- China and Hong Kong benchmark stock indices have almost erased last week’s gains.

- NBS Non-Manufacturing PMI sub-components for January are indicating feeble service activities in China.

- A weaker US dollar via a dovish forward monetary policy guidance from the Fed is not enough to act as a bullish catalyst for China and Hong stock markets.

- Technical analysis advocates further potential weakness in the Hang Seng Index in the short to medium term.

این یک تحلیل پیگیری از گزارش قبلی ما است، “Hang Seng Index Technical: Countertrend rebound in play but not major bottoming” به تاریخ 25 ژانویه 2024. کلیک کنید اینجا کلیک نمایید برای یک خلاصه

Last week’s countertrend rallies triggered by the liquidity infusion from China’s central bank, PBoC’s 50 basis points (bps) cut announcement on the RRR (reserve requirement ratio) for major commercial banks have almost been wiped out at this time of the writing.

Week-to-date as of 31 January, China CSI 300 has declined by -2.8 % with similar losses in Hong Kong’s Hang Seng Indices; Hang Seng Index (-2.6%), Hang Seng TECH Index (-4.7%), and Hang Seng China Enterprises Index (-2.6%).

The resurgence of the bearish tone has been the continuation of lacklustre data from China’s key leading economic indicators. Manufacturing activities have continued to hover in a contractionary mode where the NBS Manufacturing PMI remained below the 50 level for four consecutive months with the latest January’s print just inched up slightly to 49.2 from the December 2023 six-month low of 49.0.

Lack of clear upside momentum in China’s services sector

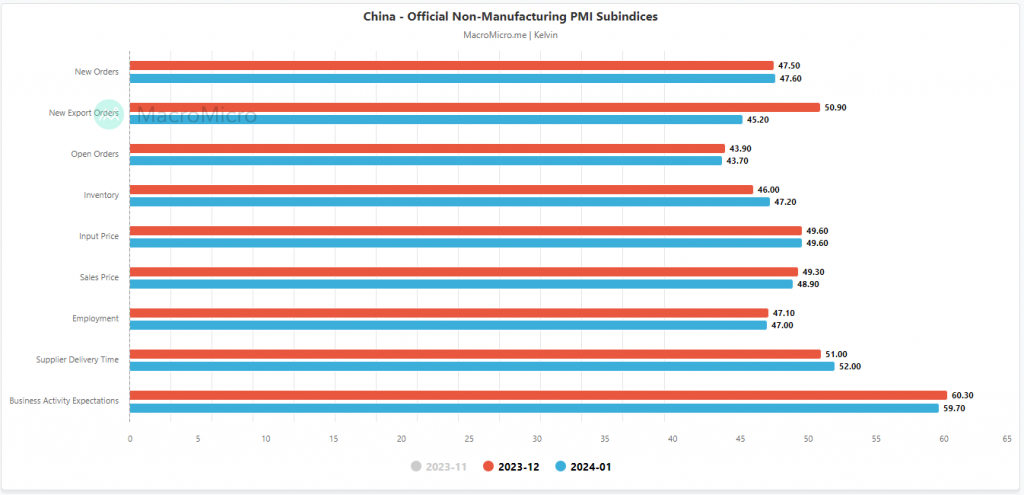

Fig 1: China NBS Non-Manufacturing PMI sub-components as of Jan 2024 (Source: MacroMicro, click to enlarge chart)

Even though the service sector has continued to expand modestly; the NBS Non-Manufacturing PMI for January came in at 50.7 from 50.4 recorded in December 2023 as well as slightly above the consensus of 50.6 but several sub-components have started to contract (see Fig 1).

New export orders have declined in January (45.20 vs 50.90 December), sales prices decreased further (48.9 vs 49.3 December), and business activity expectations (sentiment) eased to a three-month low (59.7 vs 60.3 December).

Overall, it’s a feeble services sector in China where the heightened risk of a deflationary spiral seems to be hard to reverse at least in the mindsets of stock market participants.

