An often repeated experience on my journey has been that one thing leads to another, which leads to another and so it goes. You may have a hunch about what these may add up to - but seldom a very clear picture or a plan. So get going - and start with what many need often (preferably same logic, user experience and tool) at home and at work - and keep adding less frequently needed features. Lessons learned: Overplanning is dangerous. Economy of repetition and economy of trust are powerful levers. And what is more important than levers - in heavy lifting.

First about the ladders & platform metafora. Ladders have steps (called rungs) - here new services that make it possible and interesting to take the next step. The two rails can be made strong by using materials like trust, habit, generic tools, convenience for builders and users, productivity improvements, security, legislation, economy of scale, economy of scope etc. The materials will typically strengthen further when they are used in many ladders.

After a while you reach a higher platform where you can start constructing new ladders to the next platform - and so it has gone - and continues to go.

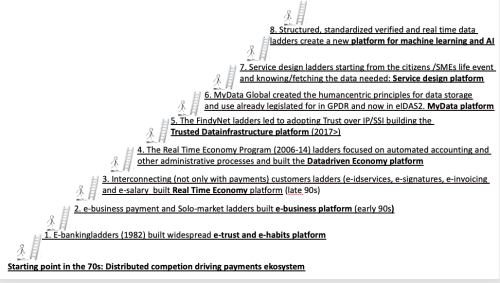

The starting point in the 70s in Finland was a decentralised and standardised payment ecosystem that furthered strong competition between the banks. The strong technology orientation and standardisation traditions also helped.

It was thus a rather natural step to use the telecom infrastructure for PC-banking services in the early 80s and gradually add all banking services to the menus - including e-signing of loans. These rather long e-banking ladders created a very important e-trust and e-habit (1st) platform. Lessons learned: Could be done before Internet. Lessons learned: Economy of repetition, economy of reuse

This was the base for the next ladder - containing rungs like account-to-account real time e-commerce payments and the Solo-market place (connecting buyers and sellers). It built an e-Business (2nd) platform in the early 90s. The rails contained e-banking, the same payment habit, cost efficiency by economy of reusing existing payment system, real time delivery of payments and full risk elimination for merchants. Lessons learned: Economy of reuse, economy of real time

The next ladders interconnected customers also with other transactions than payments. Such steps as e-identification, e-signing documents, e-invoicing and e-salary building a Real Time Economy (3rd) platform in the late 90s. Reusing the banking login credentials and the trust created for third parties interacting was an important achievement here. Today this bank-IDservice is used some 50 times per adult person in Finland – possibly even more in Sweden. Lessons learned: Economy of trust, economy of reause, economy of scope. No state operated tool needed. e-banking has to be safe in any case. All banks should offer the bank codes also to unbanked - as long as they can be securely identitied.

E-invoicing started off as improving convenience as customers started to complain about having to feed in lengthy reference numbers. With e-invoicing a simple one-click acceptance was enabled for on due date payment. Then the state calculated that the full annual savings potential for incoming invoices would be 150m€, the municipalities arrived at the same 150m€ and the Federation for Industry to 2800m€. Even if some claimed that this is an understatement - on a European level it equals some 250bn - it for sure is big enough – especially as it should be a major element to make the Single Market more single… at the latest with the corporate factwallets. Lessons learned: You can stumble upon massive producivity improvement when improvin convenience. Banks are the natural distributers for consumer invoices and also for sending especially SME invoices and payment requests.

The rails and steps in this ladder thus contained very strong business cases for both parties in a transaction – and also the economy of trust and repetition.

The next ladders were using the private-public Real Time Economy program (2006-14) to drive e-invoicing also on EUscale, automation of accounting, digital procurement procedures, salary administration, VAT-reporting and e-receipts. Once the productivity aspects of using data not only for automation but also for decision making became clear the level reached was named Datadriven Economy (4th) platform. Lesson learned: The accounting industry is not driving change in the same way as banks. High time to shape up as a part of the Trust Infrastructure.

The work to drive progress on 4th platform took us to the vision of global e-invoicing. When sending payments to any bank customer in the world without the 25 000 or so banks having to sign contracts between themselves is possible - why not also sending invoices? This multilateral structure based on having to follow the rules related to being a member of the not-for-profit SWIFT cooperative should be reusable – and also allow non-banks to join for new services. It did not happen even if we managed to get both e-invoicing and the Real Time Economy on the EU-Commission agenda.

So, we had to witness how cumbersome it was to get interoperability between e-invoice service providers even in EU and keep looking for the next way forward.

We then found new elements for the ladders – https://trustoverip.org and Self-Sovereign Identity in the www.Findy.fi ladders with rungs like life event driven service design, global standards, general-purpose interoperable wallets, e-IDAS2 legislation. This is taking us to the Trusted Datainfrastructure (5th) Platform. Lesson learned: Miraculous things can happen

A short description of the ladders being built (started in 2017) – in so many directions – by so many – goes as follows:

The data rights holder (see Digital Governance Act and GDPR art 20) has the right to know where her/his data is and get all of it – especially important is the identity building verified data – including identification credentials - in use. In practice it means getting it downloaded from the data source data wallet to her/his own factwallet (eIDAS IDwallet term is not as suitable as it may lead to thinking that the wallets only handling identification) and then have the right to choose which service provider is the best for solving the service needing at hand.

The 3 parties involved do not have to be technically integrated, as the typically national infrastructure layer (the Findynets) will handle the DID-layers. The amount of friction in the economy, risks, crime and grey economy this will eliminate and how much it will add privacy and convenience is unbelievable.

