Climate Week NYC is in full force, so let’s explore one of the hardest-to-abate areas of our economy — maritime shipping.

DNV recently released its annual Maritime Forecast to 2050 report, looking at the shipping market’s decarbonization journey in 2023. I dove into this 74-page report and identified four key findings.

To get further insight into the report’s findings, I spoke with Antony DSouza, regional president of maritime at DNV. So without further ado, let’s set sail.

1. There’s more to decarbonization than the fuel

Much of the report discusses how the maritime industry’s pathway to decarbonization is intrinsically driven by regulations. More on regulations below at No. 4, but it’s important to consider them in tandem with shipping technologies and fuels because carriers are increasingly pushed to meet stronger emissions standards.

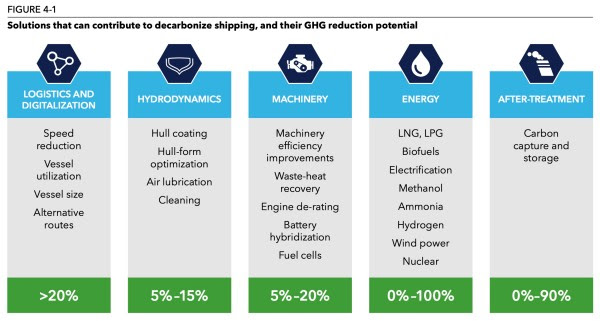

The energy source for ships is a focal point of decarbonization as many across the industry explore alternative fuels such as ammonia, hydrogen, green methanol and even wind power.

![]()

![]()

![]()

![]()

Recent excitement about Maersk unveiling the world’s first vessel using green methanol and Cargill chartering a ship supported by wind energy showcase the potential of what can be if we get maritime decarbonization right.

However, DSouza points out that there will be a bottleneck on available alternative fuels, especially in the near term as other industries such as aviation potentially win out on securing more of the supply for some fuel types.

Thus, industry players must not discredit the many other ways of decarbonization. The report highlights several of these methods — which have varying degrees of impact — such as improving the hydrodynamics of the ship and more efficient onboard machinery. For example, machinery improvements can support decarbonization in a range from 5 to 20 percent.

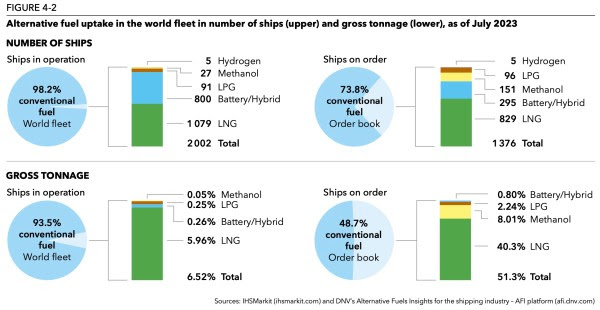

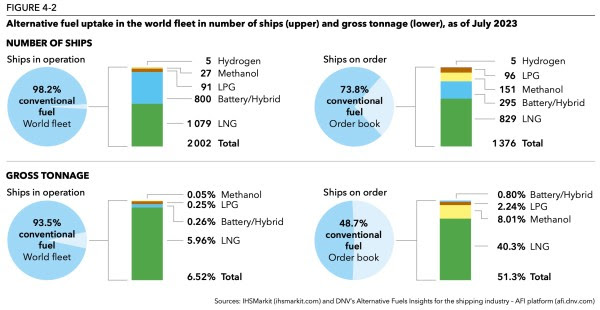

2. LNG ships still dominate the order books

While there are many ways to advance decarbonization, it’s clear the biggest piece of the pie comes from using alternative fuels on ships. Liquid natural gas (LNG) ships continue to dominate the order books. Out of a total of 1,376 ships on order, 829 are LNG with the second-most dominant being battery/hybrid at 295. Based on gross tonnage, LNG represents 40.3 percent of ships on order.

![]()

![]()

![]()

![]()

DSouza shared how the industry truly sees LNG as a transition fuel to cleaner options such as ammonia and methanol. Other reports have shown that converting ships from LNG to ammonia or methanol is cost-effective and feasible. DSouza pointed out that the maritime industry is in a unique position because there isn’t one future fuel for ships to run on. Thus, industry players have settled on LNG as a full-fledged transition fuel to lead to cleaner options.

