Soitec is a semiconductor materials company known for its smart cut and Silicon on Insulator (SOI) technologies, which are critical in 5G, Silicon Photonics, and Silicon Carbide (EV) end-markets.

Yesterday, they announced that current CEO Paul Boudre will retire and be replaced by Pierre Barnabé in July of 2022. Barnabé is currently an SVP at Atos, a French IT consulting company. This seemingly routine CEO transition sank company shares by over 15%. It’s not what it seems.

First, the entire existing management team is opposed. The management team sent a letter to the board that does not mince words. Translated to English, it reads:

Soitec’s Management Committee deplores the takeover of Soitec by the Chairman of the Board of Directors for 3 years, which culminates today with the incomprehensible appointment of a new CEO.

What exactly is happening at Soitec? Well first let’s just start with the current story of the now outgoing CEO, Paul Boudre.

The Story of Soitec (and Paul Boudre)

Soitec, like most firms, was no overnight success. This timeline of the companies history is the best place to start. Soitec originally pursued other markets but failed to gain traction. In 2015, the company Soitec shuttered its solar business as part of a hard pivot away from its existing failures.

The situation was dire. The company had more debt than the value of its market capitalization.

In January of 2015, with shares trading at measly $200 million market capitalization, Paul Boudre was appointed CEO. Paul initially joined the company from KLA as an Executive VP in Sales before transitioning to COO in 2008. Drastic changes were needed.

In the midst of significant layoffs in the solar division, a hefty financing package company to keep the company afloat, Paul focused the company on SOI and made it what it is today.

The details of the turnaround are unimportant, but the results today speak for themselves: Soitec now boasts a ~$5.8B market capitalization (~29x higher than the start of his tenure) and has 4x+ annual revenue. This is a legendary turnaround that will surely be sung of in Semiconductor Valhalla.

At the age of 63, Paul is approaching retirement. Given such a track record, one imagines a thoughtful process involving existing management, not the overnight skullduggery that actually occurred. Further, the new CEO candidate has no experience in the semiconductor field. Why did the board choose newcomer Pierre Barnabé over other qualified internal candidates?

To answer this, we need to learn about the Chairman of the Board.

Enter Eric Meurice (and Pierre)

Eric Meurice is best known as the former CEO of ASML. In 2013 Eric was appointed Chairman of the board of ASML after 8 years of being CEO. Note the exact lanaguage of the Chairman announcement.

Eric Meurice will be Chairman of ASML Holding and act as adviser to the new leadership and the Supervisory Board until the end of his contract on 31 March 2014, ensuring a smooth and comprehensive transition of critical tasks and processes, customer contacts and relations with strategic suppliers.

The current CEO gets the job during Eric Meurice’s contract and Mr. Meurice gets bumped to Chairman. It’s pretty customary for the outgoing CEO to spend time as the current Chairman. It’s less customary to not have the contract renewed. Despite European CEOs having shorter tenures, this is atypical.

As the former CEO of ASML, Eric Meurice is now an ideal candidate for board memberships. Here’s a list of the few boards he’s been a part of.

Let’s hone in on Eric’s stint at Soitec. Eric Meurice joined the board of Soitec in 2018 as the chair of the Nomination Committee. The committee was tasked with nominating a new Chairman, so else does Eric Meurice nominate but himself?

Eric, overqualified as he is, gets the job. But that’s not enough. In 2019, he picks up two more important roles as the Chair of the Strategic Committee and Chair of the Compensation Committee. He now holds both the keys to the kingdom and to its treasury.

Joining a company, becoming the Chairman of the Board, and then taking on additional roles as the head of the Compensation and Strategic Committees fit into the typical model of a high-powered executive. That’s standard.

How does the French Government fit into Eric’s rise to power?

Eric Meurice’s Extraordinary Actions

Let’s look at the specific actions Eric Meurice took that prompted significant backlash from the executive committee. In the executive committee letter, they listed out a few specific complaints that were (importantly) falsifiable. Their (translated) list of grievances is as follows:

- Takeover of the interim compensation committee that has become definitive, creating an omnipresence in all committees and at the head of several committees

- Interference in social dialogue without consultation with management.

- Double language regarding the opposition of management on the implementation of PAT (Action Plan for All) in 2021.

- Establishment of internal regulations granting exceptionally extensive powers to the Chairman of the Board of Directors and establishing the keys to his takeover.

