BoJ Noguchi reiterated the central bank’s focus on

wage growth to reach their 2% target sustainably with no policy change in

نظر:

- It’s true the impact

of elevated global inflation is reaching Japan’s economy with consumer

inflation exceeding the BoJ’s 2% target since the spring of 2022. - But the rise (in

inflation) is mostly due to cost-push factors amid higher import prices. - To achieve our 2% inflation

target, we must see price rises backed by sustained wage increases. - While annual spring

wage negotiations this year achieved wage hikes unseen in 30 years, we’ve

only just reached a stage where the possibility of achieving our target

has come into sight.

BoJ Noguchi

The Switzerland November CPI missed expectations with

both the measures comfortably in the SNB’s 0-2% target range:

- CPI Y/Y 1.4% بمقابلہ

1.7% متوقع اور 1.7% پہلے۔ - CPI M/M -0.2% vs.

-0.1% expected and 0.1% prior. - Core CPI Y/Y 1.4% vs.

1.5% پہلے۔

Switzerland CPI YoY

ECB’s de Guindos (neutral – voter) maintained his

neutral stance as the central bank keeps a “wait and see” approach:

- Recent inflation

data is good news. - یہ ایک رہا ہے

‘positive surprise’. - But it is too early

to declare victory. - اجرت میں اضافہ۔

can still have an impact on inflation. - مانیٹری پالیسی

stance will be data dependent.

ای سی بی کے ڈی گینڈوس

The Tokyo CPI for

November fell further:

- سی پی آئی

Y/Y 2.6% vs. 3.3% prior. - کور

CPI Y/Y 2.3% vs. 2.4% expected and 2.7% prior. - Core-Core

CPI Y/Y 2.7% vs. 2.7% prior.

ٹوکیو کور-کور CPI YoY

The Chinese Caixin Services

PMI for November beat expectations:

- Caixin سروسز PMI

51.5 بمقابلہ 50.8 متوقع اور 50.4 پہلے۔

کلیدی

points from the report:

- کاروباری سرگرمی

and new orders increase at quickest rates in three months. - Confidence around

the year-ahead improves. - افراط زر کا دباؤ کمزور ہوتا ہے۔

چائنا کیکسن سروسز پی ایم آئی

The RBA left the cash

rate unchanged at 4.35% as expected with a slightly dovish tone:

- Whether further

tightening of monetary policy is required to ensure that inflation returns

to target in a reasonable timeframe will depend upon the data and the

evolving assessment of risks. - Board remains

resolute in its determination to return inflation to target. - محدود

information received on the domestic economy since the November meeting

has been broadly in line with expectations. - کے لیے آؤٹ لک۔

household consumption also remains uncertain. - The monthly CPI

indicator for October suggested that inflation is continuing to moderate,

driven by the goods sector; the inflation update did not, however, provide

much more information on services inflation. - کے اقدامات

inflation expectations remain consistent with the inflation target. - میں حالات

labour market also continued to ease gradually, although they remain tight. - Domestically, there

are uncertainties regarding the lags in the effect of monetary policy. - زیادہ دلچسپی

rates are working to establish a more sustainable balance between

aggregate supply and demand in the economy. - Holding the cash

rate steady at this meeting will allow time to assess the impact of the

increases in interest rates on demand, inflation and the labour market.

آرجیبی

The Eurozone PPI

for October came in line with expectations:

- PPI Y/Y -9.4% vs.

-9.5% expected and -12.4% prior. - PPI M/M 0.2% vs.

0.2% متوقع اور 0.5% پہلے۔

Eurozone PPI YoY

ای سی بی کے شنابیل

(hawk – voter) changed her tone to a more neutral stance after the latest

inflation report:

- مزید شرح میں اضافہ

“rather unlikely” after latest inflation data. - Inflation developments

are encouraging, fall in core prices remarkable. - Must be careful

about guiding policy for many months out. - Current level of

restriction is sufficient, has increased confidence 2% target will be met

2025. - But must not declare

victory prematurely. - Inflation is on the

right track, but more progress is needed. - No prolonged

recession is seen. - ڈیٹا سے پتہ چلتا ہے

economy may be bottoming out.

