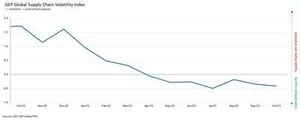

The GEP Global Supply Chain Volatility Index — the indicator tracking demand conditions, shortages, transportation costs, inventories and backlogs based on a monthly survey of 27,000 businesses — decreased again in October to -0.41, from -0.35 in September, indicating a 7th successive month of rising spare capacity across the world’s supply chains.

Additionally, the extent to which supplier capacity went underutilised was even greater than in September and August. Coupled with October’s downturn in demand for raw materials, components and commodities, this shows rising slack in global supply chains.

“While the shrinking of global suppliers’ order books is not worsening, there are no signs of improvement,” explained Jamie Ogilvie-Smals, vice president, consulting, GEP. “The notable increase in supplier capacity in Asia, which was driven by China, provides global manufacturers with greater leverage to drive down prices and inventories in 2024.”

A key finding from October’s report was the strongest rise in excess capacity across Asian supply chains since June 2020. Sustained weakness in demand, coupled with falling pressures on factories in Asia, indicates that the global manufacturing recession has further to run. With the exception of India, which continues to perform strongly, large economies in the region, such as Japan and China, are losing momentum.

Suppliers in Europe continue to report the largest level of spare capacity. In fact, the lower levels in GEP’s supply chain index for the continent have only been seen during the global financial crisis between 2008 and 2009. They highlight sustained weakness in economic conditions across the continent. Western Europe, particularly Germany’s manufacturing industry, is a key driver behind the region’s deterioration.

وتتمثل النقطة المضيئة نسبيا في أمريكا الشمالية، حيث تتمتع سلاسل التوريد بقدرة فائضة، ولكن بدرجة أقل كثيرا من أي مكان آخر، حيث يواصل الاقتصاد الأمريكي إظهار مرونته، في تناقض صارخ مع أوروبا.

أكتوبر 2023 النتائج الرئيسية

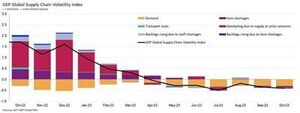

Demand: Demand for raw materials, components and commodities remains depressed, although the downturn seems to have stabilised. There are still no signs of conditions improving, however, as global purchasing activity fell again in October at a pace similar to what we’ve seen since around mid-year.

Demand: Demand for raw materials, components and commodities remains depressed, although the downturn seems to have stabilised. There are still no signs of conditions improving, however, as global purchasing activity fell again in October at a pace similar to what we’ve seen since around mid-year.- المخزونات: مع انخفاض الطلب، تظهر بياناتنا شهرًا آخر من استنزاف الشركات العالمية للمخزونات، مما يشير إلى جهود الحفاظ على التدفق النقدي.

- نقص المواد: لا تزال التقارير عن نقص المواد عند أدنى مستوياتها منذ يناير 2020.

- Labour shortages: Shortages of workers are not impacting global manufacturers’ capacity to produce, with reports of backlogs due to inadequate labour supply running at historically typical levels.

- Transportation: Global transportation costs held steady with September’s level, although oil prices have declined in recent weeks.

تقلبات سلسلة التوريد الإقليمية

-

أمريكا الشمالية: انخفض المؤشر إلى -0.34 من -0.30. ويظل هذا أقل بكثير من المتوسط العالمي ويستمر في الإشارة إلى الولايات المتحدة. الاقتصاد يستعد لهبوط ناعم

- أوروبا: ارتفع المؤشر إلى -0.90، من -1.01، لكنه لا يزال عند مستوى يدل على هشاشة اقتصادية كبيرة.

- المملكة المتحدة: ارتفع المؤشر قليلاً إلى -0.93، من -0.98. ومع ذلك، تشير البيانات إلى ارتفاع كبير في الطاقة الفائضة لدى الموردين لأسواق المملكة المتحدة.

- Asia: Notably, the index dropped to -0.38, from -0.20, highlighting the biggest rise in spare supplier capacity in Asia since June 2020 as the region’s resilience fades.

- محتوى مدعوم من تحسين محركات البحث وتوزيع العلاقات العامة. تضخيم اليوم.

- PlatoData.Network Vertical Generative Ai. تمكين نفسك. الوصول هنا.

- أفلاطونايستريم. ذكاء Web3. تضخيم المعرفة. الوصول هنا.

- أفلاطون كربون، كلينتك ، الطاقة، بيئة، شمسي، إدارة المخلفات. الوصول هنا.

