Click here to browse our Real Estate Agent Directory and contact top-rated agents in your area!

If you want to apply for a mortgage to buy a house, you will need to know your credit score. Your lender will ask about this score during the pre-qualification process and will confirm your estimate during the pre-approval and formal application steps. Many lenders have minimum credit score thresholds for approving loans, and a high credit score can also reduce your interest rate. Essentially, the lower your interest rate, the less money you will give to the bank and the more money you will keep in your pocket.

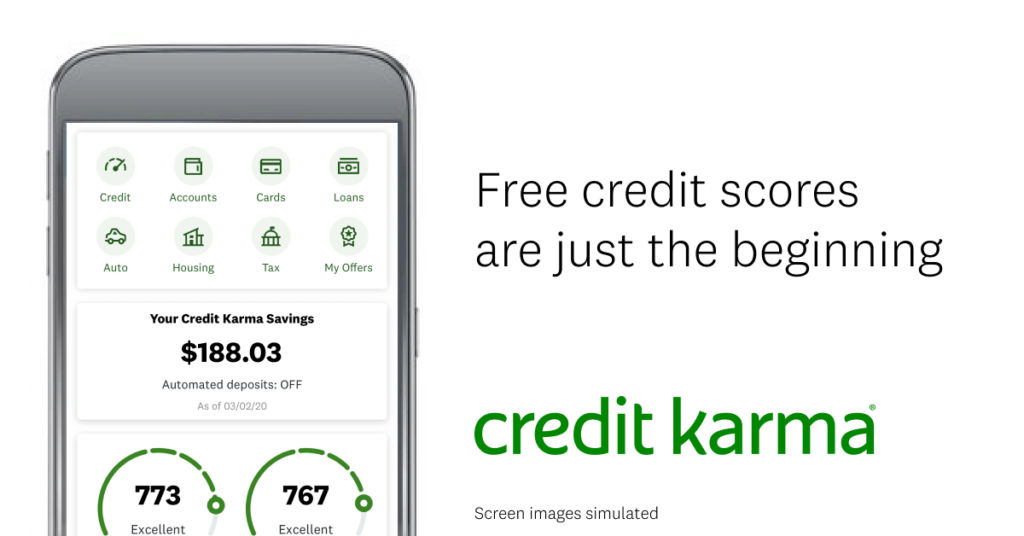

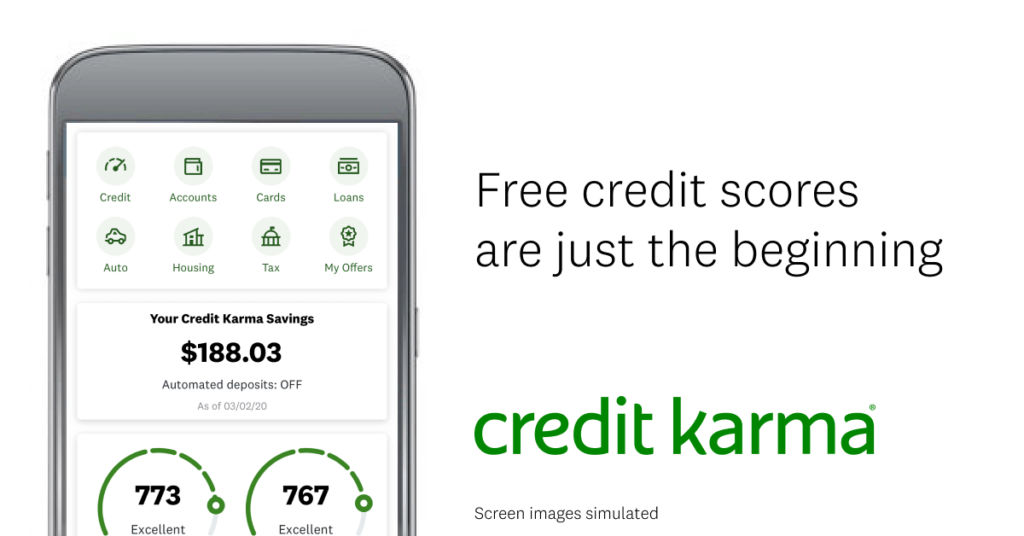

One of the most popular sites for checking credit scores is Credit Karma. Not only does this website promise a free credit score, but it also provides a variety of financial services if you need to build yours up. Is Credit Karma accurate? Should you trust this website and its reports? Learn more about this brand and the role credit scores play in the home-buying process.