- Alteration of evidence in the context of the investigation of a governance drift.

- Intimidation, vexatious practices towards members of the Executive Committee.

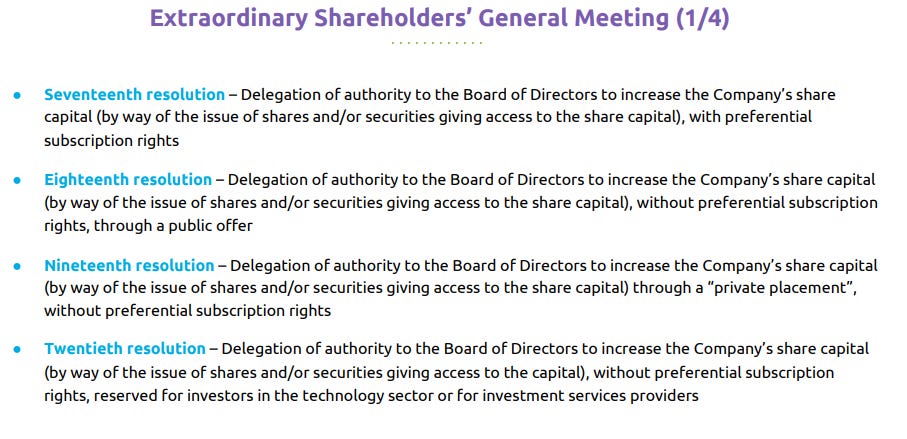

The board granted itself extensive power through a list of resolutions added to the typical bylaws of the company at the so-called “extraordinary shareholders general meeting”. It’s rare to see an extraordinary resolution, so it’s outright mind-boggling to see 35 resolutions. This is one of the broadest power grabs I’ve ever seen. Let’s consider a few of the resolutions.

The resolutions are technical, but the gist of them is that the board now has a whole set of new powers that are usually reserved for the CFO. They can issue shares, buy back shares, decide who gets shares, and all of these powers are directly granted to the board. This creates extraordinary power to the board and the people on it.

This explains why they had 3 CFOs since the extraordinary resolutions began. Remy Pierre was replaced in September 2019 by Sébastien Rouge who was replaced one year later by Lea Alzingre. That’s high turnover for the job.

Maybe these resolutions could be kosher, but the reason they are not is all the extraordinary resolutions are new for Soitec. Take 2017 for example, when there were only 6 plain resolutions. Something has changed.

But besides the mundane extraordinary powers of resolutions given to the board, there’s more at play. I now want to focus on the executive committee complaint around the compensation board because this is where the other players (France) start to enter the scene.