- أفلاطون هيلث. التكنولوجيا الحيوية وذكاء التجارب السريرية. الوصول هنا.

- المصدر https://www.logisticsit.com/articles/2023/11/21/supply-chains-worldwide-remain-significantly-underutilised-gep-global-supply-chain-volatility-index

- :لديها

- :يكون

- :ليس

- :أين

- 000

- 01

- 121

- 20

- 2008

- 2020

- 2023

- 2024

- 27

- 30

- 300

- 35%

- 41

- المرتبة الرابعة

- 90

- 98

- a

- في

- نشاط

- مرة أخرى

- بالرغم ان

- أمريكا

- و

- آخر

- هي

- حول

- AS

- آسيا

- الآسيوية

- At

- أغسطس

- المتوسط

- على أساس

- كان

- وراء

- ما بين

- أكبر

- كُتُب

- مشرق

- الأعمال

- لكن

- by

- الطاقة الإنتاجية

- سلسلة

- السلاسل

- الصين

- السلع

- مكونات

- الشروط

- كبير

- الاستشارات

- قارة

- استمر

- تواصل

- تباين

- التكاليف

- إلى جانب

- أزمة

- البيانات

- انخفض

- الطلب

- العرض

- إلى أسفل

- هبوط

- قيادة

- مدفوع

- سائق

- إسقاط

- اثنان

- أثناء

- اقتصادي

- ظروف اقتصادية

- الاقتصادات

- اقتصاد

- جهود

- في مكان آخر

- الأثير (ETH)

- أوروبا

- حتى

- استثناء

- فائض

- شرح

- مدى

- حقيقة

- المصانع

- يتلاشى

- هبوط

- مالي

- أزمة مالية

- العثور على

- في حالة

- ضعف

- تبدأ من

- إضافي

- ألمانيا

- العالمية

- المالية العالمية

- الأزمة المالية العالمية

- أكبر

- يملك

- عقد

- أعلى

- تسليط الضوء

- تسليط الضوء

- تاريخيا

- لكن

- HTTPS

- تؤثر

- تحسين

- تحسين

- in

- القيمة الاسمية

- مؤشر

- الهند

- يشير

- مبينا

- دلالي

- مؤشر

- العالمية

- انها

- جيمي

- يناير

- اليابان

- JPG

- يونيو

- القفل

- العمل

- هبوط

- كبير

- أكبر

- أقل

- مستوى

- ومستوياتها

- الرافعة المالية

- فقدان

- خفض

- أدنى

- الشركات المصنعة

- تصنيع

- الصناعة التحويلية

- الأسواق

- المواد

- زخم

- شهر

- شهريا

- كثيرا

- لا

- شمال

- امريكا الشمالية

- جدير بالذكر

- لا سيما

- شهر اكتوبر

- of

- زيت

- on

- فقط

- طلب

- ترتيب الكتب

- لنا

- سلام

- خاصة

- نفذ

- أفلاطون

- الذكاء افلاطون البيانات

- أفلاطون داتا

- البوينت

- تستعد

- حفظ

- رئيس

- الأسعار

- إنتاج

- ويوفر

- المشتريات

- الخام

- الأخيرة

- ركود

- منطقة

- نسبي

- لا تزال

- بقايا

- تقرير

- التقارير

- مرونة

- ارتفاع

- ارتفاع

- ROSE

- يجري

- تشغيل

- s

- يبدو

- رأيت

- سبتمبر

- نقص

- يظهر

- بشكل ملحوظ

- لوحات

- مماثل

- منذ

- تثاقل

- ناعم

- بقعة

- قاس

- ثابت

- لا يزال

- أقوى

- بقوة

- جوهري

- هذه

- اقترح

- مزود

- الموردين

- تزويد

- سلسلة التوريد

- سلاسل التوريد

- الدراسة الاستقصائية

- مستمر

- من

- أن

- •

- العالم

- من مشاركة

- هناك.

- هم

- إلى

- تتبع الشحنة

- وسائل النقل

- نموذجي

- Uk

- us

- الاقتصاد الأمريكي

- Ve

- رذيلة

- Vice President

- تطاير

- وكان

- we

- ضعف

- أسابيع

- ذهب

- الغربي

- أوروبا الغربية

- ابحث عن

- التي

- في حين

- مع

- العمال

- العالم

- في جميع أنحاء العالم

- زفيرنت