The housing market is now aggressively out of reach for first-time home buyers. Nearly sixty percent of homes for sale are unaffordable to the average American. What’s causing such a lack of affordability? High mortgage rates, meager supply, and baby boomers refusing to sell their single-family homes (seriously). These factors have created a housing market where “forced renter households” will become the norm…but not for long.

According to Matthew Gardner, Chief Economist at Windermere Real Estate, there’s at least some hope on the horizon. Mathew knows the solution to this almost unfathomable unaffordability issue, and it’s much simpler than most people think. In this episode, he talks about the primary driver of high home prices, the factors causing so many Americans to rent, and why we can’t repair this market using the same housing market “incentives” that worked in the past.

And, as someone who works regularly with large-scale investors, Mathew has some advice for those still trying to invest in a market where profits seem improbable. When will mortgage rates head down? How long will unaffordability last? And what’s the solution Matthew thinks will solve it all? We’ll get into all that in this episode!

Click here to listen on Apple Podcasts.

Listen to the Podcast Here

Read the Transcript Here

Dave:

Hey everyone, welcome to On The Market. I’m your host, Dave Meyer, joined today by James Dainard. James, is that a… Do you have a tower of Rockstar Energy Drink behind you?

James:

I do, it’s my… My staff got me a Rockstar cake for my 40th birthday. So, it had this beautiful bouquet on top, and so it’s been slow. It’s kind of like the cake in your kitchen though. I could feel like I’m pulling the frosting off because I’m pulling one can out at a time. I was trying to keep it, but I can’t help it.

Dave:

James, you’re an easy man to buy a gift for, if all you need is Rockstar Energy Drink. For those who don’t know James personally, he is never more than a few inches away from Rockstar, so that seems like a very good gift for him.

James:

A sales fuel. Sales fuel.

Dave:

Absolutely. Well, you recommended the excellent guest we have today. Tell us first of all, who our guest is and why you wanted to bring him on?

James:

Yeah, so Matthew Gardner is the chief economist of the Windermere, which is a real estate company mostly in the Pacific Northwest or the West Coast. But in our local market, they are the biggest brokerage. They have the best brand presence. And for years, I’ve been listening to Matthew talk about the economy, whether it was in the recession times or even up in today, and he’s just very factual. He understands stats, he looks at trends, and he’s just a very smart guy. And he’s so well-spoken with how he delivers the information. But everybody in the Pacific Northwest loves Matthew. We all listen to his reports. He always provides value.

Dave:

Yeah, absolutely. I didn’t know who Matthew was until we booked him for the show, and I’ve been reading some of his reports here. And I’m super excited to talk to him about affordability, because this is… We talk about rates, which obviously is a lot on the show, that has a huge impact on affordability. But there are a lot of variables that go into affordability. And I think there’s a little bit of misunderstanding and confusion around the topic, so I’m really looking forward to digging into the affordability question with him. Is there anything else you’re hoping to talk to him about?

James:

Well, I am hoping he gives me a little gold nugget for the Pacific Northwest of what to go buy, but I don’t know if he’s going to be able to give me that.

Dave:

Like, you want a specific address, like he’s going to tell you exactly what to go buy.

James:

Yeah, “Buy here, it will grow.”

Dave:

If he knows that, he might keep that for some paying clients. I don’t know if he just dishes that out to an entire podcast audience.

James:

That’s true. Well, maybe we’ll be buddy buddies by the end of the podcast, and he’ll give me those little golden gems.

Dave:

Well, I think no matter what, it might not be down to the address level, but I’m sure we’re going to get some golden gems out of Matthew. And for all of you listening, if you do appreciate us bringing on these types of economists who help you unpack and understand the market that we’re in right now, I help identify opportunities for your own investment portfolio. Please make sure to write On The Market a review. You can do that either on Spotify or on Apple.

And I know it’s just like this little thing, and I promise it only takes like 30 seconds, but it really does help the show a lot be able to attract these types of guests, and continuing to make this great content. So, if you’re a loyal listener and you haven’t yet written us a review, we would really appreciate if you took one minute to do that on Spotify or Apple right now. With that said, let’s bring on Matthew Gardner, the chief economist for Windermere Real Estate. Matthew Gardner, welcome to On The Market. Thanks for being here.

Matthew:

Hello, Dave. Good to be here. Thanks for the invitation.

Dave:

Absolutely. We’re excited to have you. Let’s start by having you introduce yourself and tell our audience a little bit about what you do as it relates to real estate and real estate investing.

Matthew:

As far as a background, as you can probably gather, I’m not from around here. I was born, raised and educated in the United Kingdom. After completing my formal education at Oxford and London School of Economics, I joined an old company of land agents. And these are companies that managed institutional portfolios of real estate. And the company I worked for represented not just my college, but the royal family as well. And there, I was involved as an analyst in advising on their portfolio, where they should sell, where they should buy.

I came to the Pacific Northwest, I’m based now in Seattle, in the late ’90s to visit my sister actually who was already living here. And what I found very quickly is that real estate developers, well, they really ride on themselves in deciding what to build. No one’s really advising them. So, I saw a niche, opened up my own company, spent 18 years advising developers, governments, and other entities on what was going on in the development world. And Windermere Real Estate was a very early client of mine. That relationship continued through my entire time having my company. So, eight years ago when they talked me into joining them… And Windermere is a company, if you don’t know this, we have about 300 offices in the 10 Western States. About 6,500 brokers that sold roughly $45 billion worth of real estate last year. And as chief economist, my ultimate goal is to analyze and interpret economic information, so I can advise our brokers on what’s going on, so they can therefore best advise their clients.

Dave:

All right, Matthew. Well, I could see why James wanted to have you on. You’re obviously an expert in his favorite market of Seattle, and obviously are doing the type of work that all of our audience is very eager to hear about. So, I’ve read a few of your reports, but let’s start… I want to dig into affordability today, but let’s just start by having you share some of your just high-level thoughts about the housing market today, to get us rolling.