Board Power Politics

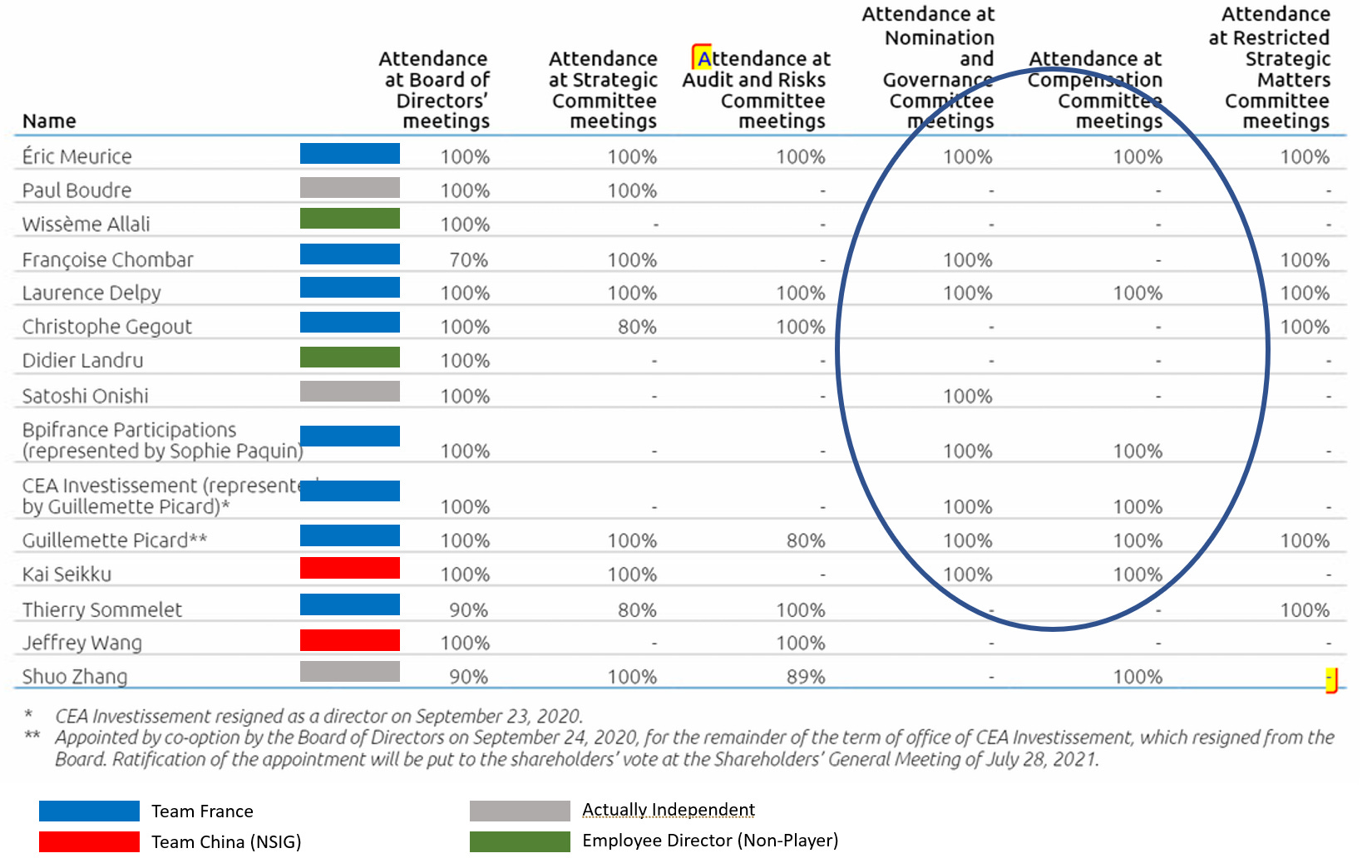

Let’s talk about the composition of the board. The board power politics make sense when you can see who is sits on what board committees. There are 5 board committees in Soitec, and the restricted strategic meeting is an ad-hoc group for acquisitions or other events. So that means there are really 4 standing committees and 1 ad-hoc committee. They are the Strategic Committee, the Audit Committee, the Nomination Committee, and the Compensation Committee.

These committees are filled with 14 members, many of them are supposed to be independent. This breaks down with further examination as many of the “independents” are clearly affiliated with the French Government. Now let’s start with chairs of the five committees.

Eric Meurice is the Chairman of the Board, Chair of the Compensation Committee (most powerful committee), and the Chair of the Strategic Committee.

Laurence Delpy is Chair of the Nomination Committee, the chair that Eric Meurice previously held before he became Chairman of the Board. She’s independent, yet she sits on all 5 committees.

Lastly, Christophe Gegout is chair of the Audit and Risk Committees. He’s supposed to be an independent member, but he used to work for CEA aka the large French consortium with a meaningful stake in Soitec. He doesn’t work there anymore, but they’re clearly playing fast and loose with the definition of the word “independent”.

Let’s look at the actual composition of the committees and identify 1) who is in what committee and 2) which committees matter. I made a simple graphic based on the filing with a legend that explains where everyone’s allegiances lie. In order of importance, it’s the Compensation, the Nomination, the Strategic & Restricted Strategic, and lastly the Audit committee. I broadly categorized the board members into the 4 “teams”, aka Team France, Team China, Independent, and Employee Directors. Note the legend in the picture below.

Let’s start backward. The green team is employee directors and is part of a movement to get labor union leaders on the board so employees have more say in the company writ large. For the sake of this analysis, I consider them non-players, as this is their first year on the board, and they don’t sit on committees.

Next is the team “actually independent”. Note that Satoshi Onishi works for Shin-Etsu, so he’s independent as in he’s representing his company’s JV with Soitec. He is not a big player. In Shuo Zhang’s case, I cannot make any meaningful connections to anyone else. Paul Boudre of course is the outgoing CEO. Notice that he does not sit on any important committees.