ای سی بی کے شنابیل

The US ISM

Services PMI for November beat expectations:

- آئی ایس ایم سروسز پی ایم آئی

52.7 بمقابلہ 52.0 متوقع اور 51.8 پہلے۔ - Employment index 50.7 vs. 50.2 prior.

- New orders index

55.5 بمقابلہ 55.5 پہلے۔ - Prices paid index

58.3 بمقابلہ 58.6 پہلے۔ - New export orders

53.6 بمقابلہ 48.8 پہلے۔ - Imports 53.7 vs. 60.0 prior.

US ISM سروسز PMI

The US Job Openings for

October missed expectations by a big margin with a negative revision to the

prior reading:

- Job Openings 8.733M

vs. 9.300M expected and 9.350M prior (revised from 9.553M). - Hires 3.7% vs. 3.7% prior.

- Separations rate 3.6% vs. 3.6% prior.

- Quits 2.3% vs. 2.3%

پہلے.

امریکی ملازمت کے مواقع

The Australian Q3 GDP

missed expectations:

- GDP Q/Q 0.2% vs.

0.4% متوقع اور 0.4% پہلے۔ - GDP Y/Y 2.1% vs.

1.8% متوقع اور 2.1% پہلے۔

Australia Q3 GDP

BoJ’s Himino just echoed

the other members’ comments with the usual focus on wage growth:

- BoJ will patiently

maintain easy policy until sustained, stable achievement of price target

نظر میں ہے. - Japan’s financial

system is likely resilient enough to weather stress from transition to

higher interest rates.

- If we do not get the

timing exit procedures wrong, the impact of a positive wage-inflation

cycle will likely benefit wide range of households, companies.

- Must make

appropriate decision on exit timing, procedure by scrutinising wage,

inflation developments. - BoJ must achieve

situation where inflation slows ahead, but not too much.

- Japan is seeing

steadily changes in price, wage behaviour.

- Solid progress is

observed in the transformation of firms’ wage- and price-setting

رویے - قیمت بڑھ جاتی ہے۔

beginning to affect wages. - Pass-through from

wages to inflation is also returning somewhat. - Without virtuous

cycle between wages and prices, Japan will most likely revert to the

deflationary state in the past.

- When Japan returns

to an economy with positive interest rate, that could improve households’

balance as a whole. - اگر مہنگائی

expectations have heightened, that would mean impact of rise in real

interest rate could be smaller than that of nominal rate.

BoJ Himino

یوروزون

Retail Sales for October missed expectations:

- پرچون

Sales M/M 0.1% vs. 0.2% expected and -0.1% prior (revised from -0.3%). - پرچون

Sales Y/Y -1.2% vs. -1.1% expected and -2.9% prior.

Eurozone Retail Sales YoY

BoE’s Bailey

(neutral – voter) reaffirmed the central bank’s “wait and see” approach:

- کے لیے آؤٹ لک۔

inflation is uncertain. - Rates likely to need

to remain around current levels. - We remain vigilant

to financial stability risks that might arise.

BoE کے گورنر بیلی

ECB’s Kazimir

(hawk – voter) pushed back against markets’ rate cuts expectations:

- مزید

rate hike is unlikely to be needed but market bets for Q1 rate cut are science

افسانہ

ECB’s Kazimir

The US ADP missed

توقعات:

- ADP 103K vs. 130K

expected and 106K prior (revised from 113K).

تفصیلات:

- Small (less than 50

employees) 6K vs. 19K prior. - Medium firms (500 –

499) 68K vs. 78K prior. - Large (greater than

499 employees) 33K vs. 18K prior.

Changes in pay:

- Job stayers 5.6% vs.

5.7% prior – slowest since September 2021. - Job changers 8.3% vs. 8.4% prior.