Matthew:

Well, I think the big thing that everyone, it’s like the 800-pound gorilla for want of a better word, is inventory. There is none. And of course there’s nothing on the market to buy, then brokers can’t sell anything. And that’s the reason why we’re going to see a remarkably low level of transactions this year. Now, is it going to get better? Well, that’s perhaps something we’ll talk about momentarily. But I think there are a couple of things are, one is supply, lack of it.

And on the other side of the equation, is a lot of people saying, “Okay, well, look at where interest rates, where mortgage rates are today. We’re at what? 7.2% I think, this morning. Isn’t that going to cause the market to, in essence, collapse in the same way it did in 2007?” And I would argue that is certainly not the case, but it is a big concern. It’s a big concern certainly as it relates to affordability. But right now, we are in a housing market that quite frankly just lacks direction. It doesn’t know where it wants to be and where it’s going to go, certainly over the course of the next year or so.

James:

What we’ve seen over the last six months is you keep hearing the doom and gloom about rate increasing. We’ve seen them dramatically go up over the last nine months. And I think everybody’s been waiting for that shoe to drop, but yet that we still see the median home price creeping up nationwide, which is, I don’t know if that’s a good thing or a bad thing for Jerome Powell, and whether he’s just going to keep increasing rates because it’s not going in the direction he wants.

But what is your take on that, because I think that’s caught everybody off guard. I did not think that the median home price would be climbing. And it’s not going up rapidly, but it’s had steady increases as rates keep going up. Is that a concern that you think rates will continue to go? Or is it more that you just think that the inventory’s so low, it doesn’t even matter, and people are finding a way to buy?

Matthew:

I think it’s probably more the latter rather than the former in that respect, James. Do I think rates are going to continue to rise? I think it is unlikely. And I think quite frankly that we’ve peaked out pretty much where we are today. I’ll be massively surprised, I think everyone else would, to see rates continue to get up into the eights, and even potentially north of that. So, I think we’ve peaked.

But as far as its impact on housing, I think you’re absolutely right. A lot of people thought it will, borrowing costs, if they’ve doubled. And as we all know, right? It’s a very simple piece of math. If you want to keep the same payment, well, for every one percentage point increase in mortgage rates, you can afford to borrow 10% less, and keep that payment the same.

So, whatever you’re paying, let’s say at four, if rates went to five, and you wanted to keep that payment the same as you had before, then you could borrow 10% less. So, everyone thought, “Yeah, the market’s going to cause the market to collapse, some massive erosion in home prices.” But it is that supply side part of the equation that really is supporting values. And it goes back to Econ 101, right? And if you have limited supply, but still net-new demand, that allows prices to appreciate.

But I think a lot of people are also hedging. They’re saying, “Okay, you know what? I found the perfect house. It’s one I’ve been wanting to buy forever. It’s now on the market. I know I hate mortgage rates where they are, but I’ll buy now, and I will refinance down the road.” So, the expectation is that rates will come down, and that is really what is supporting home values, at least nationally. Of course, not all markets are created equal.

Dave:

So, Matthew, we’re sort of talking a little bit around here about affordability, and obviously there are multiple inputs into affordability, so I want to dig into that. But can you just tell our audience a little bit about what affordability means in terms of the housing market, and what are the different variables that make up affordability?

Matthew:

Only from affordability index, and as you know, a lot of entities are out there that put their own numbers out. And what it really looks at is the ability for a household who’s making an area’s median income, “Can they afford a median priced house based upon the last quarter, last year’s sale price?” Normally, it’s quarterly. So, that really is the math that goes into it. So you’ll know what they’re making, you know what they can borrow, make some assumptions on down payments, taxes, et cetera. But can they afford to buy some or not?

And I think if you look at affordability in general, and quite frankly, it’s something which has been keeping me awake at night for the last 20 odd years. It’s always been an issue because there is a massive undersupply of housing. And so, is housing affordable across the country? It’s not, but I think we’ll probably get to that point in a minute. But in essence, it really looks at relationship between home prices in a location, and how much households are making.

Dave:

Thank you for explaining that. And could you tell us a little bit about where affordability is now, in a historical context?

Matthew:

Okay. Well, there’s two groups I look at in terms of the numbers that they put out relative to affordability. One, obviously is the National Association of Realtors. And their affordability index really suggested that a household in America making median income could not afford to buy a medium-priced house starting in May of last year. As we all know, that was when actually a month or so after mortgage rates started to jump massively. Now, although it does say they were technically affordable in two months later on that year, August and December. For the last five months of this year, most recent dates within July, US housing is not technically affordable. That’s across the country.

Now, there’s another index put out by the National Association of Home Builders. Now, their data, the second quarter of the year, suggests that, 40.5% of homes, both new and resale single-family homes that sold in the second quarter, were affordable. So, that’s less than half. Now, that number’s up from about 38% I believe, in the fourth quarter of last year. But it was the third-lowest level of affordability we’ve seen since they started publishing that report back in what? 2004. So, affordability, certainly in a lot of the country, not everywhere is a major constraint still. And I think that’s likely to continue to be the case.

Dave:

I think affordability comes up a lot, because people look at some of these indices, and they see what you’re showing, that indexes that measure this are at some of the lowest points that they’ve been in multiple decades. And they say, “[inaudible 00:12:23], the housing market has to correct.” This is sort of the thing, like, “Look, this is unsustainable.” Do you believe that? Do you believe that we do need to get back to, let’s say the average affordability of the last 40 years? Or are we sort of in this new normal now, where housing affordability is just lower?