How does Credit Karma report credit scores?

Before you can answer how accurate is Credit Karma, it helps to develop an understanding of how the company works. This business pulls information from the three major credit bureaus: Equifax, Transunion, and Experian. These three organizations track a variety of data points related to your personal finance. For example, if you made all of your student loan payments on time last year, this positive data is recorded in your credit history. If you missed a credit card payment, that negative point is also recorded.

>> AGENT ANSWERS: Should I wait to increase my credit score before buying a house?

Your credit score isn’t a hidden number that you can’t see. Many credit card issuers (like Discover and Mastercard) offer free credit reports to customers each month. You also have a right to pull your credit report from any of these agencies. Credit Karma offers a weekly credit report by requesting soft inquiries of your credit from the three major credit bureaus.

Is Credit Karma accurate? For the most part, yes. The company doesn’t use its own algorithm to determine credit scores, it simply reports what the three major credit bureaus send it. While your score might change from one week to the next, you can trust that the reports you receive reflect your current state of credit.

Will checking my credit hurt my score?

There’s a common belief that you shouldn’t check your credit score too often, or else it will start to drop. This is only half-true. Too many hard inquiries into your credit can drop the score. However, soft inquiries cost you nothing.

What is the difference? A hard inquiry is a formal request into your credit history from a lender or other financial institution. When you formally start the mortgage application process, your lender will conduct a hard inquiry into your finances. One or two hard inquiries won’t harm your credit score – this is because taking out loans and financing is part of life. People buy houses, purchase cars, and take out student loans in order to improve their finances, lives, and careers.

However, if you have several hard inquiries over the course of a year, they could start to impact your finances. It could mean that banks are denying you loans or that you are taking on more debt than you can handle.

A soft inquiry is a light check into your credit score that doesn’t affect your credit at all. This is what Credit Karma pulls. The existence of a soft inquiry is why you can receive weekly reports from this organization without risking your credit – it’s not a hard pull.

Don’t be afraid of checking your credit score. Knowing your score is a powerful tool for navigating the financial world and securing the loans and interest rates that you deserve.

Is Credit Karma really free?

The next question that most people have after, “Is my Credit Karma score accurate,” is whether or not this service is really free. Yes, it is free for customers to request credit scores from this organization.

There’s a saying in marketing that if you aren’t the customer, you are the product. This is the case with Credit Karma. The company wants to collect your information in order to send your targeted messages on relevant products you can use. For example, if you have a lower than desired credit score because of your credit card debt, then the company might recommend a credit card issuer that allows you to consolidate your debt. If you sign up for a card through this company, Credit Karma receives a commission on the sale.

This doesn’t mean that the information shouldn’t be trusted. Credit Karma will still try to recommend the best possible credit cards, loans, and services to improve your financial standing. However, it helps to know that opting for any of these services helps the company stay in business.

Meanwhile, it is in Credit Karma’s best interest to keep offering free credit scores and other products to users. The more value people get out of the Credit Karma suite of free products, the greater the user base will grow and the greater the number of customers the company can market its affiliates to.

Does Credit Karma report my FICO score?

No, the free credit report you receive from Credit Karma will not reflect your FICO score. FICO is a separate organization that offers its own credit score data. While FICO scores offer a decent picture of your credit, it isn’t the report used by most lenders and banking institutions.