US ADP

The BoC left

interest rates unchanged at 5.00% as expected:

- Statement repeats

that BoC “is prepared to raise the policy rate further if

needed”. - Data “suggest

the economy is no longer in excess demand”. - BoC saw

“further signs that monetary policy is moderating spending and relieving

price pressures”. - The slowdown in the

economy is reducing inflationary pressures in a broadening range of goods

and services prices. - گورننگ کونسل

wants to see further and sustained easing in core inflation. - The global economy continues

to slow, and inflation has eased further. - US growth has been

stronger than expected but is likely to weaken in the months ahead. - Growth in the euro

area has weakened. - Oil prices are about

$10-per-barrel lower than was assumed in the October MPR. - The US dollar has

weakened against most currencies, including Canada’s. - زیادہ دلچسپی

rates are clearly restraining spending: consumption growth in the last two

quarters was close to zero. - لیبر مارکیٹ۔

continues to ease: job creation has been slower than labour force growth.

BoC

ای سی بی کے ویلرائے

(neutral – voter) reaffirmed that the central bank is done with rate hikes and

the next step is rate cuts in 2024:

- Disinflation is

happening more quickly than we thought. - This is why, barring

any shocks, there will not be any new rise in rates. The question of a

rate cut could arise in 2024, but not right now.

ای سی بی کے ویلرائے

BoJ Governor Ueda didn’t

say anything explicitly about an exit from the current easy policy BUT you can

clearly read between the lines that they are considering rate hikes:

- Japan’s economy to

continue recovering moderately, supported mainly by accommodative

financial conditions and effects of economic stimulus measures. - Uncertainty over

Japan’s economy extremely high. - Closely watching the

impact of financial, forex markets on the Japanese economy, prices.

- Will patiently

continue monetary easing under YCC to support economic activity, cycle of

اجرت میں اضافہ

- We have not yet

reached a situation in which we can achieve price target sustainably and

stably and with sufficient certainty.

- Challenging situation remains.

- It’ll become even

more challenging towards the end of this year and into early 2024.

- BoJ has not made

decision on which interest rate to target once we end negative interest

rate policy. - اختیارات میں شامل ہیں

raising rate applied to financial institutions’ reserves at BoJ, or revert

to policy targeting overnight call rate.

- Don’t have any

specific idea in mind on how much we will raise rates once we end negative

rate policy.

- Whether to keep

interest rate at zero or move it up to 0.1%, and at what pace short-term

rates will be hiked after ending negative rate policy, will depend on

economic and financial developments at the time. - Achieving 2% trend

inflation can be defined as a state where economy, void of new shocks, can

see inflation sustained around 2% and wage growth somewhat above that

سطح. - Would be difficult

to choose which monetary policy tools to mobilise when exit from stimulus

قریب آتا ہے - BoJ to work closely

with govt while monitoring currency, financial market moves. - Service spending

increasing moderately as a trend. - کیا اہم ہے

from here is for wages to keep rising and underpin consumption.

BoJ گورنر Ueda

سوئٹزرلینڈ

Unemployment Rate for November ticked higher to 2.1% vs. 2.0% prior, while the

Seasonally adjusted unemployment rate remained unchanged at 2.1% vs. 2.2%

متوقع.

Switzerland Unemployment Rate

The US Challenger

Job Cuts for November increased to 45.51K vs. 36.84K prior. Compared to the

same month last year, job cuts are down by roughly 41% but then again there was

an exceptional number of tech layoffs in November of 2022. The 45.51K layoffs

last month brings the year-to-date total to 686,860 and that’s roughly a 115%

increase to the year-to-date total for last year through to November.

یو ایس چیلنجر نوکریوں میں کمی

The US Jobless

Claims beat expectations across the board:

- ابتدائی دعوے 220K

بمقابلہ 222K متوقع اور 219K پہلے (218K سے نظر ثانی شدہ)۔ - دعوے جاری رکھنا

1861K بمقابلہ 1910K متوقع اور 1925K پہلے (1927K سے نظر ثانی شدہ)۔

امریکی بے روزگاری کے دعوے

BoC’s Gravelle

acknowledged the progress on inflation:

- Gravelle noted that

housing imbalances have serious consequences for shelter price inflation,

contributing 1.8 percentage points to the total October inflation rate of

3.1٪ - Emphasized the need

for Canada to have more homes and a housing supply that is more responsive

to increases in demand. - Pointed out that a

jump in demographic demand, coupled with existing structural supply

issues, could explain why rent inflation continues to climb. - Stressed the

importance of all levels of government working together on housing

policies to boost supply. - Urged the reduction

of barriers to adding capacity and ensuring market flexibility to meet

future changes in housing demand. - Warned that without

more house building, inflationary pressures in the shelter sector could

continue to build. - Highlighted that

rent inflation reached a 40-year high in October, with housing supply not

keeping pace with recent increases in immigration. - Reported that

housing activity grew 8.3% in Q3 but remains far below the level needed to

meet growing housing needs. - Commented that

recent increases in immigration have boosted near-term consumption but

haven’t significantly affected inflation. - Noted that the

economy is now roughly in balance, with a focus on monitoring inflation

expectations, wage growth, and corporate pricing behaviour. - Stressed the

importance of indicators in assessing whether inflation is on a sustained

path to the 2% target. - Said that the market

has been relatively right on their previous two or three decisions, so it

seems like it’s taking in the data in the same way they are.

BoC’s Gravelle

The Japanese Average Cash Earnings increased in

October on a year-over-year basis marking the 22nd لگاتار مہینہ

of rising wages:

- Average Cash

Earnings Y/Y 1.5% vs. 0.6% prior (revised from 1.2%). - Real wages Y/Y -2.3%.

جاپان کی اوسط نقد آمدنی YoY

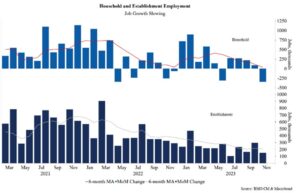

The US NFP report beat expectations across the board

by a big margin:

- NFP 199K vs. 180K

expected and 150K prior. - Two-month net

revision -35K vs -101K prior. - بے روزگاری کی شرح 3.7٪

بمقابلہ 3.9% متوقع اور 3.9% پہلے۔ - Participation rate 62.8% vs. 62.7% prior.

- U6 underemployment

rate 7.0% vs. 7.2% prior. - اوسط فی گھنٹہ

earnings M/M 0.4% vs. 0.3% expected and 0.2% prior. - اوسط فی گھنٹہ

earnings Y/Y 4.0% vs. 4.1% expected and 4.0% prior (revised from 4.1%). - اوسط ہفتہ وار گھنٹے

34.4 بمقابلہ 34.3 متوقع اور 34.3 پہلے۔ - Change in private

payrolls 150K vs. 153K expected. - میں تبدیلی

manufacturing payrolls 28K vs. 30K expected. - Household survey 747K

vs. -348K prior. - Birth-death

adjustment 4K vs. 412K prior.

امریکی بے روزگاری کی شرح

The highlights for next week will be:

- منگل: Japan PPI, UK Labour Market report, NFIB Small

Business Optimism Index, US CPI. - بدھ کے روز: UK GDP, Eurozone Industrial Production, US PPI, FOMC

Policy Decision, New Zealand GDP. - جمعرات: Australia Labour Market report, SNB Policy Decision,

BoE Policy Decision, ECB Policy Decision, US Retail Sales, US Jobless Claims,

New Zealand Manufacturing PMI. - جمعہ: Australia/Japan/Eurozone/UK/US Flash PMIs, China

Industrial Production and Retail Sales, Eurozone Wage data, US Industrial

Production, PBoC MLF.

That’s all folks. Have a nice weekend!

- SEO سے چلنے والا مواد اور PR کی تقسیم۔ آج ہی بڑھا دیں۔

- پلیٹو ڈیٹا ڈاٹ نیٹ ورک ورٹیکل جنریٹو اے آئی۔ اپنے آپ کو بااختیار بنائیں۔ یہاں تک رسائی حاصل کریں۔

- پلیٹوآئ اسٹریم۔ ویب 3 انٹیلی جنس۔ علم میں اضافہ۔ یہاں تک رسائی حاصل کریں۔

- پلیٹو ای ایس جی۔ کاربن، کلین ٹیک، توانائی ، ماحولیات، شمسی، ویسٹ مینجمنٹ یہاں تک رسائی حاصل کریں۔