A weaker US dollar is likely not enough to act as a bullish catalyst

Fig 2: USD/CNH medium-term trend with CSI 300, HSI, HSCEI & EMXC as of 31 Jan 2024 (Source: TradingView, click to enlarge chart)

Given that the deflationary risk spiral is a structural economic weakness phenomenal, any potential upside cyclical factors such as lower interest rates, and a weaker US dollar may not be enough to trigger a medium-term bullish catalyst for China and the Hong Kong stock market.

Based on the recent broad-based US dollar weakness seen since late October 2023 where the US Fed’s dovish pivot intensified, the offshore yuan (CNH) has reversed from its prior nine-months of bearish trend against the US dollar and rallied by +3.1% but it has not translated to a positive reflexive feedback loop into the CSI 300, Hang Seng Index, and Hang Seng China Enterprises Index in contrast to its previous positive price actions seen during October 2022 to January 2023.

A further conclusion can be observed that other emerging markets stock markets have benefited from a weaker US dollar environment so far as the MSCI Emerging Markets excluding China exchange-traded fund (EMXC) has gained by close to 13% since the end of October 2023.

Therefore, if US Fed Chair Powell issues a dovish forward monetary policy guidance in today’s FOMC, it is likely that the US dollar may kickstart another impulsive down move sequence as US Treasury yields are likely to come under downside pressure.

However, China and Hong Kong stock markets may not be able to reap the fruits of such potential renewed US dollar weakness until the deflationary risk spiral is eradicated.

Watch the 15,900 key short-term resistance on the Hang Seng Index

Fig 3: Hong Kong 33 short-term trend as of 31 Jan 2024 (Source: TradingView, click to enlarge chart)

In the lens of technical analysis, the short and medium-term downtrend phases of the شاخص 33 هنگ کنگ (a proxy of the Hang Seng Index futures) are still intact despite last week’s rebound as price actions have continued to oscillate below its 20-day and 50-day moving averages.

Recent price actions have failed to make any clear breakout above its 20-day moving average after a test on it in the past week coupled with no bullish divergence condition being flashed out in the hourly RSI momentum indicator when it hit its oversold zone yesterday, 30 January.

These observations have suggested that short-term downside momentum has resurfaced which may lead to lower price actions of the Index that exposes the next immediate supports at 15,000 and 14,600 (also the key 31 October 2022 swing low area).

On the other hand, a clearance above 15,900 key short-term pivotal resistance negates the bearish tone for another round of countertrend rebound sequence with the next intermediate resistances coming in at 16,220 and 16,525.

محتوا فقط برای اهداف اطلاعات عمومی است. این توصیه سرمایه گذاری یا راه حلی برای خرید یا فروش اوراق بهادار نیست. نظرات نویسندگان هستند. نه لزوما OANDA Business Information & Services, Inc. یا هر یک از شرکت های وابسته، شرکت های تابعه، افسران یا مدیران آن. اگر مایل به بازتولید یا توزیع مجدد هر یک از محتوای موجود در MarketPulse هستید، یک فارکس برنده جایزه، تحلیل کالاها و شاخص های جهانی و سرویس سایت خبری تولید شده توسط OANDA Business Information & Services, Inc.، لطفاً به فید RSS دسترسی داشته باشید یا با ما تماس بگیرید info@marketpulse.com. بازدید https://www.marketpulse.com/ برای کسب اطلاعات بیشتر در مورد ضربان بازارهای جهانی. © 2023 OANDA Business Information & Services Inc.

کلوین وانگ که علاقه مند به اتصال نقاط در بازارهای مالی و به اشتراک گذاشتن دیدگاه ها در مورد معاملات و سرمایه گذاری است، متخصص در استفاده از ترکیبی منحصر به فرد از تحلیل های بنیادی و فنی است که متخصص در موقعیت یابی موج الیوت و جریان وجوه برای تعیین سطوح معکوس کلیدی در مالی است. بازارها

علاوه بر این، طی ده سال گذشته، کلوین سمینارهای متعددی درباره چشم انداز بازار و تجارت و همچنین دوره های آموزشی تحلیل تکنیکال برای هزاران تاجر خرده فروشی برگزار کرده است.