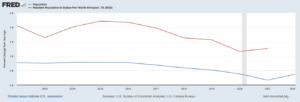

Matthew:

I think about it in terms of the ability not just for household to buy a home, but look at homeownership rates. If going back from 1965 to now on average, 65% of US households own their home, 35% rent, just that is what it is. Sorry, jump up significantly as the housing bubble was forming. And that really kind of started actually in the early 1990s. But anyway, but it really has trended back to that level. So, I don’t think it’s a case that we need to see prices drop, because of course, incomes have not, they continue to go up, that can allow prices to increase. And there’s only really been a couple of times since 1890, I think, we’ve seen a systemic decline in home values.

So, I think that that’s unlikely, but the way to address it is really rather simple, more supply. And so that supply can come from two areas. It can come from either the resale market, more people selling? Unlikely. And it can come potentially from investors. Say, “Okay, well, now’s the time for me to cash out. I’ve done very well in having single-family rentals or housing which I’ve owned as an investment.” So, Dave, it can happen that way, but quite frankly, I think it needs to come from the new construction market. We just need to build a lot more. And that in turn, more supply, still a reasonable amount of demand that can allow price growth to slow down pretty significantly, which I think is what’s needed.

James:

That’s an interesting conversation, because for investors like myself that are buying and producing housing, it also is hard to find inventory right now that you can actually mathematically make sense. We have construction costs are still… they’re down 10% roughly year-over-year it seems like, but the costs are still outrageous. Getting people to show up is a struggle still. And for investors, you still have to buy product at a certain price, whether it’s land or value-add property. And so when we’re looking at these, we’re like, “Well, okay, we have to put a certain amount of money in, so we still have to sell them for a very high price.” Which is kind of going against the affordability, right? For a lot of us investors, we have to sell it at peak because we’re giving it kind of peak type of product, totally turned.

And as the affordability starts to shrink, do you get concerned that people can’t keep up? Wage growth, they’re predicting that is going to be three to 4% for this year. And that the cost of housing is going up. And I know locally in our Seattle market, I look at what things are selling for and who the buyers are, I’m like, “Wow, they are really stretching themselves.” So, if this continues to increase, how are they going to keep up with it with wage growth kind of getting flat, or forecasting being more flat for the next 12 months?

Matthew:

But, again, you have to look back in time, which is what us economists always do. We try and figure out the future by looking behind us, what happened in the past? Historically across the country, again, going back over a hundred years, house value is got by inflation, just the way it’s always worked. In a couple of periods where that hasn’t quite worked out well, and recently obviously because of where inflation was, that reaction was different. But that is where we’ve seen it. So, ultimately, do I expect to see home values or the pace of growth slow? Yeah.

But when you think about pricing, what’s fascinating is the variability. We all talk about every market’s local, right? So, if you think about the coastal markets, do they go up by more than the Midwest of the United States? Of course they do. 15 of the least affordable housing markets in America are where? California. And so it’s quite remarkable. So, where you have a situation, that’s where we are seeing some jurisdictions, some states try and look at, “Okay, well, coastal markets or coastal states are expensive, why?” Lack of land, and also land regulation. Trying to loosen those regulatory constraints, free up more land in order to build more, because their view is, and I agree, that we have to build our way out of this issue.

Because we’re not likely to see sales increase or get back up to that six, six and a half million level. And I don’t think we’ll ever see that. If you think about it this way, mortgage rates back in 1980 were what? Almost 20%. But by a decade, it came down from 20% to 12%, to 6%, et cetera. So, as rates come down, people’s buying power increased, and that was therefore their incentive to say, “Okay, it’s time for me to sell, upsize, and move on.”

But that would require rates not just dropping back to in the fives, which I think is where they’re going to end up long-term, but continue to drop. And we’re not going to see that, otherwise money will be free, right? So, I think we really have reached that point whereby I don’t expect to see transactions increase beyond the normal demographic scenarios of people downsizing. We know that baby boomers are getting older, but quite frankly, they’re not downsizing at the speed we’d like to see for a couple of reasons. One of which is, they’ve got too much stuff, and the kids, you try and give it to them, it’ll be on eBay next week. So, they’re not downsizing. And so if they’re not downsizing, the move-up buyers, they have limited opportunity. If they’re not moving, then the first-time buyers are shot. And that is the market we really need to start addressing.

Dave:

Well, just as an anecdotal evidence, there’s a, I won’t name, a group in my family. Some boomers who sold their house to, quote, unquote, “downsize.” And they wound up buying a five-bedroom house that was bigger than their earlier one. So, I think just in my personal experience, I’ve seen that myself.

Matthew:

And they do that because they think that all the kids are going to come back and visit with them. No, they’re not.

Dave:

Honestly, that is the number one thing. They want everyone in one house at the same time. Which I understand, but that’s like a use case of maybe one time per year, or every other year.

Matthew:

Exactly.

Dave:

And now they’re taking up all this housing. That’s a whole other sociological discussion. But I just want to sort of recap what you were saying before, about rates and going down. You were saying that, “You didn’t think we’re going to get to that transaction volume of six million again.” I just want to make sure I understand. You’re basically saying that the incentive to transact as rates fell by decade, kept going down and down and down. We might never reach another point where there is as strong an incentive for people to move up, or to trade, or transact. And therefore we may have hit, at least for the foreseeable future, sort of the peak amount of home sales that are going to happen in any given month or year. Is that what you’re saying?

Matthew:

Yeah, I think you’re right. I think by my forecast, this year will probably be around 4.3 million, horrible number. Been decades since we last drove that low.

Dave:

Yeah, low.

Matthew:

Next year, I’d be surprised if we broke above five million. I think we’ll get close to it, 4.8, maybe 4.85. So, I think kind of five million is somewhere where, which we could have a certain level of comfort going forward. But more than that, again, just logically speaking, and mathematically speaking, I think I will be surprised to see us get back to those heady levels we saw. But also remember, through the pandemic, what were we doing? We were booking out of large cities, where it’d be Seattle, Los Angeles, San Francisco, and moving to Austin, Idaho, Boise, these kinds of markets. So, that really, I think pulled a lot of that demand forward already.