The report also highlights that a transition period in maritime is perhaps needed more than in some other industries because the industry needs sufficient training capacity for safely operating ships on alternative fuels. A lack of clarity surrounding alternative fuel options and decarbonization trajectories is partially contributing to the challenge of how and on what to train seafarers.

3. The cargo owner’s role in cleaner maritime

The report notes that shipping companies have started responding to increasing demand from cargo owners for cleaner services to reduce their Scope 3 emissions. Phrased as “net-zero emission services,” DNV suspects this trajectory and these offerings will continue upward to meet cargo owner demands.

“It [the transition to net-zero shipping] is going to be expensive… but the question is, whether the end user is willing to put their money where their mouth is,” DSouza said. In this case, I see end users as either the cargo owners who will have to help pay for these increased services and absorb those costs or the actual customers who will face increased costs for their online purchases.

One example of the cargo owner’s role in maritime decarbonization recently came from the Zero Emission Maritime Buyers Alliance (ZEMBA). Amazon and 20 other major global companies launched a tender, inviting shipping lines to submit bids for zero-emission shipping services.

DSouza shared how efforts of groups such as Cargo Owners for Zero Emission Vessels, also known as coZEV, and ZEMBA are a good start, but questions remain as to how much the customer is willing to pay for increased costs of goods.

Green shipping corridors are also discussed heavily throughout the report, along with book-and-claim programs as mechanisms to help advance decarbonization technologies across maritime.

4. Regulations and well-to-wake emissions

Regulations and policies remain the key drivers of decarbonization across the shipping industry, according to the DNV report.

The U.S. and China are laggards across maritime decarbonization compared with the European Union. The report states that it’s unlikely the U.S. will impose additional requirements anytime soon or set clear targets on international ships entering U.S. ports beyond what it has done tangentially — through actions such as reentering the Paris Climate Agreement, its supportive work through the First Movers Coalition on green shipping corridors and bold laws such as the Inflation Reduction Act of 2022.

As for the EU, ambitious legislation such as the Emissions Trading System and eFuelEU Maritime set specific environmental requirements on ships. FuelEU Maritime is notable for its focus on well-to-wake emissions, something DNV expects more regulations to incorporate. The FuelEU Maritime requirements take effect in 2025 and become more stringent over time, starting with a 2 percent reduction in the greenhouse gas intensity of the fuel, increasing to an 80 percent reduction by 2050.

![]()

![]()

![]()

![]()

And, should an alternative fuel not meet the criteria and certification requirements of the EU’s Renewable Energy Directive, it’s then considered equal to the least favorable fossil pathway.

Finally, one cannot discuss regulations in maritime without mentioning the International Maritime Organization’s recent meeting in July, which set new targets for maritime decarbonization including a 20 percent reduction in emissions by 2030, 70 percent by 2040 and an ultimate goal of net zero by 2050. The regulations will go into effect around mid-2027. These changes also included language on measuring the well-to-wake emissions of alternative fuels.

- SEO Powered Content & PR Distribution. Get Amplified Today.

- PlatoData.Network Vertical Generative Ai. Empower Yourself. Access Here.

- PlatoAiStream. Web3 Intelligence. Knowledge Amplified. Access Here.

- PlatoESG. Carbon, CleanTech, Energy, Environment, Solar, Waste Management. Access Here.

- PlatoHealth. Biotech and Clinical Trials Intelligence. Access Here.