That brings me to Team China. Team China is the NSIG (National Silicon Industry Group) block, which invested 14.5% at the time which now is diluted to 10.34% stake (this is lower now) into Soitec in May 2016. NSIG, like many large Chinese firms, is an extension of the CCP. They hold two seats that I represent in Red. Kai Seikku is actually sitting on the powerful committees, aka the nomination and compensation committees. But importantly Jeffrey Wang has been pushed out to the not-important audit committee.

Last is Team France. With the exception of Francoise Chombar, they are all French Nationals. I put Francoise Chombar on Team France because she shares a board with Eric Meurice at Umicore, so I assume she’s on his team.

Everyone else either works for CEA (French Alternative Energies and Atomic Energy Commission) or Bpifrance (French Public Investment Bank), formerly worked there, or suspiciously looks connected (Laurence Delpy is clearly important but I have no links other than she worked at Alcatel Lucent where Pierre is from). Thierry Sommelet works at Bpifrance for example.

Importantly Team France consists of 6 out of 8 members of both of the most powerful Nomination and Compensation committees. And everyone else who is not affiliated with Team France conveniently sits outside of these boards with the exception of Kai Seikku, who represents the powerful ~10.34% share block from NSIG. Team France is clearly in control here, and the BPI and CEA seats are permanent, with rotating members but consistent committees.

What I’m trying to say is that Soitec’s board is controlled board by a very small number of players, all of which can be linked to France. Obviously, these members want to protect the interests of France, and what’s more most of the moves taken by the board pre-date Eric’s arrival. So it’s clearly not Eric in charge, but rather the representatives of France that are driving this bus!

What’s France Got to Do With It?

When I first started down the rabbit hole of the Eric Meurice takeover I thought the motivation was pretty simple. Ousted CEO Eric Meurice was looking for another kingdom to rule and found it in the form of Soitec. A clear power play, as highlighted by the management letter. After all, we knew he already had ambitions to sit in the CEO seat again, per this ST Micro rumor. In a series of successive moves, he rose from Director to Chairman, and he pushed his way to the top.

There are a few problems with that theory and it comes in two bold flavors. First, the year (July 2018) that Eric Meurice got appointed to the board as a director was the first year of expanded extraordinary resolutions. The previous year it went from 8 total resolutions to whopping 23 new resolutions. So the expanded board powers actually pre-date Eric’s arrival on the board. Eric Meurice was just the conduit for the control of the board.

The second thing was this extremely crucial disclosure about a standstill agreement with NSIG that made clued me in that something else was happening. When NSIG (National Silicon Industry Group aka China) bought the 14.5% stake in Soitec, they agreed to a standstill agreement on the shares.

The standstill agreement is an agreement at the time so that NSIG (China) didn’t continue to raise their stake in Soitec and effectively take over the company. It’s a takeover provision that stopped their large influence from increasing. The French board members were clearly aware of this.

But that standstill agreement ended on June 7, 2019, which was 1 year after Eric’s rise to power. This explains why he entered when he did. However, this tidbit made everything become clear(er) regarding the resolutions.

Should NSIG Sunrise S.à.r.l acquire shares in the Company before the expiration of the Shareholders’ Agreement at the close of the Shareholders’ General Meeting called to approve the financial statements for the fiscal year ended March 31, 2021, it would lose its rights relating to the Company’s governance

Team France knew they needed to lock down the company from a governance standpoint before March 31, 2021, or risk further influence from NSIG aka China. And Eric Meurice was the perfect man for the job. Win-win.

Besides Paul Boudre was ready to go. He terminated a paused employment contract so that the company wouldn’t have to pay him a termination fee, and they rewarded him with an incentive (I find this weird). He clearly signaled he was on the way out. Readers of the filings could have spotted his retirement as early as 2020, it was just the executive team that was blindsided.

But that brings us to what really happened. France Nationalized Soitec through a series of board moves, just in time before the Chinese government could push for more control. The CEO put in place is just a placeholder for the board.

National Champions Need Nationalization

How are we surprised that France wanted to nationalize Soitec?! This is France we are talking about here! It’s clear that there’s a vested interest in keeping Soitec French-controlled. The expanded board powers also expanded government influence over Soitec. Soitec has effectively become a State Owned Controlled Enterprise.