So, because of that, in addition to the fact that I just don’t see… We said we’re going to see rates drop over time, probably not. Anyone that thinks we’re going to get back to a 3%, 30 again, I think is going to be waiting a very long time. Because unless the Fed jumps in again, that’s the reason why we had rates sub-3 anyway. Then if that doesn’t occur, again, it just doesn’t work out because always rates have to have a relationship with the yield on 10-year treasuries. So, that means the yield on 10-year paper is going to be down around 1%, not going to happen.

James:

So, Matthew, with the sale volume being… that’s almost two million less homes being sold. You talked about earlier, that it was about 70-30 with the renters, or 65-35 with renters versus homeowners. Do you see that switching over the next 12 to 24 months, to where, as new buyers come in, they’re just more comfortable being renters because there’s no product to buy? And are we looking at an America that could go 50-50 renter versus ownership?

Matthew:

I don’t think so. And I think that most home buyers or would be home buyers… If you think about it demographically, everyone talks about millennials, right? Well, they’re getting older. As they’re aging out, a lot of them are turning 40 now. But I’m looking at, let’s say my son, Gen Z behind them. And, well, almost 70% of them believe that buying a home will be the most astute financial investment they’ll ever make. And I know the Fed, every three years, comes out with an analysis, so I’m actually waiting on the latest one, which shows the median household wealth of a homeowner household versus a renter household. And the last numbers are 2019, and if memory serves me right, I think they said the median household wealth, a homeowner household was around quarter of a million dollars, and a renter household around $6,000.

So, I can extrapolate that out to today easily, we’re looking at an owner household across America has a net wealth of probably around 320,000 renter, about eight. So, it’s the way a majority of Americans create their wealth is through long-term ownership of housing. Is it for everyone? Of course no, it’s not. But I think it is still a goal of a sizable part of our not just growing population, but aging population. I think about the young kids in college today.

James:

And it kind of shows the sign of the times. Because I remember after the 2008 crash, it was like nine, 10, and 11. The younger population had this negative stigma on owning a house, right? Their parents had just been foreclosed. Everyone was losing their properties, no one wanted real estate at all. They’re like, “That is a terrible thing to own.” And now you have these Gen Zs coming up, and they saw all this growth, and people having all this success. And I do feel like the first-time home buyer… I was actually talking to my title rep the other day, who works for a very large title company, Fidelity National Title. And he said, “50% of all transactions that they’re doing right now are first-time home buyers.”

And so I think that is been ingrained into that… If you want to make it in America, you have to buy that house. And so there’s going to be sacrifice for your house payment. But it’s crazy how much of a switch it is from watching the young buyers back then. And they were incentivized, they had that first-time home buyer credit back then, it was a great product, and people still didn’t want it. And now people are just taking the leap on where pricing is at right now.

Matthew:

I mean, education is everything, right? I think people who have watched The Big Short, people who watched a lot of these movies that came out about the housing bubble, and there are three of them which are very good. So, I think it comes down to education, and the understanding of what happened back then. The genesis of the housing bubble under Clinton in the early ’90s, all the way through Bush, et cetera, et cetera, is something which is unlikely to happen now. You think about it. Last week was the anniversary of Lehman Brothers filing a bankruptcy, which was the biggest filing in US history.

So, yes, there’s a lot of negative connotations, but I think people understand that what happened then is very unlikely to happen again. And they’re also seeing the fact that, yeah, they can own their house, guess what? They can paint their walls. It’s also forced savings. Through mortgage payment, a little piece of that pie comes out paying down principle, the tax benefits, et cetera, et cetera, all the things that everyone is aware of. So, I think they’re seeing that today and saying, “Yeah, I really think that that is the way I want to go rather than renting, and what am I doing? Paying somebody else’s mortgage.”

Dave:

There are a lot of, Matthew, analysis now though that show that if you are a renter, and actually take the… It’s sort of this hypothetical, right? So, if you had the money to make a down payment, and instead of buying a home, you rented and invested, say in the stock market and earned eight to 9% or whatever. Or perhaps invested in a rental property instead of a primary residence, that you would actually do better. And I actually do that myself. I rent and invest my money into rental properties, because you actually earn a better return in some markets. It depends on where you are. But I was just curious of your thoughts on that.

Matthew:

Let’s talk about the stock market first, or investing in equities. And I’m assuming equities, let me not talk about crypto because I’m-

Dave:

Nope.

Matthew:

I’m kind of the Charlie Munger viewer in that respect, but-

Dave:

Not for James or I at least.

Matthew:

Yeah, well, the first thing I’d say is very simple, capital gains taxes. So, you’d have to remember, as a married household, the first $500,000 in upside, in terms of the increased value of that home, tax-free.

Dave:

Tax free.

Matthew:

Now, are the equities you’re buying going to be tax-free? Guess what? No, they’re not. They’re now 30-plus percent on those. So, there is that. And again, in addition to that, you’re paying down your mortgage, et cetera, et cetera, depending on obviously how long you are there. But more than anything else, it’s shelter, and it’s yours. Now, certainly as you said, Dave, “There are people like yourselves, where it makes more sense for them to still invest in real estate.” Now, I could argue, you could still see, if you choose to sell that unit, the same issue regarding capital gains unless you made it your principal primary residence. Unless you kind of moved into it for a while.

Dave:

Right.

Matthew:

But subject to that, yeah, I think that can be for some, a viable option. Again, depending on where in the country you are. But for most people, the stock market every day, it certainly acts like a petulant child more often than not. Yes, you can see those swings, those upsides, but you also can see downside as well. And is it more likely to see a recession, therefore a contraction in equity prices? Or is it as likely you’ll see a contraction in home values?