- پلیٹو ہیلتھ۔ بائیوٹیک اینڈ کلینیکل ٹرائلز انٹیلی جنس۔ یہاں تک رسائی حاصل کریں۔

- ماخذ: https://www.forexlive.com/news/weekly-market-recap-04-08-december-20231208/

- : ہے

- : ہے

- : نہیں

- :کہاں

- $UP

- 1

- 18k

- 2%

- 2% افراط زر

- 2021

- 2022

- 2024

- 2025

- 220K

- 26

- 30

- 35٪

- 36

- 4k

- 50

- 500

- 51

- 52

- 53

- 58

- 60

- 7

- 8

- 9

- a

- ہمارے بارے میں

- اوپر

- حاصل

- حاصل کیا

- کامیابی

- حصول

- کا اعتراف

- کے پار

- سرگرمی

- انہوں نے مزید کہا

- ایڈجسٹ

- ایڈجسٹمنٹ

- اے پی پی

- پر اثر انداز

- متاثر

- کے بعد

- پھر

- کے خلاف

- مجموعی

- آگے

- تمام

- کی اجازت

- بھی

- اگرچہ

- کے ساتھ

- an

- اور

- سالانہ

- کوئی بھی

- کچھ

- اطلاقی

- نقطہ نظر

- مناسب

- کیا

- رقبہ

- اٹھتا

- ارد گرد

- AS

- تشخیص کریں

- اندازہ

- تشخیص

- فرض کیا

- At

- آسٹریلیا

- آسٹریلیا

- اوسط

- واپس

- حمایت کی

- بیلی

- متوازن

- بینک

- راہ میں حائل رکاوٹیں

- بنیاد

- BE

- شکست دے دی

- بن

- رہا

- شروع

- رویے

- نیچے

- فائدہ

- شرط لگاتا ہے۔

- کے درمیان

- بگ

- بورڈ

- BoC

- BoE

- بوج

- بڑھانے کے

- بڑھا

- دونوں

- لاتا ہے

- موٹے طور پر

- تعمیر

- عمارت

- کاروبار

- لیکن

- by

- فون

- آیا

- کر سکتے ہیں

- کینیڈا

- اہلیت

- ہوشیار

- کیش

- مرکزی

- مرکزی بینک

- یقین

- چیلنج

- چیلنج

- تبدیل

- تبدیل کر دیا گیا

- تبدیلیاں

- چین

- چینی

- میں سے انتخاب کریں

- دعوے

- واضح طور پر

- چڑھنے

- کلوز

- قریب سے

- کس طرح

- تبصروں

- کمپنیاں

- مقابلے میں

- حالات

- آپکا اعتماد

- مسلسل

- نتائج

- پر غور

- متواتر

- صارفین

- کھپت

- جاری

- جاری رہی

- جاری ہے

- جاری

- تعاون کرنا

- کور

- کور افراط زر

- کارپوریٹ

- سکتا ہے

- کونسل

- مل کر

- سی پی آئی

- مخلوق

- کرنسیوں کے لئے منڈی کے اوقات کو واضح طور پر دیکھ پائیں گے۔

- کرنسی

- موجودہ

- کٹ

- کمی

- سائیکل

- اعداد و شمار

- دسمبر

- فیصلہ

- فیصلے

- کی وضاحت

- ڈیفلیشنری

- ڈیمانڈ

- آبادیاتی

- انحصار

- انحصار

