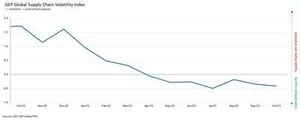

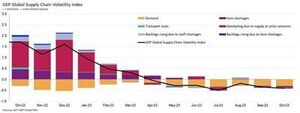

The GEP Global Supply Chain Volatility Index — the indicator tracking demand conditions, shortages, transportation costs, inventories and backlogs based on a monthly survey of 27,000 businesses — decreased again in October to -0.41, from -0.35 in September, indicating a 7th successive month of rising spare capacity across the world’s supply chains.

Additionally, the extent to which supplier capacity went underutilised was even greater than in September and August. Coupled with October’s downturn in demand for raw materials, components and commodities, this shows rising slack in global supply chains.

“While the shrinking of global suppliers’ order books is not worsening, there are no signs of improvement,” explained Jamie Ogilvie-Smals, vice president, consulting, GEP. “The notable increase in supplier capacity in Asia, which was driven by China, provides global manufacturers with greater leverage to drive down prices and inventories in 2024.”

A key finding from October’s report was the strongest rise in excess capacity across Asian supply chains since June 2020. Sustained weakness in demand, coupled with falling pressures on factories in Asia, indicates that the global manufacturing recession has further to run. With the exception of India, which continues to perform strongly, large economies in the region, such as Japan and China, are losing momentum.

Suppliers in Europe continue to report the largest level of spare capacity. In fact, the lower levels in GEP’s supply chain index for the continent have only been seen during the global financial crisis between 2008 and 2009. They highlight sustained weakness in economic conditions across the continent. Western Europe, particularly Germany’s manufacturing industry, is a key driver behind the region’s deterioration.

נקודת אור יחסית היא צפון אמריקה, שבה יש לרשתות האספקה קיבולת עודפת, אך במידה הרבה פחות מאשר במקומות אחרים, שכן כלכלת ארה"ב ממשיכה להציג את חוסנה, בניגוד מוחלט לאירופה.

אוקטובר 2023 ממצאים מרכזיים

Demand: Demand for raw materials, components and commodities remains depressed, although the downturn seems to have stabilised. There are still no signs of conditions improving, however, as global purchasing activity fell again in October at a pace similar to what we’ve seen since around mid-year.

Demand: Demand for raw materials, components and commodities remains depressed, although the downturn seems to have stabilised. There are still no signs of conditions improving, however, as global purchasing activity fell again in October at a pace similar to what we’ve seen since around mid-year.- מלאים: עם ירידה בביקוש, הנתונים שלנו מראים עוד חודש של הוצאת מלאי על ידי עסקים גלובליים, מה שמסמן מאמצים לשימור תזרים המזומנים.

- מחסור בחומר: הדיווחים על מחסור בפריטים נותרו בשפל מאז ינואר 2020.

- Labour shortages: Shortages of workers are not impacting global manufacturers’ capacity to produce, with reports of backlogs due to inadequate labour supply running at historically typical levels.

- Transportation: Global transportation costs held steady with September’s level, although oil prices have declined in recent weeks.

תנודתיות בשרשרת האספקה האזורית

-

צפון אמריקה: המדד ירד ל-0.34, מ-0.30. זה נשאר הרבה יותר רך מהממוצע העולמי וממשיך להציע את ארה"ב. הכלכלה מוכנה לנחיתה רכה.

- אירופה: המדד עלה ל-0.90, מ-1.01, אך עדיין נשאר ברמה המעידה על שבריריות כלכלית ניכרת.

- בריטניה: המדד עלה מעט ל-0.93, מ-0.98. עם זאת, הנתונים מצביעים על עלייה משמעותית בקיבולת העודפת אצל ספקים לשווקים בבריטניה.

- Asia: Notably, the index dropped to -0.38, from -0.20, highlighting the biggest rise in spare supplier capacity in Asia since June 2020 as the region’s resilience fades.

- הפצת תוכן ויחסי ציבור מופעל על ידי SEO. קבל הגברה היום.

- PlatoData.Network Vertical Generative Ai. העצים את עצמך. גישה כאן.

- PlatoAiStream. Web3 Intelligence. הידע מוגבר. גישה כאן.

- PlatoESG. פחמן, קלינטק, אנרגיה, סביבה, שמש, ניהול פסולת. גישה כאן.

- PlatoHealth. מודיעין ביוטכנולוגיה וניסויים קליניים. גישה כאן.

