BoJ Noguchi reiterated the central bank’s focus on

wage growth to reach their 2% target sustainably with no policy change in

взгляд:

- It’s true the impact

of elevated global inflation is reaching Japan’s economy with consumer

inflation exceeding the BoJ’s 2% target since the spring of 2022. - But the rise (in

inflation) is mostly due to cost-push factors amid higher import prices. - To achieve our 2% inflation

target, we must see price rises backed by sustained wage increases. - While annual spring

wage negotiations this year achieved wage hikes unseen in 30 years, we’ve

only just reached a stage where the possibility of achieving our target

has come into sight.

Банк Японии Ногучи

The Switzerland November CPI missed expectations with

both the measures comfortably in the SNB’s 0-2% target range:

- CPI Y/Y 1.4% vs.

1.7% ожидается и 1.7% ранее. - CPI M/M -0.2% vs.

-0.1% expected and 0.1% prior. - Core CPI Y/Y 1.4% vs.

1.5% до.

ИПЦ в Швейцарии г/г

ECB’s de Guindos (neutral – voter) maintained his

neutral stance as the central bank keeps a “wait and see” approach:

- Recent inflation

data is good news. - Это был

‘positive surprise’. - But it is too early

to declare victory. - Повышение заработной платы

can still have an impact on inflation. - Денежно-кредитная политика

stance will be data dependent.

ECB’s de Guindos

The Tokyo CPI for

November fell further:

- индекс потребительских цен

Y/Y 2.6% vs. 3.3% prior. - Основные

CPI Y/Y 2.3% vs. 2.4% expected and 2.7% prior. - Core-Core

CPI Y/Y 2.7% vs. 2.7% prior.

Базовый индекс потребительских цен в Токио (г/г)

The Chinese Caixin Services

PMI for November beat expectations:

- PMI в сфере услуг Caixin

51.5 vs. 50.8 expected and 50.4 prior.

Основные

points from the report:

- Деловая активность

and new orders increase at quickest rates in three months. - Confidence around

the year-ahead improves. - Инфляционное давление ослабевает.

Китай Caixin Services PMI

The RBA left the cash

rate unchanged at 4.35% as expected with a slightly dovish tone:

- Whether further

tightening of monetary policy is required to ensure that inflation returns

to target in a reasonable timeframe will depend upon the data and the

evolving assessment of risks. - Board remains

resolute in its determination to return inflation to target. - Ограниченный

information received on the domestic economy since the November meeting

has been broadly in line with expectations. - Outlook для

household consumption also remains uncertain. - The monthly CPI

indicator for October suggested that inflation is continuing to moderate,

driven by the goods sector; the inflation update did not, however, provide

much more information on services inflation. - Меры

inflation expectations remain consistent with the inflation target. - Условия в

labour market also continued to ease gradually, хотя они остаются тугими. - Domestically, there

are uncertainties regarding the lags in the effect of monetary policy. - Более высокий процент

rates are working to establish a more sustainable balance between

aggregate supply and demand in the economy. - Holding the cash

rate steady at this meeting will allow time to assess the impact of the

increases in interest rates on demand, inflation and the labour market.

RBA

The Eurozone PPI

for October came in line with expectations:

- PPI Y/Y -9.4% vs.

-9.5% expected and -12.4% prior. - PPI M/M 0.2% vs.

0.2% ожидается и 0.5% ранее.

Индекс цен производителей еврозоны (г/г)

Шнабель из ЕЦБ

(hawk – voter) changed her tone to a more neutral stance after the latest

inflation report:

- Дальнейшее повышение ставок

“rather unlikely” after latest inflation data. - Inflation developments

are encouraging, fall in core prices remarkable. - Must be careful

about guiding policy for many months out. - Current level of

restriction is sufficient, has increased confidence 2% target will be met

в 2025 году. - But must not declare

victory prematurely. - Inflation is on the

right track, but more progress is needed. - No prolonged

recession is seen. - Данные свидетельствуют

economy may be bottoming out.

Шнабель из ЕЦБ

The US ISM

Services PMI for November beat expectations:

- Индекс деловой активности ISM Services

52.7 vs. 52.0 expected and 51.8 prior. - Индекс занятости 50.7 против 50.2 ранее.