- Source: https://www.greenbiz.com/article/4-takeaways-surface-dnvs-maritime-forecast-2050-report

- :has

- :is

- :not

- :where

- $UP

- 1

- 15%

- 20

- 2022

- 2023

- 2025

- 2030

- 2050

- 23

- 40

- 7

- 70

- 80

- 9

- a

- About

- According

- across

- Act

- actions

- actual

- Additional

- advance

- Agreement

- Alliance

- along

- also

- alternative

- Amazon

- ambitious

- Ammonia

- an

- analysis

- and

- annual

- ARE

- areas

- around

- article

- AS

- At

- available

- aviation

- based

- BE

- because

- become

- being

- below

- Beyond

- Biggest

- bold

- Books

- but

- buyers

- by

- CA

- came

- CAN

- cannot

- Capacity

- Cargill

- Cargo

- carriers

- case

- Center

- Certification

- challenge

- Changes

- China

- clarity

- cleaner

- clear

- click

- Climate

- coalition

- comes

- Companies

- compared

- Consider

- considered

- continue

- contribute

- contributing

- converting

- cost-effective

- Costs

- criteria

- customer

- Customers

- data

- decarbonization

- Demand

- demands

- dialogue

- discuss

- discussed

- dominant

- dominate

- done

- dove

- driven

- drivers

- economy

- effect

- efficient

- efforts

- either

- Electric

- emission

- Emissions

- end

- energy

- entering

- environmental

- equal

- equitable

- especially

- Ether (ETH)

- EU

- European

- european union

- Even

- example

- Excitement

- expects

- explore

- Face

- favorable

- feasible

- findings

- First

- FLEET

- focal

- Focus

- For

- Force

- Forecast

- fossil

- four

- Free

- from

- Fuel

- fuels

- full

- full-fledged

- further

- future

- GAS

- get

- Global

- Go

- goal

- going

- good

- goods

- graphic

- great

- Green

- greenhouse gas

- gross

- Group’s

- Have

- heavily

- help

- highlights

- How

- http

- HTTPS

- hydrogen

- i

- identified

- if

- Impact

- important

- impose

- improvements

- improving

- in

- Including

- incorporate

- increased

- increasing

- increasingly

- industries

- industry

- industry’s

- inflation

- insight

- International

- into

- intrinsically

- inviting

- IT

- ITS

- journey

- jpg

- July

- Key

- known

- Lack

- laggards

- launched

- Laws

- lead

- least

- Legislation

- let

- lines

- Liquid

- lng

- looking

- machinery

- Maersk

- major

- many

- Maritime

- measuring

- mechanisms

- Meet

- meeting

- Methanol

- methods

- money

- more

- more efficient

- mouth

- move

- Movers

- much

- must

- Natural

- Natural Gas

- Near

- needed

- needs

- net

- net-zero

- New

- Newsletter

- no

- node

- notable

- Notes

- NYC

- Oct

- of

- Offerings

- on

- Onboard

- ONE

- online

- online purchases

- operating

- Options

- or

- order

- order books

- Other

- our

- out

- over

- owner

- owners

- paris

- pathway

- Pay

- percent

- perhaps

- period

- piece

- Place

- plato

- Plato Data Intelligence

- PlatoData

- players

- Point

- points

- policies

- ports

- position

- potential

- potentially

- power

- presentation

- president

- purchases

- pushed

- put

- question

- Questions

- range

- recent

- recently

- reduce

- reduction

- regional

- regulations

- released

- remain

- Renewable

- renewable energy

- report

- represents

- Requirements

- responding

- right

- Role

- Run

- s

- safely

- Said

- San

- San Jose

- scope

- securing

- see

- sees

- Services

- set

- Settled

- several

- shared

- Shipping

- ships

- should

- showcase

- shown

- sign

- sizes

- So

- Solutions

- some

- something

- Soon

- Source

- specific

- standards

- start

- started

- Starting

- States

- Still

- stronger

- submit

- such

- sufficient

- supply

- support

- supportive

- Surface

- Surrounding

- sustainable

- system

- Take

- Takeaways

- taking

- Tandem

- targets

- Technologies

- Tender

- term

- than

- that

- The

- their

- Them

- then

- There.

- These

- this

- those

- Through

- throughout

- Thus

- time

- timeline

- to

- Total

- Trading

- trading system

- Train

- Training

- trajectory

- transition

- transport

- transportation

- truly

- types

- u.s.

- ultimate

- union

- unique

- unlikely

- upward

- User

- users

- using

- Vessel

- vessels

- want

- ways

- we

- week

- What

- whether

- which

- WHO

- will

- willing

- win

- wind

- wind power

- with

- without

- Work

- world

- world’s

- zephyrnet

- zero