Company A” has a 50% 12 month retention rate and Company B has a 40% rate, it doesn’t mean Company A’s retention is actually better. In his example, Company A exhibits an exponential decay, while B has a linear decay, so Company A is actually on pace to leak customers much more quickly than B.

As always, if you or someone you know is considering selling, taking investment, or even looking for a bit of debt we might be able to help out. Just reply to this thread and we can get acquainted. We may or may not be a perfect fit, but we’re always up for meeting SaaS founders and extending our network where helpful.

- SEO Powered Content & PR Distribution. Get Amplified Today.

- Platoblockchain. Web3 Metaverse Intelligence. Knowledge Amplified. Access Here.

- Source: https://thesaasplaybook.substack.com/p/figma-for-fifty-x-what-happens-to

- 10

- 2022

- 400M

- 9

- a

- Able

- About

- above

- acquainted

- acquire

- actually

- Adobe

- After

- always

- analysis

- and

- annual

- antitrust

- articles

- B2B

- back

- because

- before

- believe

- below

- Better

- billionaire

- Bit

- Block

- built

- button

- Can Get

- ceo

- Changes

- Cohort

- COM

- come

- Companies

- company

- competitor

- considering

- could

- create

- Creating

- Current

- curve

- customer

- Customers

- data

- Debt

- deploy

- Design

- Dip

- Doesn’t

- down

- during

- each

- especially

- etc

- Even

- EVER

- example

- exhibits

- existing

- expectations

- exponential

- extending

- field

- figma

- finance

- Find

- fine

- fit

- Focus

- founders

- fraction

- from

- FTC

- game

- General

- get

- given

- going

- good

- Growth

- happen

- happens

- heard

- help

- helpful

- hopes

- How

- HTML

- HTTPS

- idea

- Impact

- improve

- in

- insights

- instead

- investing

- investment

- IT

- Jobs

- Know

- Last

- Late

- Leadership

- leak

- likely

- loads

- Long

- looking

- make

- make investing

- MAKES

- Making

- mark

- Market

- market crashes

- Market Prices

- meaning

- meaningful

- medium

- meeting

- methods

- might

- mistake

- Month

- more

- most

- move

- network

- New

- North

- number

- numbers

- Old

- Pace

- partner

- paying

- Peak

- perfect

- piece

- Pitchbook

- plan

- plato

- Plato Data Intelligence

- PlatoData

- Point

- points

- Post

- Precious

- Prices

- primary

- priority

- Product

- protecting

- question

- quickly

- raised

- Rate

- Read

- real

- reasons

- recent

- recovery

- reply

- report

- represent

- representing

- retention

- rewarding

- round

- SaaS

- segmentation

- Selling

- sense

- shocked

- Slope

- small

- So

- Software

- Solving

- Someone

- Stage

- start

- States

- Strategic

- tactics

- Take

- taking

- team

- The

- their

- things

- Thinking

- Thinks

- thought

- thought leadership

- tightening

- to

- top

- transaction

- true

- use

- users

- Valuation

- Valuations

- value

- VC

- venture

- Ventures

- via

- Waiting

- ways

- week

- What

- which

- while

- WHO

- will

- without

- world

- writing

- X

- year

- Your

- zephyrnet