While the Findyconsortium was starting up https://mydata.org was established. It is now operating in 40 countries and its human-centric paradigm aims making sharing of personal data based on trust and a balanced relationship between individual and organizations. Make data sharing happen for better services and productivity and making it right. MyData built the ladders to the MyData (6th) Platform

As use of personal data is now already mandatory and the wallets and infrastructure (data highway) and needed governance are being delivered service design should now start from the citizen’s or SME’s context (life event). What data is needed, where is it, how can it be accessed (wallet to wallet) and how can the data rights holder freely choose who can use the data to solve the need at hand (usecases galore..). This platform is thus called the New Service Design (7th) Platform.

The next ladders will deliver My and Big Data that is structured, more standardized, verified and available in real time on its birth. Pretty easy to see that the quality, energy efficiency and transparence of machine learning and AI will improve radically. This is the Machine Learning and AI (8th) Platform.

And the next ladders are for sure being built already. The materials for these rails have been tested and improved in all previous ladders and platforms. So if the big picture is made into a narrative by generalists the experts can keep working and the demand will be there as the next steps appear.

- SEO Powered Content & PR Distribution. Get Amplified Today.

- Platoblockchain. Web3 Metaverse Intelligence. Knowledge Amplified. Access Here.

- Source: https://www.finextra.com/blogposting/23508/my-e-journey---over-40-years-part-6-ladders-galore?utm_medium=rssfinextra&utm_source=finextrablogs

- 000

- 2017

- a

- About

- acceptance

- accessed

- Accounting

- achievement

- Act

- administration

- Adult

- agenda

- AI

- aims

- All

- already

- amount

- and

- and infrastructure

- annual

- Another

- appear

- Art

- aspects

- Automation

- available

- Bank

- Banking

- Banks

- base

- based

- before

- being

- BEST

- Better

- between

- Big

- Big Data

- Big Picture

- Bo

- both parties

- builders

- Building

- built

- business

- buyers

- calculated

- called

- case

- cases

- change

- Choose

- claimed

- clear

- competition

- Connecting

- constructing

- consumer

- context

- continues

- contracts

- convenience

- cooperative

- Corporate

- Cost

- could

- countries

- created

- Credentials

- Crime

- customer

- Customers

- Dangerous

- data

- data sharing

- Date

- decentralised

- decision

- Decision Making

- deliver

- delivered

- delivery

- Demand

- description

- Design

- DID

- digital

- documents

- drive

- driven

- driving

- e-commerce

- Early

- economy

- efficiency

- elements

- eliminate

- enabled

- energy

- energy efficiency

- enough

- Equals

- especially

- established

- etc

- Ether (ETH)

- EU

- eu-commission

- European

- Even

- Event

- existing

- experience

- experts

- Features

- Federation

- Finextra

- Finland

- follow

- follows

- Forward

- found

- frequently

- friction

- from

- full

- further

- GDPR

- general-purpose

- get

- getting

- Global

- Go

- Goes

- going

- governance

- gradually

- handle

- Handling

- happen

- having

- helped

- here

- High

- Highway

- holder

- Home

- How

- HTTPS

- Identification

- Identity

- image

- important

- improve

- improved

- improvement

- improvements

- improving

- in

- Including

- Incoming

- individual

- industry

- Infrastructure

- integrated

- interacting

- interconnected

- interesting

- Internet

- Interoperability

- interoperable

- involved

- IT

- join

- journey

- Keep

- Know

- ladder

- Late

- latest

- layer

- lead

- Leads

- learned

- learning

- Legislation

- lesson

- Lessons

- Lessons Learned

- Level

- Life

- lifting

- Loans

- Long

- looking

- machine

- machine learning

- made

- make

- Making

- managed

- mandatory

- many

- Market

- massive

- materials

- means

- member

- Merchants

- more

- multilateral

- Municipalities

- NARRATIVE

- Natural

- Need

- needed

- needing

- New

- next

- numbers

- offer

- ONE

- operated

- operating

- organizations

- paradigm

- part

- parties

- payment

- payment system

- payments

- person

- personal

- personal data

- picture

- Place

- plan

- platform

- Platforms

- plato

- Plato Data Intelligence

- PlatoData

- Point

- possible

- potential

- powerful

- practice

- pretty

- previous

- privacy

- procedures

- productivity

- Program

- Progress

- provider

- providers

- quality

- radically

- rails

- reach

- reached

- real

- real-time

- related

- relationship

- repeated

- requests

- reusable

- rights

- Risk

- risks

- rules

- safe

- salary

- same

- Savings

- Scale

- scope

- securely

- security

- Sellers

- sending

- service

- Service Provider

- service providers

- Services

- Shape

- sharing

- Short

- should

- sign

- Simple

- single

- SME

- So

- SOLVE

- Solving

- some

- Source

- standards

- start

- started

- Starting

- State

- Step

- Steps

- Strengthen

- strong

- structure

- structured

- suitable

- Sweden

- SWIFT

- system

- Take

- taking

- Technology

- telecom

- The

- The State

- the world

- themselves

- things

- Thinking

- Third

- third parties

- time

- times

- to

- today

- tool

- tools

- transaction

- Transactions

- Trust

- typically

- unbanked

- us

- use

- User

- User Experience

- users

- verified

- vision

- Wallet

- Wallets

- What

- which

- while

- WHO

- will

- without

- witness

- Work

- working

- world

- would

- years

- zephyrnet