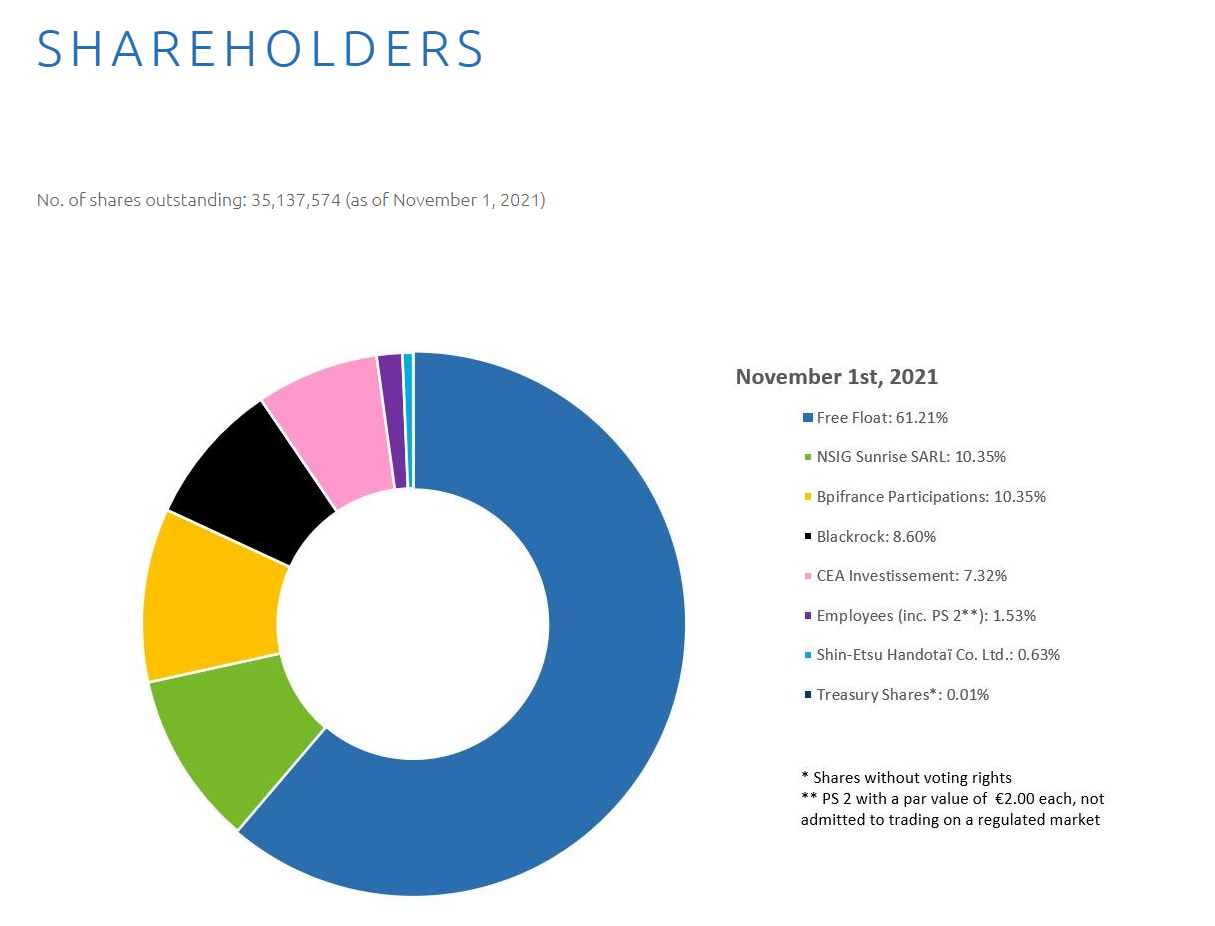

Look at the shareholder base. The ~17.67% French-controlled block was large, but not completely dominant given the large NSIG (aka China) block. A Chinese takeover of France’s semiconductor star would be devastating (not to mention embarrassing). Team France could not let this happen.

All of the board actions in conjunction means that this was likely premeditated by the controlling shareholders – the state of France – to further control Soitec. Paul’s retirement was just the catalyst to push the changes that have already been made ahead. So what about our underqualified CEO candidate, Pierre Barnabe?

The thing that I found really curious was that Pierre is on the board of INRIA, or the Institute for Research in Computer Science and Automation. It’s a government lead entity that’s core purpose is to further France’s technology interests. From the French National control lens, Pierre is a perfect CEO.