Dave:

Yeah.

Matthew:

You’ve only seen a couple of downsides in home values.

Dave:

No. Yeah, yeah, totally. Way less volatility, for sure.

Matthew:

So, again, it’s not a one-size-fits-all scenario at all. But I think in general market, it would be those that are saying, “You’re better off if you’d invested in, I don’t know, Tesla or something.” I would say, “Yes today, maybe not six months ago.” But you could say that. But I think that’s more cherry-picking than anything else. If you just get into an index fund, okay. I’d actually never seen anyone living under a stock certificate.

James:

Yeah, so Matthew, you made kind of a good point, right? “That real estate can be a lot less volatile and more dependable than the stock market,” which I truly do believe. I seem to lose money on stock market, and crypto, and anything else besides real estate. Not that you can’t lose money in real estate too. So, I do believe that. But in the climate that we’re in right now, there’s obviously risk in every type of asset class. What should we be wary of, as real estate investors? Like right now, we’re out trying to buy properties to sell them for profit, keep them as rental properties. What should investors be looking out for right now, as they’re looking at buying that next investment? Because we’re all eager to buy, but we’re a little bit cautious right now.

Matthew:

I think that there’s some things which actually you gentlemen have already mentioned. And that is the fact that, is it a market that you can buy a house, and knowing that the rent you’ll be able to achieve having bought it? Is there a yield there? I mean, there’s a reason why institutional investors, obviously not mom-and-pop investors, which although that comprises a vast majority of the market, have they been pulling back significantly? Absolutely. I mean, they’re still active in a couple of markets, but generally not.

So, I would say that the first thing to do is, you know what you’re borrowing, you know what your payment’s going to be, your rents are going to be. Does that make sense today or does it not? And so I think that’s one of the first things. Secondly, I’d look at the market. And is it a market that you could potentially see some additional price erosion from where we are today? And I think in the past, I guess, [inaudible 00:28:48] you’ve talked about markets which are still of a concern, Austin, Texas is obviously one. I’d say Boise, Idaho is another one.

James:

We love beating up on those markets too.

Matthew:

Everyone does right now, quite frankly. It really is kind of scary. But there are markets which, and certainly Boise, which go back 15, 20 years, no one really wanted to be there. But it’s funny, it’s an area of last time… I go there every year now. I had to give a speech. And it reminds me of a scaled-down gas stamp district in San Diego. It’s kind of hip, it’s got some good restaurants, and distilleries, and breweries. It’s got the most amazing convention center that’s built by a company, and then given to the city for nothing. Great regional airport. So, I think it’s got some good things going to it. However, a couple of years ago, you could have bought a nice house for a bit north of quarter of a million dollars. Today, we’re talking north of $600,000. And that again is because of that massive flight out of some of the more expensive markets, not just here in the Northwest, but very specifically California.

So a couple of things that I just mentioned, one of which is there a yield? Does it make financial sense, or is it costing you money? And that would therefore mean, start looking at high property tax states and these kinds of things. Is it a market that potentially can see some further price erosion, then you might want to wait before you jump in? So, those I think are the two things that stick out to me. But in terms of being an investor and where prices are, we started out talking about affordability. We are creating a lot, a forced renter households that would like to buy, they just can’t. And not just the young kids that weren’t quite ready to move out of their apartment, they hadn’t got a down payment ready. All they’ve done is see prices go up and mortgage rates double.

But you look at a lot of families. Everyone assumes that if you’re a family, then you rent an apartment. No, you don’t, you rent a single-family home. And so these are people that might want to get their foot on the first rung of the ladder, just can’t make it work. They need somewhere to live. And so, again, shelter at the long-term, is always going to be a good investment. But the worry, again, comes back to affordability. So, I’d say just look at the markets in which you’re choosing or you’re thinking about investing in. Don’t bite off more than you can chew, don’t overleverage. All the things I would say to somebody who’s looking to buy a home for themselves.

Dave:

Yeah, it’s really a lot of the same fundamentals that we were saying. Matthew, before we get out of here, this has been a fascinating conversation, and thank you. Is there anything else you think that our audience, primarily of those small mom-and-pop investors you just talked about, should know about the market, or factor into their decision-making over the next year?

Matthew:

Yeah, I would say that when it comes to… Everyone’s looking at mortgage rates, we started talking about it. But from my end, I’m talking about it. Are we going to see them continue to skyrocket? I think that that is highly unlikely. But as they come down, and I expect they will. And in fact, I think we’ll be down probably in the mid-fives by the latter part of next year. Just calm down, it’s going to be okay. We’re just in a very unique situation right now. The Fed’s trying to cool inflation, and in some respects, it’s working. But the resilience of the US economy has been remarkable. That is not a good thing in terms of investors or indeed analysts like myself who try and forecast mortgage rates, because we should be slowing down a bit more, but that is not the case.

However, we could overshoot, or they could overshoot, keep rates higher longer, that could lead to a recession. Not a good feeling for any of us, however, good for mortgage rates, because they will drop faster than I’m anticipating. So, I think really it is, we are in a situation now coming out of COVID, that we hadn’t seen before in a century. No one wrote the book about it, about what was going to happen. The world is a very different place. So, I think we just need to figure that out, and let’s let the seas calm down somewhat, which I think they will. But do I always think that in the right circumstance, again, not over-leveraging yourself, is owning real estate as an investment or as somewhere in which you live a good investment? Historically, it has been. And again, as an economist, I tend to look at history, not to forecast the future, I do not see that changing. But just be patient, in time, things will settle down.

Dave:

All right, great. Well, thank you so much, Matthew, for being here. We really appreciate it. If people want to follow your research, check out your incredible in-depth reports, where should they do that?