- New orders index

55.5 против 55.5 ранее. - Prices paid index

58.3 против 58.6 ранее. - New export orders

53.6 против 48.8 ранее. - Импорт 53.7 против 60.0 предыдущего.

Индекс деловой активности ISM в сфере услуг США

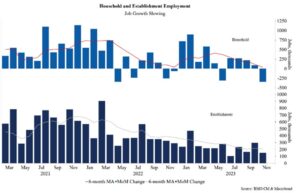

The US Job Openings for

October missed expectations by a big margin with a negative revision to the

prior reading:

- Job Openings 8.733M

vs. 9.300M expected and 9.350M prior (revised from 9.553M). - Нанимает 3.7% против 3.7% ранее.

- Уровень отделений составил 3.6% по сравнению с 3.6% ранее.

- Quits 2.3% vs. 2.3%

до.

Вакансии в США

The Australian Q3 GDP

missed expectations:

- GDP Q/Q 0.2% vs.

0.4% ожидается и 0.4% ранее. - GDP Y/Y 2.1% vs.

1.8% ожидается и 2.1% ранее.

ВВП Австралии в третьем квартале

BoJ’s Himino just echoed

the other members’ comments with the usual focus on wage growth:

- BoJ will patiently

maintain easy policy until sustained, stable achievement of price target

is in sight. - Japan’s financial

system is likely resilient enough to weather stress from transition to

higher interest rates.

- If we do not get the

timing exit procedures wrong, the impact of a positive wage-inflation

cycle will likely benefit wide range of households, companies.

- Must make

appropriate decision on exit timing, procedure by scrutinising wage,

inflation developments. - BoJ must achieve

situation where inflation slows ahead, but not too much.

- Japan is seeing

steadily changes in price, wage behaviour.

- Solid progress is

observed in the transformation of firms’ wage- and price-setting

поведение. - Цена растет

beginning to affect wages. - Pass-through from

wages to inflation is also returning somewhat. - Without virtuous

cycle between wages and prices, Japan will most likely revert to the

deflationary state in the past.

- When Japan returns

to an economy with positive interest rate, that could improve households’

balance as a whole. - If inflation

expectations have heightened, that would mean impact of rise in real

interest rate could be smaller than that of nominal rate.

Банк Японии Химино

Еврозона

Retail Sales for October missed expectations:

- Ритейл

Sales M/M 0.1% vs. 0.2% expected and -0.1% prior (revised from -0.3%). - Ритейл

Sales Y/Y -1.2% vs. -1.1% expected and -2.9% prior.

Розничные продажи в еврозоне (г/г)

Бэйли из Банка Англии

(neutral – voter) reaffirmed the central bank’s “wait and see” approach:

- Outlook для

inflation is uncertain. - Rates likely to need

to remain around current levels. - We remain vigilant

to financial stability risks that might arise.

BoE’s Governor Bailey

ECB’s Kazimir

(hawk – voter) pushed back against markets’ rate cuts expectations:

- В дальнейшем

rate hike is unlikely to be needed but market bets for Q1 rate cut are science

художественная литература.

ECB’s Kazimir

The US ADP missed

ожидания:

- ADP 103K vs. 130K

expected and 106K prior (revised from 113K).

Детали:

- Small (less than 50

employees) 6K vs. 19K prior. - Medium firms (500 –

499) 68K vs. 78K prior. - Large (greater than

499 employees) 33K vs. 18K prior.

Изменения в оплате:

- Job stayers 5.6% vs.

5.7% prior – slowest since September 2021. - Сменившие работу 8.3% против 8.4% ранее.

АДП США

The BoC left

interest rates unchanged at 5.00% as expected:

- Statement repeats

that BoC “is prepared to raise the policy rate further if

needed”. - Data “suggest

the economy is no longer in excess demand”. - BoC saw

“further signs that monetary policy is moderating spending and relieving

price pressures”. - The slowdown in the

economy is reducing inflationary pressures in a broadening range of goods

and services prices. - Управляющий совет

wants to see further and sustained easing in core inflation. - The global economy continues

to slow, and inflation has eased further. - US growth has been

stronger than expected but is likely to weaken in the months ahead. - Growth in the euro

area has weakened. - Oil prices are about

$10-per-barrel lower than was assumed in the October MPR. - The US dollar has

weakened against most currencies, including Canada’s. - Более высокий процент

rates are clearly restraining spending: consumption growth in the last two

quarters was close to zero. - Рынок труда

continues to ease: job creation has been slower than labour force growth.