آخرین پست های کلوین ونگ (دیدن همه)

- محتوای مبتنی بر SEO و توزیع روابط عمومی. امروز تقویت شوید.

- PlatoData.Network Vertical Generative Ai. به خودت قدرت بده دسترسی به اینجا.

- PlatoAiStream. هوش وب 3 دانش تقویت شده دسترسی به اینجا.

- PlatoESG. کربن ، CleanTech، انرژی، محیط، خورشیدی، مدیریت پسماند دسترسی به اینجا.

- PlatoHealth. هوش بیوتکنولوژی و آزمایشات بالینی. دسترسی به اینجا.

- منبع: https://www.marketpulse.com/indices/a-dovish-fed-guidance-may-not-reverse-the-rout-in-china-and-hong-kong-stock-markets/kwong

- : دارد

- :است

- :نه

- :جایی که

- $UP

- 000

- 1

- 14

- سال 15

- ٪۱۰۰

- 16

- 20

- 2022

- 2023

- 2024

- 220

- 25

- 30

- 300

- 31

- 33

- 420

- 45

- 49

- 50

- 60

- 600

- 7

- 700

- 8

- 9

- 90

- a

- قادر

- درباره ما

- بالاتر

- دسترسی

- عمل

- اقدامات

- فعالیت ها

- فعالیت

- اضافه

- نصیحت

- طرفداران

- وابستگان

- پس از

- در برابر

- تقریبا

- همچنین

- an

- تجزیه و تحلیل

- تحلیل

- و

- خبر

- دیگر

- هر

- هستند

- محدوده

- دور و بر

- AS

- At

- نویسنده

- نویسندگان

- نماد

- میانگین

- جایزه

- بانک

- بانک

- اساس

- BE

- بی تربیت

- ضرب

- بوده

- بودن

- در زیر

- محک

- جعبه

- برک آوت

- گسترده

- سرسخت کله شق

- واگرایی صعودی

- کسب و کار

- اما

- دکمه ها

- خرید

- by

- آمد

- CAN

- کاتالیست

- مرکزی

- بانک مرکزی

- صندلی

- چارت سازمانی

- چین

- چیناس

- واضح

- ترخیص کالا از گمرک

- کلیک

- نزدیک

- COM

- ترکیب

- بیا

- آینده

- تجاری

- Commodities

- نتیجه

- شرط

- انجام

- اتصال

- متوالی

- اجماع

- تماس

- محتوا

- ادامه

- ادامه داد:

- قرارداد

- کنتراست

- همراه

- دوره

- CSI

- CSI 300

- برش

- چرخه ای

- داده ها

- دسامبر

- کاهش یافته

- deflationary

- با وجود

- مدیران

- واگرایی

- دلار

- دلپذیر

- پایین

- نزولی

- در طی

- اقتصادی

- نشانگرهای اقتصادی

- الیوت

- سنگ سنباده

- بازارهای در حال ظهور

- پایان

- بزرگنمایی کنید

- کافی

- شرکت

- محیط

- اتر (ETH)