Matthew:

Well, thank you. So, Instagram, Facebook, and Twitter. It’s mgardnerecon. So, mgardner, G-A-R-D-N-E-R, econ, E-C-O-N. LinkedIn, mjdgardner. And that’s where we put out all of our analysis.

Dave:

All right. Well, thanks again for being here. We really appreciate it.

Matthew:

David, James, pleasure.

James:

Yeah, thanks, Matthew.

Matthew:

You’re welcome.

Dave:

Well, I see why you wanted to have Matthew come on the show here, James. What’d you think of our conversation?

James:

Oh, I loved it. I mean, it was great for him to just talk about the affordability, because we’re all worried about this. As investors, are we going to get to a price point where no one’s going to buy or no one’s going to rent? And so it was just good to get some perspective on it. But being a Pacific Northwest guy, we listen to Matthew Gardner all the time as the chief economist for Windermere. And every time he speaks, it’s always a little piece of gold.

Dave:

I mean, there was a lot in there. And I think what he was talking about in terms of affordability really extends beyond even the expensive state. Quote, unquote, “expensive areas,” like obviously where you are in Seattle, we talked a lot about California. But most of the country now falls under the quote, unquote, “unaffordable area.” Even the places people are moving in the southeast in Florida and Tennessee, and in a lot of areas of Texas, the median income cannot afford the median price home in those places.

And I think that, for good reason, has… People have point to that and said, “Hey, things have to come back to normal.” But according to Matthew, that’s not necessarily true. As long as supply is as low as it is, it apparently can stay up. And I think that’s a really interesting thing that I’ve debated with many people, because no one knows for sure. But I think Matthew brought us some really interesting perspectives on this, and whether or not we’re going to have to see an improvement in affordability in the near future here.

James:

And after we were getting done talking, I mean, for me, in the back of my mind, I was like, “I think rent has some more growth in it.”

Dave:

You do?

James:

For some reason, it’s like if pricing keeps going up and people seem to just be making this payment, and sales are so far down, you’re going to have to rent in the short term until you find that house. And so it could push rents up a little bit more.

Dave:

Yeah, I think it’s certain markets. I just feel like there’s this big pull-forward, and household formation is just slowing down. All these people did the COVID breakup basically, like roommates, everyone wanted to go their own way. And so it just created more renter households, and that fueled a lot of the rent growth. And I don’t think it’s necessarily going backwards, but I think that all that juice that was in rent for a while might be slowing down. But we’ll see. I don’t necessarily think… Rents are sticky, so I don’t think they’re going to slide a lot. But I personally, if I’m looking at deals right now, I underwrite pretty slow rent growth. Are you in your deals putting in rent growth, or is this a revelation you had today?

James:

No, very minimum. I think anything we’re looking at, we’re being very conservative. Whether it’s a value rent growth, we’re sticking it pretty flat. But there’s certain areas that I’m watching and I’m like, “Well, there could be some rent growth.” It really comes down to what is the cost for rent versus buying? And certain areas are way out of whack. And so we’re still underwriting with low growth, but I think the upside’s there.

Dave:

Yeah, exactly. If you underwrite, find a good deal with no rent growth and then it grows, then it’s good to be wrong.

James:

Yes.

Dave:

All right. Well, thanks a lot, man. We appreciate you being here, and for recommending this great guest to us. Thank you all for listening. We appreciate you, and we’ll see you for the next episode of On The Market. On The Market is created by me, Dave Meyer, and Kailyn Bennett. Produced by Kailyn Bennett, editing by Joel Esparza and OnyxMedia. Research by Pooja Jindal, copywriting by Nate Weintraub. And a very special thanks to the entire BiggerPockets team. The content on the show On The Market are opinions only. All listeners should independently verify data points, opinions, and investment strategies.

Watch the Episode Here

Help Us Out!

Help us reach new listeners on iTunes by leaving us a rating and review! It takes just 30 seconds and instructions can be found here. Thanks! We really appreciate it!

In This Episode We Cover:

- The SINGLE factor that’s causing so much unaffordability in the housing market

- Home price updates and a surprising statistic about homes for sale

- Mortgage rate predictions and whether or not we’ll see them fall next year

- “Forced renter household” formation and whether America will become a renter nation

- Crucial advice for ANYONE who’s buying real estate in 2023 (and if you should wait)

- And So Much More!

Links from the Show

Connect with Matthew

Interested in learning more about today’s sponsors or becoming a BiggerPockets partner yourself? Email .

Note By BiggerPockets: These are opinions written by the author and do not necessarily represent the opinions of BiggerPockets.

- SEO Powered Content & PR Distribution. Get Amplified Today.

- PlatoData.Network Vertical Generative Ai. Empower Yourself. Access Here.

- PlatoAiStream. Web3 Intelligence. Knowledge Amplified. Access Here.

- PlatoESG. Carbon, CleanTech, Energy, Environment, Solar, Waste Management. Access Here.

- PlatoHealth. Biotech and Clinical Trials Intelligence. Access Here.