Банка Канады

ECB’s Villeroy

(neutral – voter) reaffirmed that the central bank is done with rate hikes and

the next step is rate cuts in 2024:

- Disinflation is

happening more quickly than we thought. - This is why, barring

any shocks, there will not be any new rise in rates. The question of a

rate cut could arise in 2024, but not right now.

ECB’s Villeroy

BoJ Governor Ueda didn’t

say anything explicitly about an exit from the current easy policy BUT you can

clearly read between the lines that they are considering rate hikes:

- Japan’s economy to

continue recovering moderately, supported mainly by accommodative

financial conditions and effects of economic stimulus measures. - Uncertainty over

Japan’s economy extremely high. - Closely watching the

impact of financial, forex markets on the Japanese economy, prices.

- Will patiently

continue monetary easing under YCC to support economic activity, cycle of

рост заработной платы.

- We have not yet

reached a situation in which we can achieve price target sustainably and

stably and with sufficient certainty.

- Сложная ситуация остается.

- It’ll become even

more challenging towards the end of this year and into early 2024.

- BoJ has not made

decision on which interest rate to target once we end negative interest

rate policy. - Варианты включают

raising rate applied to financial institutions’ reserves at BoJ, or revert

to policy targeting overnight call rate.

- Don’t have any

specific idea in mind on how much we will raise rates once we end negative

rate policy.

- Whether to keep

interest rate at zero or move it up to 0.1%, and at what pace short-term

rates will be hiked after ending negative rate policy, will depend on

economic and financial developments at the time. - Achieving 2% trend

inflation can be defined as a state where economy, void of new shocks, can

see inflation sustained around 2% and wage growth somewhat above that

уровень. - Would be difficult

to choose which monetary policy tools to mobilise when exit from stimulus

приближается. - BoJ to work closely

with govt while monitoring currency, financial market moves. - Service spending

increasing moderately as a trend. - Что важно

from here is for wages to keep rising and underpin consumption.

Губернатор Банка Японии Уэда

Швейцария

Unemployment Rate for November ticked higher to 2.1% vs. 2.0% prior, while the

Seasonally adjusted unemployment rate remained unchanged at 2.1% vs. 2.2%

ожидалось.

Уровень безработицы в Швейцарии

The US Challenger

Job Cuts for November increased to 45.51K vs. 36.84K prior. Compared to the

same month last year, job cuts are down by roughly 41% but then again there was

an exceptional number of tech layoffs in November of 2022. The 45.51K layoffs

last month brings the year-to-date total to 686,860 and that’s roughly a 115%

increase to the year-to-date total for last year through to November.

Сокращение рабочих мест в Challenger США

The US Jobless

Claims beat expectations across the board:

- Initial Claims 220K

vs. 222K expected and 219K prior (revised from 218K). - Продолжающиеся претензии

1861K vs. 1910K expected and 1925K prior (revised from 1927K).

Заявки на пособие по безработице в США

BoC’s Gravelle

acknowledged the progress on inflation:

- Gravelle noted that

housing imbalances have serious consequences for shelter price inflation,

contributing 1.8 percentage points to the total October inflation rate of

3.1%. - Emphasized the need

for Canada to have more homes and a housing supply that is more responsive

to increases in demand. - Pointed out that a

jump in demographic demand, coupled with existing structural supply

issues, could explain why rent inflation continues to climb. - Stressed the

importance of all levels of government working together on housing

policies to boost supply. - Urged the reduction

of barriers to adding capacity and ensuring market flexibility to meet

future changes in housing demand. - Warned that without

more house building, inflationary pressures in the shelter sector could

continue to build. - Highlighted that

rent inflation reached a 40-year high in October, with housing supply not

keeping pace with recent increases in immigration. - Reported that

housing activity grew 8.3% in Q3 but remains far below the level needed to

meet growing housing needs. - Commented that

recent increases in immigration have boosted near-term consumption but

haven’t significantly affected inflation. - Noted that the

economy is now roughly in balance, with a focus on monitoring inflation

expectations, wage growth, and corporate pricing behaviour. - Stressed the

importance of indicators in assessing whether inflation is on a sustained

path to the 2% target. - Said that the market

has been relatively right on their previous two or three decisions, so it

seems like it’s taking in the data in the same way they are.