So now France effectively owns Soitec. What are they going to do with it? Paul left the company on a strong financial note and Soitec is a springboard for other national pursuits, like manufacturing Silicon Carbide. Manufacturing Silicon Carbide would be terrible for Soitec the business, but great for France’s national ambitions.

Another likely option is that the board can use its expanded powers to purchase a fab in Europe, which would be perfect given Soitec produces wafers. Now France produces wafers and chips! There is a small design team within Soitec, and expanding that could also further French national interests. That’s a full stack semiconductor company with just 2 additional acquisitions.

All of this makes sense in the now geopolitically driven world of semiconductors. As of late, there have been multiple announcements for new mega-fabs, like the Intel Ohio fab or the new TSMC Japan fab. Every country is doing what it can to shore up its semiconductor businesses, and France couldn’t let China steal their national champion.

Conclusions and Questions

Soitec is effectively nationalized through board control. It makes sense given that China had a window to push for control, so instead, France just took the whole thing. France, Soitec’s largest shareholder, put everyone in a place of power in order to achieve this. What looked like a power-hungry move by a single actor, Eric Meurice, really was a coordinated win-win to control the company for France.

While I’m sure Soitec’s nationalization will be disappointing for free-market capitalists (where they at?), it’s not surprising at all given the current semiconductor climate. It’s a de facto-controlled company now. The takeaway: national-level politics continue to matter in the semiconductor industry. This theme is not going to go away any time soon. Soitec is just the latest and greatest in the series. Goodbye Soitec, Hello French National Semiconductor company.

There are some loose ends. How does NSIG feel about this? Did Paul Boudre know about any of this? There are a lot of other interesting threads in this entire story, but it’s clear what happened. France nationalized their largest semiconductor company!

If you enjoyed this piece, please consider subscribing. Even the free tier gets occasional posts. I try to write about semiconductor companies broadly from an investment perspective, so this investigative journalism is a bit different.

Oh by the way if you are either a past ASML employee during Eric’s time at ASML or a current Soitec employee who would love to talk, you can reach me at Doug@fabricatedknowledge.com.

Some Unfinished Business

I wanted to discuss parts of the story that didn’t flow well with the rest of the power politics at Soitec. The question I presume most people would be wondering is about Pierre Barnabe. Why is he not qualified again?

I really had a problem with this statement from Soitec management.

He draws upon a remarkable track record that includes a threefold revenue increase at the Atos Big Data and Cybersecurity division in the space of a few years, in a highly competitive market requiring deep cooperation with the ecosystem.

Part of that three-fold growth was 38 acquisitions along the way. Is that execution or is that just buying three times more revenue? And also the stock and business are horrid. It’s down 63% over the last 5 years and revenue growth is tepid at best.

Oh, and STMicroelectronics has a deep bench of French National semiconductor executives that would have made a perfect fit. Given Pierres in with the government, Pierre definitely did not get the job on the basis of merit.

What about Paul Boudre?

One of the weirdest side exits is Paul Boudre. By voluntarily abdicating his contract agreement and then getting paid to do so, I think Paul had wind of changes but didn’t care as he knew he was on the way out. And even if Paul did want to change things, he was locked out of the committees that matter (compensation and nomination). He wouldn’t be privy to what happened anyways.

I think the biggest blindside is the executive committee. I get why their reaction is so strong, but I think their outrage of Paul’s replacement and the lack of internal promotion is missing the bigger national interest story in what they thought would be a routine succession. The COO likely expected promotion, and other executives in turn would be promoted to COO. I feel bad for them, as it’s frustrating to not be a part of the company they clearly helped build.