- Source: https://www.biggerpockets.com/blog/on-the-market-145

- :has

- :is

- :not

- :where

- $UP

- 000

- 1

- 10

- 11

- 12

- 12 months

- 15%

- 2%

- 20

- 20 years

- 2008

- 2019

- 2023

- 23

- 24

- 28

- 30

- 300

- 320

- 35%

- 40

- 40th

- 500

- 7

- 8

- a

- ability

- Able

- About

- About Crypto

- about IT

- above

- absolutely

- According

- Achieve

- across

- active

- acts

- actually

- addition

- Additional

- address

- addressing

- advice

- advise

- advising

- affordable

- affordable housing

- After

- again

- against

- agents

- aggressively

- Aging

- ago

- airport

- All

- All Transactions

- allow

- allows

- almost

- already

- also

- Although

- always

- am

- amazing

- america

- American

- Americans

- amount

- an

- analysis

- analyst

- Analysts

- analyze

- and

- Angeles

- Anniversary

- Another

- anticipating

- any

- anyone

- anything

- Apartment

- Apple

- appreciate

- ARE

- AREA

- areas

- argue

- around

- AS

- asset

- asset class

- Association

- assumes

- assumptions

- At

- attract

- audience

- AUGUST

- austin

- author

- average

- aware

- away

- Baby

- back

- background

- Bad

- Bankruptcy

- based

- Basically

- BE

- beautiful

- because

- become

- becoming

- been

- before

- behind

- being

- believe

- benefits

- besides

- BEST

- Better

- between

- Beyond

- Big

- bigger

- Biggest

- Billion

- Bit

- book

- booking

- border

- born

- borrow

- Borrowing

- both

- bought

- brand

- bring

- Bringing

- Broke

- brokerage

- brokers

- brothers

- brought

- bubble

- build

- builders

- built

- but

- buy

- BUYER..

- buyers

- Buying

- buying power

- by

- CAKE

- california

- came

- CAN

- cannot

- capital

- case

- Cash

- Cash Out

- caught

- Cause

- causing

- cautious

- Center

- Century

- certain

- certainly

- certificate

- changing

- Charlie

- Charlie Munger

- check

- chief

- child

- Choose

- choosing

- circumstance

- Cities

- City

- class

- classified

- client

- clients

- Climate

- Climbing

- Close

- Coast

- coastal

- Collapse

- College

- come

- comes

- comfort

- comfortable

- coming

- Companies

- company

- completing

- comprises

- Concern

- concerned

- confusion

- conservative

- constraints

- construction

- content

- context

- continue

- continued

- continues

- continuing

- contraction

- Convention

- Conversation

- Cool

- copywriting

- correct

- Cost

- Costs

- could

- country

- Couple

- course

- cover

- Covid

- Crash

- crazy

- create

- created

- Creating

- credit

- crypto

- curious

- data

- data points

- Dates

- Dave

- day

- deal

- Deals

- decade

- decades

- December

- Deciding

- Decision Making

- Decline

- delivers

- Demand

- demographic

- dependable

- Depending

- depends

- developers

- Development

- DID

- Diego

- different

- DIG

- direction

- discussion

- Display

- district

- do

- does

- Doesn’t

- doing

- dollars

- done

- Dont

- doom

- double

- doubled

- down

- downside

- downsides

- downsizing

- dramatically

- Drink

- driver

- Drop

- Dropping

- E&T

- eager

- Earlier

- Early

- earn

- earned

- easily

- easy

- eBay

- Economic

- Economics

- Economist

- economists

- economy

- editing

- Education

- either

- else

- Else’s

- end

- energy

- Entire

- entities

- episode

- equal

- Equities

- equity

- essence

- estate

- Ether (ETH)

- Even

- EVER

- Every

- every day

- everybody

- everyone

- everyone’s

- everything

- everywhere

- evidence

- exactly

- excellent

- excited

- expect

- expectation

- expensive

- experience

- expert

- explaining

- extends

- fact

- factor

- factors

- Factual

- Fall

- Falls

- families

- family

- far

- fascinating

- faster

- Favorite

- Fed

- feel

- few

- fidelity

- Figure

- Filing

- financial

- Find

- finding

- First

- five

- flat

- flight

- florida

- follow

- Foot

- For

- For Investors

- Forecast

- foreseeable

- forever

- formal

- formation

- Former

- Forward

- found

- four

- Fourth

- Francisco

- Free

- from

- Fuel

- fueled

- fund

- Fundamentals

- funny

- further

- future

- Gains

- gardner

- GAS

- gather

- Gen

- Gen Z

- General

- generally

- Genesis

- get

- getting

- gift

- Give

- given

- gives

- Giving

- Go

- goal

- Goes

- going

- Gold

- Golden

- good

- got

- Governments

- great

- Group

- Group’s

- Grow

- Growing

- Grows

- Growth

- Guard

- Guest

- guests

- Guy

- had

- Half

- happen

- happened

- Hard

- hate

- Have

- having

- he

- head

- hear

- hearing

- hedging

- help

- here

- Hidden

- High

- high-level

- higher

- highly

- him

- his

- historical

- historically

- history

- Hit

- Home

- Homes

- hoping

- host

- House

- household

- households

- housing

- housing market

- How

- However

- HTTPS

- huge

- hundred

- i

- I’LL

- identify

- if

- Impact

- Improbable

- improvement

- in

- in-depth

- Incentive

- incentivized

- inches

- Income

- Increase

- increased

- Increases

- increasing

- incredible

- independently

- index

- indexes

- Indices

- inflation

- information

- inputs

- instead

- Institutional

- institutional investors

- instructions

- interest

- Interest Rates

- interesting

- into

- introduce

- inventory

- Invest

- invested

- investing

- investment

- investment portfolio

- investor

- Investors

- invitation

- involved

- issue

- IT

- ITS

- iTunes

- james

- jerome

- jerome powell

- joined

- joining

- jpg

- July

- jump

- jumps

- jurisdictions

- just

- Keep

- keeping

- kept

- kids

- Kind

- Kingdom

- Know

- Knowing

- knows

- Lack

- ladder

- Land

- large

- large-scale

- Last

- Last Year

- Late

- later

- latest

- lead

- Leap

- learning

- least

- leaving

- Lehman

- less

- let

- Level

- levels

- LG

- like

- likely

- Limited

- listener

- Listening

- little

- live

- living

- local

- locally

- location

- London

- Long

- long time

- long-term

- longer

- Look

- looking

- LOOKS

- los

- Los Angeles

- lose

- losing

- Lot

- love

- loved

- loves

- Low

- lower

- lowest

- loyal

- made

- major

- Majority

- make

- MAKES

- Making

- man

- managed

- many

- many people

- Market

- Markets

- massive

- massively

- math

- mathematically

- Matter

- matthew

- May..