- تبادل

- مبادله شده

- به استثنای

- گسترش

- انتظارات

- تجربه

- کارشناس

- صادرات

- عوامل

- ناموفق

- بسیار

- تغذیه

- صندلی صندوق عقب

- صندلی فدرال رزرو پاول

- باز خورد

- انجیر

- مالی

- پیدا کردن

- جریان

- FOMC

- برای

- خارجی

- ارز خارجی

- فارکس

- به جلو

- یافت

- چهار

- از جانب

- میوه ها

- صندوق

- اساسی

- بیشتر

- آینده

- به دست آورد

- عایدات

- سوالات عمومی

- جهانی

- بازارهای جهانی

- راهنمایی

- دست

- آویزان کردن

- آویزان سنگ

- سخت

- آیا

- بالا بردن

- اصابت

- هنگ

- هنگ کنگ

- در تردید بودن

- HTTPS

- if

- فوری

- تکان دهنده

- in

- شرکت

- شاخص

- نشان دادن

- شاخص

- شاخص ها

- Indices

- اطلاعات

- تزریق

- تشدید شد

- علاقه

- نرخ بهره

- حد واسط

- به

- سرمایه گذاری

- مسائل

- IT

- ITS

- ژان

- ژانویه

- تنها

- کلوین

- کلید

- کنگ

- نام

- دیر

- آخرین

- رهبری

- برجسته

- کمترین

- عدسی

- سطح

- سطح

- پسندیدن

- احتمالا

- نقدینگی

- تلفات

- کم

- کاهش

- درشت دستور

- عمده

- ساخت

- تولید

- بازار

- چشم انداز بازار

- تحقیقات بازار

- MarketPulse

- بازارها

- حداکثر عرض

- ممکن است..

- متوسط

- حالت

- حرکت

- پولی

- سیاست های پولی

- ماه

- بیش

- حرکت

- متحرک

- میانگین متحرک

- میانگین متحرک

- MSCI

- لزوما

- اخبار

- بعد

- نه

- متعدد

- مشاهدات

- مشاهده

- اکتبر

- of

- مامورین

- on

- فقط

- دیدگاه ها

- or

- سفارشات

- دیگر

- ما

- خارج

- چشم انداز

- روی

- شرکت کنندگان

- احساساتی

- گذشته

- دیدگاه

- فاز

- فوق العاده

- عکس

- محور

- محوری

- افلاطون

- هوش داده افلاطون

- PlatoData

- بازی

- لطفا

- بعد از ظهر

- نقطه

- سیاست

- تثبیت موقعیت

- مثبت

- پست ها

- پتانسیل

- پاول

- فشار

- قبلی

- قیمت

- قیمت

- چاپ

- قبلا

- ساخته

- ارائه

- پروکسی

- اهداف

- تظاهرات

- نرخ

- نسبت

- درو کنید

- عقب نشینی

- خلاصه

- اخیر

- ثبت

- باقی مانده است

- تجدید

- گزارش

- نیاز

- تحقیق

- ذخیره

- مقاومت

- خرده فروشی

- برگشت

- معکوس

- خطر

- دور

- مسیر

- RSI

- RSS

- حراجی

- بخش

- اوراق بهادار

- دیدن

- به نظر می رسد

- مشاهده گردید

- فروش

- ارشد

- احساس

- دنباله

- سرویس

- خدمات

- چند

- اشتراک

- کوتاه

- کوتاه مدت

- مشابه

- پس از

- سنگاپور

- سایت

- So

- تا حالا

- راه حل

- منبع

- متخصص

- آغاز شده

- هنوز

- موجودی

- بازار سهام

- بازار سهام

- رزمارا

- ساختاری

- شرکتهای تابعه

- چنین

- پشتیبانی از

- تاب خوردن

- فن آوری

- فنی

- تجزیه و تحلیل فنی

- ده

- مدت

- آزمون

- که

- La

- فدرال رزرو

- این

- اگر چه؟

- هزاران نفر

- زمان

- به

- امروز

- TONE

- معامله گران

- تجارت

- TradingView

- آموزش

- خزانه داری

- بازده خزانه داری

- روند

- ماشه

- باعث شد

- زیر

- منحصر به فرد

- تا

- بالا

- us

- دلار آمریکا

- ما تغذیه کردیم

- وزارت خزانه داری ایالات متحده

- بازدهی خزانه داری آمریکا

- با استفاده از

- v1

- از طريق

- بازدید

- vs

- موج

- ضعیف تر

- ضعف

- هفته

- خوب

- چه زمانی

- که

- برنده

- با

- وانگ

- خواهد بود

- نوشته

- سال

- دیروز

- بازده

- شما

- یوان

- زفیرنت

- منطقه