The score you receive comes from the VantageScore 3.0 scoring model. This model was developed through a collaboration of the major credit bureaus (Equifax, TransUnion, and Experian). Your VantageScore is the one your lender will look at when evaluating your mortgage application.

You can trust the Credit Karma report even if the numbers differ slightly from your FICO score. Both scores reflect the same metrics of payment history, debt-to-income ratio, and overall financial health.

Why do my scores differ across the three credit bureaus?

When you receive your credit score, you might notice slight discrepancies between the three credit bureaus. This is normal. Each credit bureau pulls data in a different way and at a different time. For example, if you pay your credit card bill on the first day of the month, one bureau might pull its report the day before you paid your bill while another pulls its report the day after. This could create slightly different numbers as a result of your paid-off debt.

Check your report to make sure your scores all fall within a similar range – and stay that way from one report to the next. You only need to be concerned if you notice major differences in the reports (for example, an Experian report of 750 and a TransUnion report of 525). There could be something wrong with the reporting or an issue with your credit that hasn’t been caught yet.

>> AGENT ANSWERS: First time home buyer with bad credit?

While weekly credit checks and long-term reporting can give you a clear idea of your credit, focus on big trends, not minor changes. An increase or decrease of a few points won’t matter from one credit bureau to the next but a big change over several months is a red flag.

What credit score do you need to get a mortgage?

When it comes to applying for a mortgage, the higher your credit score, the lower your interest rates will likely be. However, there are also minimum thresholds that companies look for in regard to different loans.

First, the minimum credit score you need to buy a house is 620. However, this is often the lowest bar. Of all the mortgage loans approved every year, the majority have scores above 650.

However, if you are interested in an FHA loan, you might be able to get approved with a credit score of around 500. These loans are meant for first-time homebuyers who don’t have a large down payment or savings. Applicants might not have a long financial history, which leads to a lower credit score.

If you want a Jumbo loan or want favorable interest rates, try to apply for a mortgage with a score above 700. The best interest rates are usually given to applicants with credit scores above 740.

There are always options if you have a poor credit score – or simply want to build it up. You can create a plan now to grow your score over the next year before you buy a house.

Turn to FastExpert When You Are Ready to Buy a House

Touring houses and dreaming about your future home is fun, but you need a clear picture of your financial state before this part can begin. Is Credit Karma accurate? Yes, and it can be a valuable tool to learn about your options. Before you decide to buy a house, gather your financial documents and get a clear idea of your credit score, estimated down payment, debt-to-income ratio, and budget. This will streamline the mortgage process and help you get approved.

Once you have your finances in order, turn to FastExpert to find a Realtor in your area. We curate the top real estate agents from across the country to help you narrow down your search. Rankings can’t be bought with FastExpert, which means you only see the best agents based on performance. Try us today and start your home-buying journey.

- SEO Powered Content & PR Distribution. Get Amplified Today.

- PlatoAiStream. Web3 Data Intelligence. Knowledge Amplified. Access Here.

- Minting the Future w Adryenn Ashley. Access Here.

- Buy and Sell Shares in PRE-IPO Companies with PREIPO®. Access Here.