- maybe

- me

- mean

- means

- measure

- Memory

- mentioned

- Meyer

- midwest

- might

- Millennials

- million

- million dollars

- mind

- mine

- minimum

- minute

- misunderstanding

- money

- Month

- months

- more

- morning

- Mortgage

- most

- mostly

- move

- moved

- Movies

- moving

- much

- multiple

- my

- myself

- name

- National

- nationally

- Nationwide

- Near

- nearly

- necessarily

- Need

- needed

- needs

- negative

- net

- never

- New

- New Construction

- next

- next week

- nice

- niche

- night

- no

- None

- normal

- normally

- North

- nothing

- now

- number

- numbers

- occur

- of

- off

- offices

- often

- Okay

- Old

- older

- on

- ONE

- only

- open

- opened

- Opinions

- opportunities

- Opportunity

- Option

- or

- order

- Other

- otherwise

- our

- out

- over

- own

- owned

- owner

- ownership

- Oxford

- Pace

- Pacific

- paint

- pandemic

- Paper

- parents

- part

- partner

- past

- patient

- paying

- payment

- payments

- Peak

- People

- people’s

- per

- percent

- percentage

- perfect

- perhaps

- periods

- personal

- Personally

- perspective

- perspectives

- piece

- Place

- Places

- plato

- Plato Data Intelligence

- PlatoData

- player

- please

- pleasure

- podcast

- Podcasts

- Point

- points

- population

- portfolio

- portfolios

- potentially

- Powell

- power

- predicting

- presence

- pretty

- price

- Prices

- pricing

- primarily

- primary

- Principal

- principle

- probably

- Produced

- producing

- Product

- Profit

- profits

- promise

- properties

- property

- protected

- provides

- Publishing

- pulling

- Push

- put

- Putting

- Quarter

- question

- quickly

- quote

- raised

- rapidly

- Rate

- Rates

- rather

- rating

- reach

- reached

- reaction

- Read

- Reading

- ready

- real

- real estate

- really

- reason

- reasonable

- reasons

- recap

- recent

- recently

- recession

- recommended

- recommending

- refusing

- regarding

- regional

- regularly

- Regulation

- regulatory

- relationship

- relative

- remarkable

- remember

- Rent

- rentals

- renters

- repair

- report

- Reports

- represent

- represented

- require

- research

- Residence

- resilience

- respect

- respects

- Restaurants

- return

- revelation

- review

- Ride

- right

- Rise

- Risk

- road

- Rockstar

- Rolling

- roughly

- round

- royal

- Royal Family

- sacrifice

- Said

- sale

- sales

- same

- San

- San Diego

- San Francisco

- Savings

- saw

- say

- saying

- scenario

- scenarios

- School

- Seattle

- Second

- second quarter

- seconds

- see

- seeing

- seem

- seems

- seen

- sell

- Selling

- sense

- seriously

- serves

- settle

- Share

- Shelter

- Short

- shot

- should

- show

- showing

- Shows

- side

- sign

- significantly

- Simple

- since

- sister

- situation

- SIX

- Six months

- sizable

- skyrocket

- Slide

- slow

- Slowing

- small

- smart

- So

- so Far

- sold

- solution

- SOLVE

- some

- Someone

- something

- somewhat

- somewhere

- son

- southeast

- speaking

- Speaks

- special

- specific

- specifically

- speech

- speed

- spent

- Sponsors

- Spotify

- Staff

- start

- started

- Starting

- starts

- State

- States

- stats

- stay

- steady

- Stick

- sticking

- sticky

- Still

- stock

- stock market

- strategies

- strong

- Struggle

- subject

- success

- such

- Suggests

- Super

- supply

- Supporting

- sure

- surprised

- Swings

- Switch

- systemic

- Take

- takes

- taking

- Talk

- talking

- Talks

- tax

- Taxes

- team

- technically

- tell

- tennessee

- term

- terms

- terrible

- Tesla

- texas

- than

- thank

- thanks

- that

- The

- The Big Short

- the Fed

- The Future

- the information

- the United Kingdom

- The West

- the world

- their

- Them

- themselves

- then

- There.

- therefore

- These

- they

- thing

- things

- think

- Thinking

- Thinks

- this

- this year

- those

- though?

- thought

- three

- Through

- time

- times

- Title

- to

- today

- today’s

- too

- took

- top

- topic

- TOTALLY

- Tower

- trade

- transact

- transaction

- Transactions

- Transcript

- Treasuries

- Trends

- true

- truly

- try

- trying

- TURN

- Turned

- Turning

- two

- type

- types

- ultimate

- Ultimately

- under

- understand

- understanding

- understands

- underwriting

- unique

- unit

- United

- United Kingdom

- United States

- unlikely

- unsustainable

- until

- Updates

- upon

- Upside

- us

- US economy

- US Housing

- use

- use case

- using

- value

- value-add

- Values

- Vast

- verify

- Versus

- very

- viable

- Video

- View

- Visit

- volatile

- Volatility

- volume

- wage

- wait

- Waiting

- want

- wanted

- wanting

- wants

- was

- watching

- Way..

- we

- Wealth

- week

- welcome

- WELL

- went

- were

- West

- Western

- What

- What is

- whatever

- when

- whether

- which

- while

- WHO

- whole

- why

- will

- with

- within

- Word

- Work

- work out

- worked

- working

- works

- world

- worried

- worry

- worth

- would

- write

- written

- Wrong

- wrote

- year

- years

- yes

- yet

- Yield

- you

- young

- Younger

- Your

- yourself

- youtube

- zephyrnet