BoC’s Gravelle

The Japanese Average Cash Earnings increased in

October on a year-over-year basis marking the 22nd месяц подряд

of rising wages:

- Average Cash

Earnings Y/Y 1.5% vs. 0.6% prior (revised from 1.2%). - Реальная заработная плата г/г -2.3%.

Средняя денежная прибыль Японии (г/г)

The US NFP report beat expectations across the board

by a big margin:

- NFP 199K vs. 180K

expected and 150K prior. - Two-month net

revision -35K vs -101K prior. - Уровень безработицы 3.7%

vs. 3.9% expected and 3.9% prior. - Уровень участия 62.8% против 62.7% ранее.

- U6 underemployment

rate 7.0% vs. 7.2% prior. - средний почасовой

earnings M/M 0.4% vs. 0.3% expected and 0.2% prior. - средний почасовой

earnings Y/Y 4.0% vs. 4.1% expected and 4.0% prior (revised from 4.1%). - Среднее количество рабочих часов в неделю

34.4 vs. 34.3 expected and 34.3 prior. - Change in private

payrolls 150K vs. 153K expected. - изменение

manufacturing payrolls 28K vs. 30K expected. - Household survey 747K

vs. -348K prior. - Birth-death

adjustment 4K vs. 412K prior.

Уровень безработицы в США

Главными событиями следующей недели станут:

- вторник: Japan PPI, UK Labour Market report, NFIB Small

Business Optimism Index, US CPI. - Wednesday: UK GDP, Eurozone Industrial Production, US PPI, FOMC

Policy Decision, New Zealand GDP. - четверг: Australia Labour Market report, SNB Policy Decision,

BoE Policy Decision, ECB Policy Decision, US Retail Sales, US Jobless Claims,

New Zealand Manufacturing PMI. - пятница: Australia/Japan/Eurozone/UK/US Flash PMIs, China

Industrial Production and Retail Sales, Eurozone Wage data, US Industrial

Production, PBoC MLF.

Вот и все, ребята. Хороших выходных!

- SEO-контент и PR-распределение. Получите усиление сегодня.

- PlatoData.Network Вертикальный генеративный ИИ. Расширьте возможности себя. Доступ здесь.

- ПлатонАйСтрим. Интеллект Web3. Расширение знаний. Доступ здесь.

- ПлатонЭСГ. Углерод, чистые технологии, Энергия, Окружающая среда, Солнечная, Управление отходами. Доступ здесь.

- ПлатонЗдоровье. Биотехнологии и клинические исследования. Доступ здесь.

- Источник: https://www.forexlive.com/news/weekly-market-recap-04-08-december-20231208/

- :имеет

- :является

- :нет

- :куда

- $UP

- 1

- 18k

- 2%

- 2% Инфляция

- 2021

- 2022

- 2024

- 2025

- 220K

- 26

- 30

- 35%

- 36

- 4k

- 50

- 500

- 51

- 52

- 53

- 58

- 60

- 7

- 8

- 9

- a

- О нас

- выше

- Достигать

- достигнутый

- достижение

- достижение

- признанный

- через

- деятельность

- добавить

- Отрегулированный

- Регулировка

- автоматическая обработка данных

- влиять на

- пострадавших

- После

- снова

- против

- совокупный

- впереди

- Все

- позволять

- причислены

- Несмотря на то, что

- Среди

- an

- и

- годовой

- любой

- все

- прикладной

- подхода

- соответствующий

- МЫ

- ПЛОЩАДЬ

- возникать

- около

- AS

- оценить

- Оценка

- оценки;