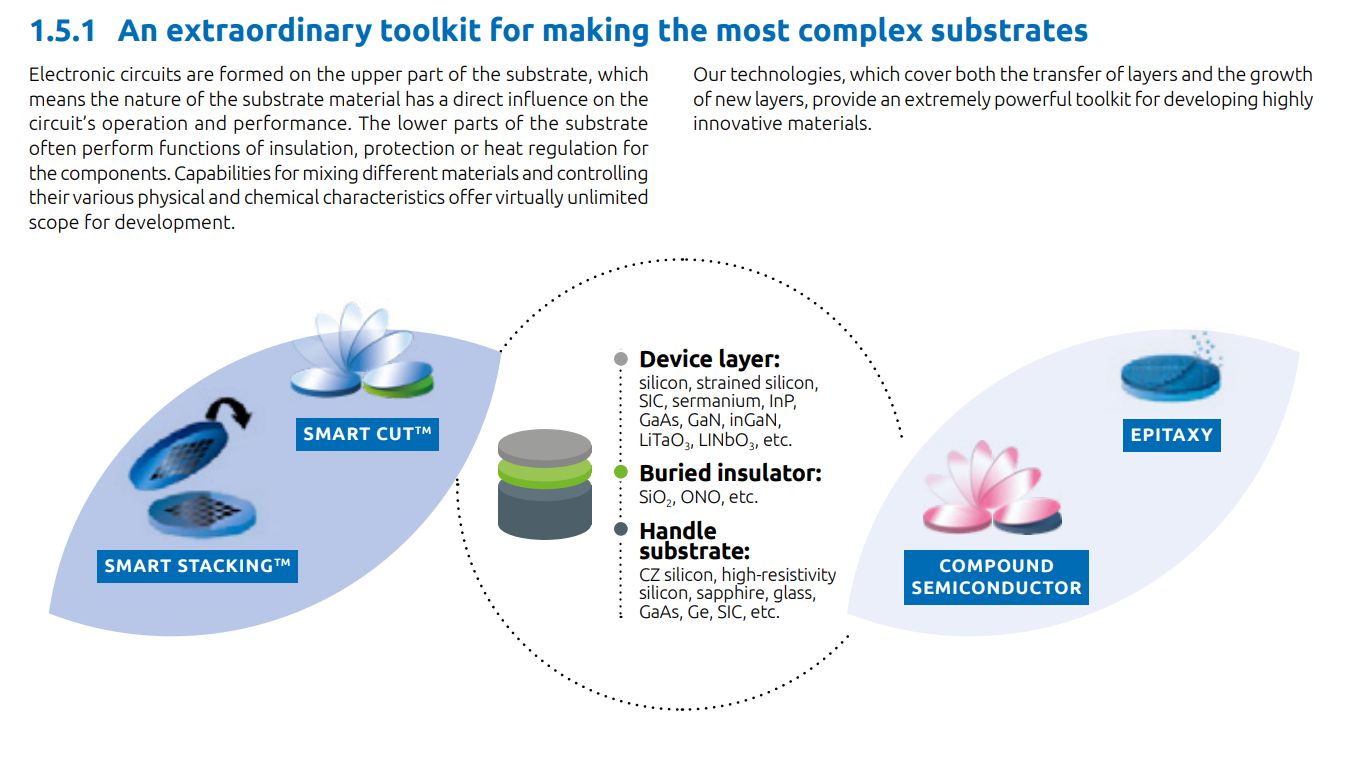

Appendix: A bit more on SOI

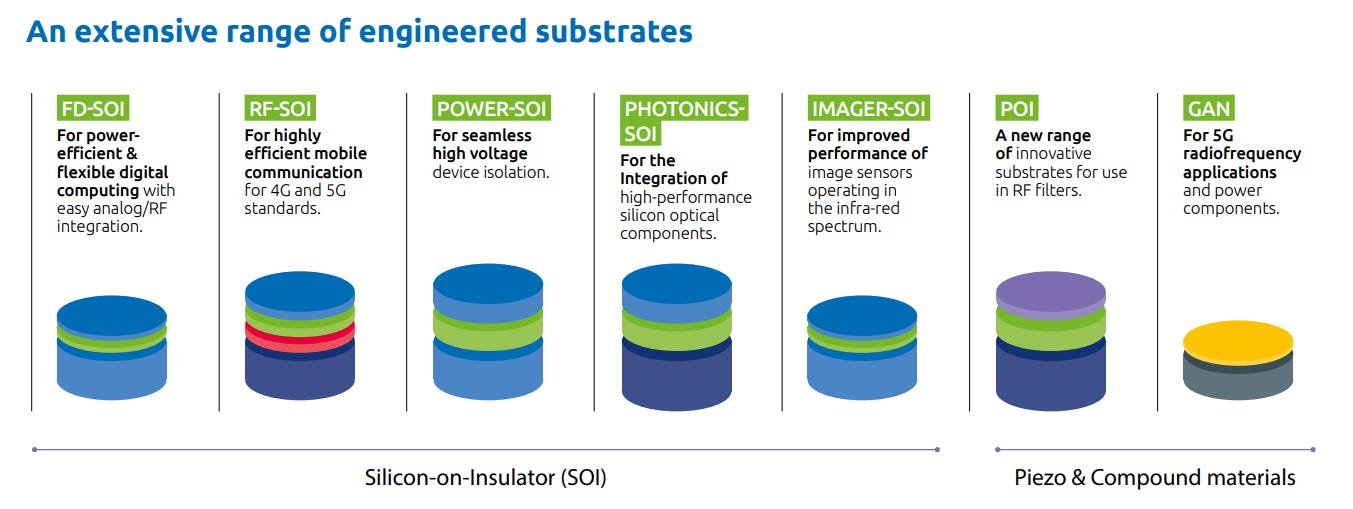

Silicon on Insulator is a technology that embeds the insulator below the surface of silicon. Usually, this is done via Ion implantation, a “smart cut” and a flip of the substrate so that the buried insulator is now below a device layer. This improves overall performance meaningfully.

Soitec is the only volume manufacturer in the world, and their competitors license their technology. Soitec believes that their market share in SOI wafers is ~77% globally.

Subscribe to Fabricated Knowledge

Share this post via: Source: https://semiwiki.com/semiconductor-services/fabricated-knowledge/306953-how-frances-largest-semiconductor-company-got-stolen-in-plain-sight/- &

- 2016

- 2019

- 2020

- 2021

- 2022

- 5G

- 7

- About

- acquisitions

- Act

- Action

- actions

- Additional

- Agreement

- All

- already

- analysis

- announced

- Announcement

- Announcements

- around

- audit

- Automation

- Bank

- being

- believes

- BEST

- Biggest

- Billion

- Bit

- Bloomberg

- board

- board of directors

- boasts

- build

- business

- businesses

- buy

- Buying

- capitalization

- care

- ccp

- ceo

- cfo

- chairman

- change

- charge

- China

- chinese

- commission

- Companies

- company

- Compensation

- competitors

- complaints

- computer science

- Connections

- consulting

- continue

- contract

- coo

- could

- Creating

- critical

- CrunchBase

- Current

- data

- Debt

- Design

- device

- DID

- different

- Director

- discuss

- Doesn’t

- down

- driven

- driving

- during

- Early

- ecosystem

- employees

- employment

- ends

- energy

- English

- Enterprise

- Euro

- Europe

- EV

- events

- example

- execution

- executive

- executives

- expanding

- experience

- FAST

- financial

- First

- fit

- flow

- Focus

- focused

- form

- found

