Deteriorating economic circumstances set stage for an

uncertain 2023 landscape

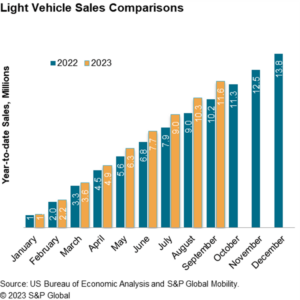

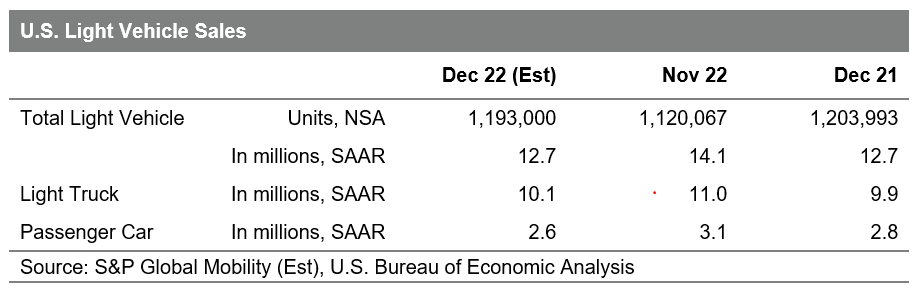

With volume for the month projected at 1.19 million units,

December U.S. auto sales are estimated to translate to an estimated

sales pace of below 13.0 million units (seasonally adjusted annual

rate: SAAR). The SAAR reading would be the weakest monthly result

since May 2022, and the underlying daily selling rate metric would

be a slight step back from the trend of the preceding three

months.

The daily selling rate metric in December is expected to

decelerate mildly from the remarkably steady 44.9K per day average

since August. While stubbornly sticky low levels of inventory

dampened year-end clearance incentives, the backward movement in

the daily selling metric could be a signal of a retrenching auto

consumer. The December result will bring the full-year U.S. light

vehicle sales total to 13.8 million units, an 8% decline from the

CY2021 total.

“Looking back at a tumultuous year for auto demand, the December

sales result reflects apparent steadiness in the market,” said

Chris Hopson, principal analyst at S&P Global Mobility. “Steadiness should not be misconstrued as exuberance though. Auto

consumers are plagued by an uncertain economic environment, high

vehicle prices, higher interest rates, and low inventory

levels.”

None of these issues will be resolved quickly as the market

moves through 2023. The S&P Global Mobility auto outlook for

next year carries a countercyclical narrative: Expected production

levels will continue to increase, even as economic conditions are

expected to deteriorate through the early stages of next year.

“The advancing production levels, along with reports of

sustained retail order books, recovering stock of vehicles, and a

fleet sector that remains starved for product, should provide some

impetus to auto demand levels even as an economic recession looms,”

Hopson said. “We project calendar-year 2023 sales volume of 14.8

million units in the U.S., a 7% increase from the estimated 2022

tally. But even as the industry hopes to leave 2022 in the review

mirror, uncertainty awaits entering the New Year.” (For S&P

Global Mobility’s full 2023 Global outlook,click here).

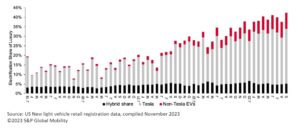

Next year will see the sustained advance of battery-electric

vehicles. BEV share of new light vehicle sales in the U.S. is

expected to reach 6.2% in December 2022, which would translate to a

full-year share of 5.4% – a YOY volume growth estimate of

approximately 260,000 units. Further electrificaton progress in

2023 will be fueled by product rollouts including the Lexus RZ,

Fisker Ocean, a wave of BEV product from GM including the Chevrolet

Equinox EV and Chevrolet Blazer EV, and advancing Tesla production

levels. Incentives as directed by the IRA should also promote

sales.

This article was published by S&P Global Mobility and not by S&P Global Ratings, which is a separately managed division of S&P Global.

- SEO Powered Content & PR Distribution. Get Amplified Today.

- Platoblockchain. Web3 Metaverse Intelligence. Knowledge Amplified. Access Here.

- Source: http://www.spglobal.com/mobility/en/research-analysis/december-auto-sales-wrap-up-year-on-a-familiar-note.html

- 000

- 1

- 2%

- 2022

- a

- Adjusted

- advance

- analyst

- and

- annual

- apparent

- approximately

- article

- AUGUST

- auto

- average

- back

- below

- Books

- bring

- circumstances

- conditions

- consumer

- Consumers

- continue

- could

- daily

- day

- December

- Decline

- Demand

- Division

- Early

- Economic

- economic recession

- Environment

- estimate

- estimated

- Ether (ETH)

- EV

- Even

- expected

- familiar

- FLEET

- from

- full

- further

- Global

- GM

- Growth

- High

- higher

- hopes

- HTML

- HTTPS

- in

- Incentives

- Including

- Increase

- industry

- interest

- Interest Rates

- inventory

- IRA

- issues

- Leave

- levels

- light

- looking

- Low

- low levels

- managed

- Market

- metric

- million

- mirror

- mobility

- Month

- monthly

- months

- movement

- moves

- NARRATIVE

- New

- new year

- next

- ocean

- order

- Outlook

- Pace

- plagued

- plato

- Plato Data Intelligence

- PlatoData

- Prices

- Principal

- Product

- Production

- Progress

- project

- projected

- promote

- provide

- published

- quickly

- Rate

- Rates

- ratings

- reach

- Reading

- recession

- recovering

- reflects

- remains

- Reports

- resolved

- result

- retail

- review

- S&P

- S&P Global

- Said

- sales

- Sales Volume

- sector

- Selling

- set

- Share

- should

- Signal

- since

- some

- Stage

- stages

- steady

- Step

- stock

- Tally

- Tesla

- The

- three

- Through

- to

- Total

- translate

- Trend

- u.s.

- Uncertainty

- underlying

- units

- vehicle

- Vehicles

- volume

- Wave

- which

- while

- will

- would

- wrap

- year

- zephyrnet