- عزم

- رفت

- DID

- مشکل

- do

- ڈالر

- ڈومیسٹک

- کیا

- ڈیوش

- نیچے

- مدد دیتی ہے

- کارفرما

- دو

- ابتدائی

- آمدنی

- کو کم

- نرمی

- آسان

- ای سی بی

- ECB پالیسی فیصلہ

- گونگا

- اقتصادی

- معیشت کو

- اثر

- اثرات

- بلند

- ملازمین

- حوصلہ افزا

- آخر

- ختم ہونے

- کافی

- کو یقینی بنانے کے

- کو یقینی بنانے ہے

- قائم کرو

- یورو

- یوروزون

- بھی

- تیار ہوتا ہے

- غیر معمولی

- اضافی

- موجودہ

- باہر نکلیں

- توقعات

- توقع

- وضاحت

- واضح طور پر

- برآمد

- انتہائی

- عوامل

- گر

- دور

- افسانے

- مالی

- مالیاتی ادارے

- مالیاتی منڈی

- مالی استحکام

- فرم

- فلیش

- لچک

- توجہ مرکوز

- FOMC

- کے لئے

- مجبور

- فوریکس

- فاریکس مارکیٹ

- سے

- مزید

- مستقبل

- جی ڈی پی

- حاصل

- گلوبل

- عالمی معیشت

- اچھا

- سامان

- حکومت

- گورنر

- گورنمنٹ

- زیادہ سے زیادہ

- بڑھی

- بڑھتے ہوئے

- ترقی

- ہو رہا ہے۔

- ہے

- جنت

- ہاک

- اونچائی

- اس کی

- یہاں

- ہائی

- اعلی

- پر روشنی ڈالی گئی

- اضافہ

- پریشان

- ان

- ہومز

- HOURS

- ہاؤس

- گھر

- گھریلو

- ہاؤسنگ

- کس طرح

- تاہم

- HTTPS

- خیال

- if

- امیگریشن

- اثر

- درآمد

- اہمیت

- اہم

- کو بہتر بنانے کے

- بہتر ہے

- in

- شامل

- سمیت

- اضافہ

- اضافہ

- اضافہ

- اضافہ

- انڈکس

- اشارے

- انڈیکیٹر

- صنعتی

- صنعتی پیداوار

- افراط زر کی شرح

- افراط زر کی توقعات

- افراط زر کی شرح

- افراط زر

- افراط زر کا دباؤ۔

- معلومات

- اداروں

- دلچسپی

- شرح سود

- سود کی شرح

- میں

- مسائل

- IT

- میں

- جاپان

- جاپان پی پی آئی

- جاپان کا

- جاپانی

- ایوب

- ملازمت میں کمی

- بے روزگار دعوے

- فوٹو

- کودنے

- صرف

- رکھیں

- رکھتے ہوئے

- لیبر

- آخری

- آخری سال

- تازہ ترین

- لے آؤٹ

- چھوڑ دیا

- کم

- سطح

- سطح

- کی طرح

- امکان

- لمیٹڈ

- لائن

- لائنوں

- ll

- اب

- کم

- بنا

- بنیادی طور پر

- برقرار رکھنے کے

- بنا

- مینوفیکچرنگ

- بہت سے

- مارجن

- مارکیٹ

- مارکیٹ کی چالیں

- مارکیٹ کی رپورٹ

- Markets

- مارکنگ

- مئی..