- France

- Free

- French

- full

- General

- getting

- Giving

- Globally

- going

- good

- governance

- Government

- great

- Green

- Group

- Growth

- having

- head

- here

- High

- Highlighted

- hold

- How

- HTTPS

- identify

- important

- Increase

- industry

- influence

- Inria

- Intel

- interest

- interests

- investigation

- investment

- IT

- January

- Japan

- Job

- joined

- journalism

- July

- keeping

- keys

- labor

- language

- large

- latest

- layoffs

- lead

- Leadership

- LEARN

- legendary

- License

- List

- looked

- looking

- love

- man

- management

- Manufacturer

- manufacturing

- March

- Market

- Market Capitalization

- Markets

- materials

- Matter

- Members

- million

- model

- more

- most

- move

- moves

- National

- needed

- Nominate

- Ohio

- opposition

- Option

- order

- Other

- Pay

- People

- performance

- perspective

- picture

- piece

- Pierre

- Pivot

- Play

- player

- players

- politics

- Posts

- power

- powerful

- pretty

- price

- Problem

- process

- processes

- promotion

- protect

- public

- purchase

- question

- raise

- reaction

- readers

- record

- regulations

- research

- REST

- Results

- retirement

- revenue

- Risk

- sales

- Science

- semiconductor

- Semiconductors

- sense

- Series

- set

- Share

- shareholder

- Shares

- significant

- Simple

- small

- smart

- So

- Social

- solar

- something

- Space

- spend

- stake

- start

- started

- State

- Statement

- stock

- stolen

- Story

- Strategic

- strong

- success

- suppliers

- Surface

- Talk

- talking

- Technical

- Technologies

- Technology

- the world

- theme

- thought

- Through

- time

- today

- top

- track

- Trading

- treasury

- union

- us

- usually

- value

- volume

- What

- WHO

- wind

- within

- without

- words

- Work

- worked

- works

- world

- would

- year

- years