- מקור: https://www.logisticsit.com/articles/2023/11/21/supply-chains-worldwide-remain-significantly-underutilised-gep-global-supply-chain-volatility-index

- :יש ל

- :הוא

- :לֹא

- :איפה

- 000

- 01

- 121

- 20

- 2008

- 2020

- 2023

- 2024

- 27

- 30

- 300

- 35%

- 41

- 7th

- 90

- 98

- a

- לרוחב

- פעילות

- שוב

- למרות

- אמריקה

- ו

- אחר

- ARE

- סביב

- AS

- אסיה

- אסיה

- At

- אוגוסט

- מְמוּצָע

- מבוסס

- היה

- מאחור

- בֵּין

- הגדול ביותר

- ספרים

- בָּהִיר

- עסקים

- אבל

- by

- קיבולת

- שרשרת

- שרשראות

- סין

- סחורות

- רכיבים

- תנאים

- רב

- ייעוץ

- יבשת

- להמשיך

- ממשיך

- לעומת זאת

- עלויות

- יחד

- משבר

- נתונים

- ירד

- דרישה

- לְהַצִיג

- מטה

- מטה

- נהיגה

- מונע

- נהג

- ירד

- ראוי

- בְּמַהֲלָך

- כַּלְכָּלִי

- תנאים כלכליים

- כלכלות

- כלכלה

- מַאֲמָצִים

- במקום אחר

- Ether (ETH)

- אירופה

- אֲפִילוּ

- יוצא מן הכלל

- עודף

- מוסבר

- מידה

- עובדה

- מפעלים

- דועך

- נפילה

- כספי

- משבר כלכלי

- מציאת

- בעד

- שְׁבִירוּת

- החל מ-

- נוסף

- גרמניה

- גלוֹבָּלִי

- פיננסי גלובלי

- משבר כלכלי עולמי

- יותר

- יש

- הוחזק

- גבוה יותר

- להבליט

- הדגשה

- הסטורי

- אולם

- HTTPS

- השפעה

- השבחה

- שיפור

- in

- להגדיל

- מדד

- הודו

- מצביע על

- המציין

- מְעִיד עַל

- אינדיקטור

- תעשייה

- שֶׁלָה

- ג'יימי

- יָנוּאָר

- יפן

- jpg

- יוני

- מפתח

- עבודה

- נחיתה

- גָדוֹל

- הגדול ביותר

- קטן יותר

- רמה

- רמות

- תנופה

- לאבד

- להוריד

- הנמוך ביותר

- התעשיינים

- ייצור

- תעשיית ייצור

- שוקי

- חומרים

- מומנטום

- חוֹדֶשׁ

- אחת לחודש

- הרבה

- לא

- צפון

- צפון אמריקה

- יַקִיר

- בייחוד

- אוֹקְטוֹבֶּר

- of

- שמן

- on

- רק

- להזמין

- ספרי הזמנות

- שלנו

- שלום

- במיוחד

- לבצע

- אפלטון

- מודיעין אפלטון

- אפלטון נתונים

- נקודה

- שָׁקוּל

- שמירה

- נשיא

- מחירים

- לייצר

- מספק

- רכישה

- חי

- לאחרונה

- שֵׁפֶל

- באזור

- קרוב משפחה

- להשאר

- שְׂרִידִים

- לדווח

- דוחות לדוגמא

- כושר התאוששות

- לעלות

- עולה

- רוז

- הפעלה

- ריצה

- s

- נראה

- לראות

- סֶפּטֶמבֶּר

- מחסור

- הופעות

- באופן משמעותי

- שלטים

- דומה

- since

- רָפוּי

- רך

- מסחרי

- מוּחלָט

- יציב

- עוד

- החזק ביותר

- בְּתוֹקֶף

- ניכר

- כזה

- להציע

- להתחנן

- ספקים

- לספק

- שרשרת אספקה

- שרשראות אספקה

- סֶקֶר

- מתמשכת

- מֵאֲשֶׁר

- זֶה

- השמיים

- העולם

- שֶׁלָהֶם

- שם.

- הֵם

- זֶה

- ל

- מעקב

- הובלה

- טיפוסי

- Uk

- us

- כלכלה אמריקאית

- Ve

- סְגָן

- סגן הנשיא

- נדיפות

- היה

- we

- חולשה

- שבועות

- הלכתי

- מערבי

- מערב אירופה

- מה

- אשר

- בזמן

- עם

- עובדים

- עוֹלָם

- עולמי

- זפירנט