- مطلب

- اقدامات

- سے ملو

- اجلاس

- کے ساتھ

- شاید

- برا

- یاد آیا

- ایم ایل ایف

- اعتدال پسند

- مالیاتی

- مانیٹری پالیسی

- نگرانی

- مہینہ

- ماہانہ

- ماہ

- زیادہ

- سب سے زیادہ

- زیادہ تر

- منتقل

- چالیں

- بہت

- ضروری

- قریب

- ضرورت ہے

- ضرورت

- ضروریات

- منفی

- مذاکرات

- خالص

- غیر جانبدار

- نئی

- نیوزی لینڈ

- نیوزی لینڈ جی ڈی پی

- نیوزی لینڈ مینوفیکچرنگ پی ایم آئی۔

- خبر

- اگلے

- اگلے ہفتے

- این ایف پی

- اچھا

- نہیں

- کا کہنا

- نومبر

- اب

- تعداد

- مشاہدہ

- اکتوبر

- of

- on

- ایک بار

- صرف

- سوراخ

- رجائیت

- or

- احکامات

- دیگر

- ہمارے

- باہر

- پر

- رات بھر

- امن

- ادا

- گزشتہ

- راستہ

- صبر سے

- ادا

- پےرولس

- پی بی او سی

- پی بی او سی ایم ایل ایف

- فیصد

- پلاٹا

- افلاطون ڈیٹا انٹیلی جنس

- پلیٹو ڈیٹا

- pmi

- پوائنٹس

- پالیسیاں

- پالیسی

- مثبت

- امکان

- پیپیآئ

- تیار

- پچھلا

- قیمت

- قیمتیں

- قیمتوں کا تعین

- پہلے

- نجی

- طریقہ کار

- طریقہ کار

- پیداوار

- پیش رفت

- فراہم

- دھکیل دیا

- Q1

- Q3

- سوال

- تیز ترین

- جلدی سے

- بلند

- بلند

- رینج

- شرح

- درجہ بندی کی شرح

- شرح میں اضافہ

- قیمتیں

- بلکہ

- آرجیبی

- تک پہنچنے

- پہنچ گئی

- پہنچنا

- پڑھیں

- پڑھنا

- ایک بار پھر تصدیق

- اصلی

- مناسب

- ریپپ

- موصول

- حال ہی میں

- کساد بازاری

- بحالی

- کو کم کرنے

- کمی

- کے بارے میں

- نسبتا

- رہے

- رہے

- باقی

- قابل ذکر

- کرایہ پر

- رپورٹ

- ضرورت

- ذخائر

- لچکدار

- قبول

- پابندی

- خوردہ

- پرچون سیلز

- واپسی

- واپس لوٹنے

- واپسی

- واپس

- ٹھیک ہے

- اضافہ

- اٹھتا ہے

- بڑھتی ہوئی

- خطرات

- تقریبا

- s

- فروخت

- اسی

- دیکھا

- کا کہنا ہے کہ

- سائنس

- شعبے

- دیکھنا

- دیکھ کر

- لگتا ہے

- دیکھا

- ستمبر

- سنگین

- سروسز

- پناہ

- مختصر مدت کے

- نگاہ

- نمایاں طور پر

- نشانیاں

- بعد

- صورتحال

- سست

- سست روی۔

- سست

- چھوٹے

- چھوٹے

- SNB

- So

- کچھ بھی نہیں

- مخصوص

- خرچ کرنا۔

- موسم بہار

- استحکام

- مستحکم

- اسٹیج

- موقف

- حالت

- مسلسل

- مستحکم

- مرحلہ

- ابھی تک

- محرک

- کشیدگی

- مضبوط

- ساختی

- کافی

- مشورہ

- پتہ چلتا ہے

- فراہمی

- طلب اور رسد

- حمایت

- تائید

- حیرت

- سروے

- پائیدار

- مستقل طور پر

- مسلسل

- سوئٹزرلینڈ

- کے نظام

- T

- لینے

- ہدف

- ھدف بندی

- ٹیک

- سے

- کہ

- ۔

- ان

- تو

- وہاں.

- وہ

- اس

- اس سال

- سوچا

- تین

- کے ذریعے

- سخت

- وقت

- ٹائم فریم

- وقت

- کرنے کے لئے

- مل کر

- ٹوکیو

- ٹوکیو سی پی آئی

- سر

- بھی

- اوزار

- کل

- کی طرف

- ٹریک

- تبدیلی

- منتقلی

- رجحان

- سچ

- دو

- Uk

- یوکے جی ڈی پی

- یوکے لیبر مارکیٹ

- غیر یقینی

- غیر یقینی صورتحال

- کے تحت

- سہارا

- بے روزگاری

- بے روزگاری کی شرح

- امکان نہیں

- جب تک

- اپ ڈیٹ کریں

- صلی اللہ علیہ وسلم

- us

- یو ایس سی پی آئی

- امریکی ڈالر

- امریکی ملازمت کے مواقع

- امریکی بے روزگاری کے دعوے

- ہمیں NFP

- امریکی پی پی آئی۔

- امریکی خوردہ فروخت

- ہمیشہ کی طرح

- Ve

- فتح

- ووٹ

- vs

- اجرت

- اجرت

- چاہتا ہے

- تھا

- دیکھ

- راستہ..

- we

- موسم

- ہفتے

- ہفتہ وار

- کیا

- جب

- چاہے

- جس

- جبکہ

- پوری

- کیوں

- وسیع

- وسیع رینج

- گے

- ساتھ

- بغیر

- کام

- کام کر

- گا

- غلط

- سال

- سال

- ابھی

- آپ

- زی لینڈ

- زیفیرنیٹ

- صفر