Wzmocnienie następnej iteracji Consumer Finance

Medium, JC Bahr-de Stefano | 31 marca 2023 r

Building the next decade of consumer finance

- Last week in Las Vegas, I had the great pleasure of moderating a panel at Fintech Meetup re: building the next decade of consumer finance by leveraging real-time data and cash flow forecasting. I wanted to share some of the key insights shared during the session by our amazing panelists, Jose Bethancourt (Co-Founder of Metoda finansowa), Ema Rouf (Co-Founder of Pave.dev), and Zane Salim (Co-Founder of Atlas)!

Zobacz: CFPB wysyła prośbę o udzielenie informacji na temat „brokerów danych”

- 1/ Alternative data augments FICO across the entire credit spectrum — this is about FICO+ NOT replacing FICO.

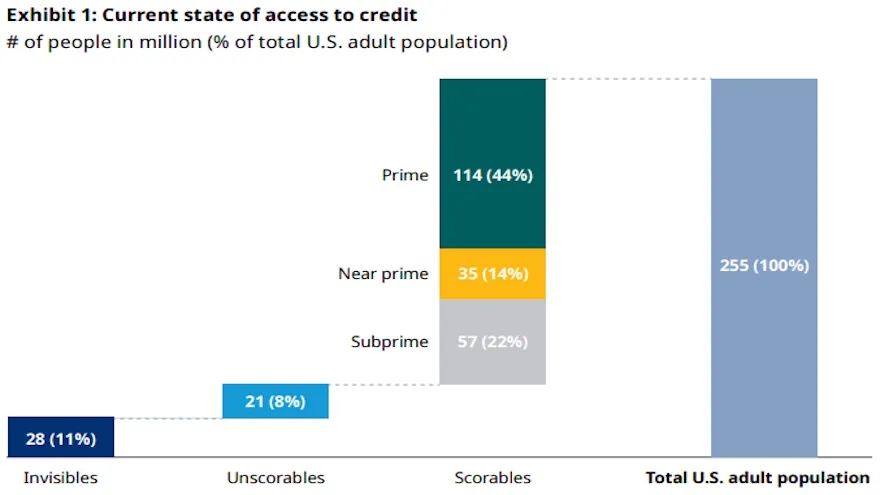

- Połączenia problem of credit invisibility in the US is growing, with an estimated 28 million adult Americans credit invisible and 21 million unscorable. To make decisions about these consumers and offer them financial services and products, alternative data, such as income and employment, can be used. This data can also help lenders make better risk-weighted decisions for many segments of users, not just credit invisible ones, and is particularly important during periods of economic stress.

- 2/ Real time data powers better products and outcomes by enabling greater access and improving the quality of risk management.

- Credit bureaus can take up to 45 days to report data, so lenders may not have the most up-to-date information on a borrower’s behavior. Atlas, a payroll-powered credit card, uses real-time data to monitor users’ financial health and adjust credit limits, allowing for better risk management and loss prevention.

- 3/ The movement to make alternative data mainstream has to happen outside of the credit bureaus.

- Credit reports do not provide a complete view of a consumer’s debt obligations as there is a lot of data that is not furnished to the credit bureaus, including most BNPL loans. However, companies like Method collect data from over 60k institutions to provide lenders with a more comprehensive view of a person’s debt obligations, combining data from credit bureaus with financial institutions’ core banking systems.

Zobacz: Kanada's Open Banking Journey: Wywiad z Abe Kararem, dyrektorem ds. produktów w Fintech Galaxy

- 4/ Recent innovation in infrastructure has made this data far more accessible than it has been in the past.

- Recent advancements in infrastructure and tools have made it easier to access and enrich the data. Companies such as Method and Pave are providing infrastructure that helps fintechs and banks adopt and use this data, leading to accelerated adoption.

- 5/ Mature lenders don’t want scores, they want raw data or attributes.

- Understanding the data is crucial for them to explain it to originating banks or capital providers, and the use of attribute generation can speed up model development. Pave is an example of a company offering transaction cleaning, enrichment, and their own attributes toolbox for lenders to use in their proprietary models.