- предполагается,

- At

- Австралия

- австралийский

- в среднем

- назад

- со спинкой

- БЕЙЛИ

- Баланс

- Банка

- барьеры

- основа

- BE

- бить

- становиться

- было

- начало

- поведение

- ниже

- польза

- Ставки

- между

- большой

- доска

- Банка Канады

- Банк Англии

- Банк Японии

- повышение

- Повышенный

- изоферменты печени

- Приносит

- широко

- строить

- Строительство

- бизнес

- но

- by

- призывают

- пришел

- CAN

- Канада

- Пропускная способность

- тщательный

- Наличный расчёт

- центральный

- Центральный банк

- уверенность

- претендент

- сложные

- изменение

- менялась

- изменения

- Китай

- китайский

- Выберите

- требования

- явно

- подниматься

- Закрыть

- тесно

- как

- Комментарии

- Компании

- сравненный

- Условия

- доверие

- последовательный

- Последствия

- принимая во внимание

- последовательный

- потребитель

- потребление

- продолжать

- продолжающийся

- продолжается

- продолжающийся

- содействие

- Основные

- базовая инфляция

- Корпоративное

- может

- Совет

- соединенный

- индекс потребительских цен

- создание

- валюты

- Валюта

- Текущий

- Порез

- сокращение

- цикл

- данным

- Декабрь

- решение

- решения

- определенный

- дефляционный

- Спрос

- демографический

- зависеть

- зависимый

- определение

- события

- DID

- трудный

- do

- Доллар

- домашняя дела

- сделанный

- Голубиная

- вниз

- рисует

- управляемый

- два

- Рано

- Заработок

- простота

- ослабление

- легко

- ЕЦБ

- Политическое решение ЕЦБ

- - подтверждает ее слова

- Экономические

- экономику

- эффект

- эффекты

- возвышенный

- сотрудников

- поощрение

- конец

- окончание

- достаточно

- обеспечивать

- обеспечение

- установить

- Евро

- Еврозона

- Даже

- развивается

- исключительный

- избыток

- существующий

- Выход

- ожидания

- ожидаемый

- Объяснять

- эксплицитно

- экспорт

- чрезвычайно

- факторы

- Осень

- далеко

- Рассказы

- финансовый

- Финансовые институты

- Финансовый рынок

- финансовая стабильность

- Компаний

- Flash

- Трансформируемость

- Фокус

- FOMC

- Что касается

- Форс-мажор

- Форекс

- Валютные рынки

- от

- далее

- будущее

- ВВП

- получить

- Глобальный

- Глобальная экономика

- хорошо

- товары

- Правительство

- Губернатор

- правительство

- большой

- выросли

- Рост

- Рост

- Случай

- Есть

- убежище

- Ястреб

- повышенный

- ее

- здесь

- High

- высший

- основной момент

- Поход

- Hikes

- его

- Дома

- ЧАСЫ

- Вилла / Бунгало

- домашнее хозяйство

- домохозяйства

- жилье

- Как

- Однако

- HTTPS

- идея

- if

- иммиграция

- Влияние

- Импортировать

- значение

- важную

- улучшать

- улучшается

- in

- включают

- В том числе

- Увеличение

- расширились

- Увеличивает

- повышение

- индекс

- Индикаторные

- индикаторы

- промышленность

- Промышленное производство

- инфляция

- Инфляционные ожидания

- уровень инфляции

- инфляционный

- Инфляционное давление

- информация

- учреждения

- интерес

- УРОВЕНЬ ИНТЕРЕСА

- Процентные ставки

- в

- вопросы

- IT

- ЕГО

- Япония

- Япония PPI

- Японии

- Японский

- работа

- сокращение рабочих мест

- заявки на пособие по безработице

- JPG

- Прыгать

- всего

- Сохранить

- хранение

- Труда

- Фамилия

- В прошлом году

- последний

- увольнениям

- оставил

- Меньше

- уровень

- уровни

- такое как

- Вероятно

- Ограниченный

- линия

- линий

- ll

- дольше

- ниже

- сделанный

- в основном

- поддерживать

- сделать

- производство

- многих

- Маржа

- рынок

- движение рынка

- Отчет о рынке

- Области применения:

- маркировка

- Май..