- Source: https://www.fastexpert.com/blog/is-credit-karma-accurate/

- :is

- :not

- $UP

- 500

- a

- Able

- About

- above

- accurate

- across

- affect

- affiliates

- afraid

- After

- agencies

- Agent

- agents

- algorithm

- All

- allows

- also

- always

- an

- and

- Another

- answer

- answers

- any

- applicants

- Application

- Apply

- Applying

- approved

- ARE

- AREA

- around

- AS

- At

- Bad

- Bank

- Banking

- Banks

- bar

- base

- based

- BE

- because

- been

- before

- begin

- belief

- BEST

- between

- Big

- Bill

- both

- bought

- brand

- budget

- build

- Bureau

- business

- but

- buy

- Buying

- by

- CAN

- card

- Cards

- careers

- cars

- case

- caught

- change

- Changes

- check

- checking

- Checks

- clear

- collaboration

- collect

- comes

- commission

- Common

- Companies

- company

- concerned

- Conduct

- Confirm

- consolidate

- contact

- Cost

- could

- country

- course

- create

- credit

- credit card

- Credit Cards

- Credit Karma

- Current

- Current state

- customer

- Customers

- data

- day

- Debt

- decide

- decrease

- deserve

- desired

- Determine

- develop

- developed

- differ

- difference

- differences

- different

- discover

- do

- documents

- does

- Doesn’t

- Dont

- down

- Drop

- during

- each

- Equifax

- essentially

- estate

- estimate

- estimated

- Ether (ETH)

- evaluating

- Even

- Every

- example

- Experian

- Fall

- few

- FICO

- finance

- Finances

- financial

- financial health

- financial history

- financial institution

- financial services

- financing

- Find

- First

- Focus

- For

- formal

- Formally

- Free

- from

- fun

- future

- gather

- get

- Give

- given

- greater

- Grow

- handle

- Hard

- harm

- Have

- Health

- help

- helps

- here

- Hidden

- High

- higher

- history

- Home

- House

- houses

- How

- However

- HTTPS

- Hurt

- i

- idea

- if

- Impact

- improve

- in

- Increase

- information

- Inquiries

- inquiry

- Institution

- institutions

- interest

- INTEREST RATE

- Interest Rates

- interested

- into

- issue

- Issuer

- issuers

- IT

- ITS

- journey

- jpg

- Karma

- Keep

- Know

- Knowing

- large

- Last

- Last Year

- Leads

- LEARN

- lender

- lenders

- less

- Life

- light

- like

- likely

- Lives

- loan

- Loans

- Long

- long-term

- Look

- lowest

- made

- major

- Majority

- make

- many

- Market

- Marketing

- mastercard

- Matter

- mean

- means

- meant

- messages

- Metrics

- might

- minimum

- minor

- model

- money

- Month

- months

- more

- Mortgage

- most

- Most Popular

- navigating

- Need

- negative

- next

- normal

- nothing

- Notice..

- now

- number

- numbers

- of

- offer

- offering

- Offers

- often

- on

- ONE

- only

- Options

- or

- order

- organization

- organizations

- Other

- our

- out

- over

- overall

- own

- paid

- part

- Pay

- payment

- payments

- People

- performance

- personal

- Personal Finance

- PHP

- picture

- plan

- plato

- Plato Data Intelligence

- PlatoData

- Play

- Point

- points

- poor

- Popular

- positive

- possible

- powerful

- process

- Product

- Products

- promise

- provides

- Pulls

- purchase

- question

- range

- Rate

- Rates

- ratio

- ready

- real

- real estate

- really

- realtor

- receive

- receives

- recommend

- recorded

- Red

- reduce

- reflect

- regard

- related

- relevant

- report

- Reporting

- Reports

- request

- result

- risking

- Role

- sale

- same

- Savings

- saying

- score

- scoring

- Search

- securing

- see

- send

- separate

- service

- Services

- several

- should

- sign

- similar

- simply

- Sites

- slightly different

- Soft

- something

- start

- State

- stay

- Steps

- Still

- streamline

- Student

- suite

- Take

- taking

- targeted

- than

- that

- The

- the information

- their

- then

- There.

- These

- they

- this

- three

- Through

- time

- to

- today

- too

- tool

- Transunion

- Trends

- Trust

- trusted

- try

- TURN

- two

- understanding

- us

- use

- used

- User

- users

- usually

- Valuable

- value

- variety

- wait

- want

- wants

- was

- Way..

- we

- Website

- week

- weekly

- What

- when

- whether

- which

- while

- WHO

- why

- will

- with

- within

- without

- works

- world

- Wrong

- year

- yet

- you

- Your

- zephyrnet