- значить

- меры

- Встречайте

- заседания

- встретивший

- может быть

- против

- пропущенный

- МФ

- умеренному

- монетарный

- денежно-кредитная политика

- Мониторинг

- Месяц

- ежемесячно

- месяцев

- БОЛЕЕ

- самых

- в основном

- двигаться

- движется

- много

- должен

- Возле

- Необходимость

- необходимый

- потребности

- отрицательный

- переговоры

- сеть

- Нейтральные

- Новые

- Новая Зеландия

- ВВП Новой Зеландии

- Индекс деловой активности в производственном секторе Новой Зеландии

- Новости

- следующий

- Следующая неделя

- НЛП

- хороший

- нет

- отметил,

- Ноябрь

- сейчас

- номер

- наблюдается

- октябрь

- of

- on

- консолидировать

- только

- отверстия

- оптимизм

- or

- заказы

- Другое

- наши

- внешний

- за

- всю ночь

- Темп

- выплачен

- мимо

- путь

- терпеливо

- ОПЛАТИТЬ

- Платежные ведомости

- PBOC

- МФ НБК

- процент

- Платон

- Платон Интеллектуальные данные

- ПлатонДанные

- PMI

- пунктов

- сборах

- политика

- положительный

- возможность

- дюйм

- (например,

- предыдущий

- цена

- Цены

- цены

- Предварительный

- частная

- процедуры

- Процедуры

- Производство

- Прогресс

- обеспечивать

- толкнул

- Q1

- Q3

- вопрос

- самый быстрый

- быстро

- повышение

- привлечение

- ассортимент

- Обменный курс

- Оценить поход

- повышение рейтинга

- Стоимость

- скорее

- RBA

- достигать

- достиг

- достигнув результата

- Читать

- Reading

- подтвердил

- реальные

- разумный

- резюме

- получила

- последний

- спад

- Я выздоровела

- снижение

- снижение

- по

- относительно

- оставаться

- остались

- остатки

- замечательный

- Аренда

- отчету

- обязательный

- резерв

- упругий

- отзывчивый

- ограничение

- розничный

- Розничные продажи

- возвращают

- возвращение

- Возвращает

- возвращаться

- правую

- Рост

- Встает

- повышение

- рисках,

- грубо

- s

- главная

- то же

- видел

- сообщили

- Наука

- сектор

- посмотреть

- видя

- кажется

- видел

- сентябрь

- серьезный

- Услуги

- Приют

- краткосрочный

- достопримечательность

- существенно

- Признаки

- с

- ситуация

- медленной

- Помедленнее

- замедляет

- небольшой

- меньше

- СНБ

- So

- в некотором роде

- конкретный

- Расходы

- весна

- Стабильность

- стабильный

- Этап

- позиция

- Область

- неуклонно

- устойчивый

- Шаг

- По-прежнему

- раздражитель

- стресс

- сильнее

- структурный

- достаточный

- предлагать

- Предлагает

- поставка

- Спрос и предложение

- поддержка

- Поддержанный

- сюрприз

- Опрос

- комфортного

- устойчиво

- устойчивый

- Швейцария

- система

- T

- с

- цель

- направлены

- технологии

- чем

- который

- Ассоциация

- их

- тогда

- Там.

- они

- этой

- В этом году

- мысль

- три

- Через

- затягивание

- время

- сроки

- синхронизация

- в

- вместе

- Токио

- Токийский ИПЦ

- TONE

- слишком

- инструменты

- Всего

- к

- трек

- трансформация

- переход

- тенденция

- правда

- два

- Uk

- ВВП Великобритании

- рынок труда Великобритании

- Неопределенный

- неопределенности

- под

- подкреплять

- безработица

- уровень безработицы

- вряд ли

- до

- Обновление ПО

- на

- us

- ИПЦ США

- Доллар США

- вакансии в США

- Заявки на пособие по безработице в США

- NFP США

- США PPI

- Розничные продажи в США

- обычный

- Ve

- победа

- голосование

- vs

- заработная плата

- заработная плата

- хочет

- законопроект

- наблюдение

- Путь..

- we

- Погода

- неделя

- еженедельно

- Что

- когда

- будь то

- , которые

- в то время как

- все

- зачем

- широкий

- Широкий диапазон

- будете

- без

- Работа

- работает

- бы

- Неправильно

- год

- лет

- еще

- являетесь

- Зеландию

- зефирнет

- нуль