Przejdź do pełnego artykułu -> tutaj

Połączenia National Crowdfunding & Fintech Association (NCFA Canada) to ekosystem innowacji finansowych, który zapewnia edukację, wywiad rynkowy, zarządzanie branżą, możliwości tworzenia sieci i finansowania oraz usługi tysiącom członków społeczności i ściśle współpracuje z przemysłem, rządem, partnerami i podmiotami stowarzyszonymi w celu stworzenia dynamicznej i innowacyjnej technologii i finansowania przemysł w Kanadzie. Zdecentralizowana i rozproszona NCFA współpracuje z globalnymi interesariuszami i pomaga w inkubacji projektów i inwestycji w sektorach fintech, alternatywnych finansów, finansowania społecznościowego, finansów peer-to-peer, płatności, aktywów i tokenów cyfrowych, blockchain, kryptowaluty, regtech i sektorów insurtech. Dołącz do rejestru Kanadyjska społeczność Fintech & Funding dzisiaj ZA DARMO! Lub zostań członek wnoszący wkład i zdobądź profity. Aby uzyskać więcej informacji prosimy odwiedzić: www.ncfacanada.org

Połączenia National Crowdfunding & Fintech Association (NCFA Canada) to ekosystem innowacji finansowych, który zapewnia edukację, wywiad rynkowy, zarządzanie branżą, możliwości tworzenia sieci i finansowania oraz usługi tysiącom członków społeczności i ściśle współpracuje z przemysłem, rządem, partnerami i podmiotami stowarzyszonymi w celu stworzenia dynamicznej i innowacyjnej technologii i finansowania przemysł w Kanadzie. Zdecentralizowana i rozproszona NCFA współpracuje z globalnymi interesariuszami i pomaga w inkubacji projektów i inwestycji w sektorach fintech, alternatywnych finansów, finansowania społecznościowego, finansów peer-to-peer, płatności, aktywów i tokenów cyfrowych, blockchain, kryptowaluty, regtech i sektorów insurtech. Dołącz do rejestru Kanadyjska społeczność Fintech & Funding dzisiaj ZA DARMO! Lub zostań członek wnoszący wkład i zdobądź profity. Aby uzyskać więcej informacji prosimy odwiedzić: www.ncfacanada.org

Chcesz uzyskać dostęp od wewnątrz do niektórych z najbardziej innowacyjnych postępów w #fintech. Zarejestruj się na #FFCON23 i posłuchaj światowych liderów myśli, co dalej! Kliknij poniżej, aby uzyskać bilety otwartego dostępu do wszystkich wirtualnych programów i treści na żądanie z FFCON23.

Wesprzyj NCFA, obserwując nas na Twitterze!

|

Podobne posty

- Dystrybucja treści i PR oparta na SEO. Uzyskaj wzmocnienie już dziś.

- Platoblockchain. Web3 Inteligencja Metaverse. Wzmocniona wiedza. Dostęp tutaj.

- Źródło: https://ncfacanada.org/empowering-the-next-iteration-of-consumer-finance/

- :Jest

- $W GÓRĘ

- 10

- 100

- 2018

- 28

- 39

- a

- O nas

- przyśpieszony

- dostęp

- dostępny

- w poprzek

- przyjąć

- Przyjęcie

- Dorosły

- postępy

- zaliczki

- Spółki stowarzyszone

- AI / ML

- Wszystkie kategorie

- Pozwalać

- alternatywny

- alternatywne finansowanie

- zdumiewający

- Amerykanie

- i

- kwiecień

- SĄ

- artykuł

- AS

- Aktywa

- At

- atlas

- atrybuty

- Bankowość

- Systemy bankowe

- Banki

- BD

- BE

- stają się

- poniżej

- Ulepsz Swój

- blockchain

- rozszerzenie BNPL

- pożyczający

- Budowanie

- by

- Pamięć podręczna

- CAN

- Kanada

- kapitał

- karta

- Gotówka

- Przepływy pieniężne

- Kategoria

- CFPB

- szef

- dyrektor ds. produktu

- Sprzątanie

- kliknij

- dokładnie

- Współzałożyciel

- zbierać

- COM

- łączenie

- społeczność

- Firmy

- sukcesy firma

- kompletny

- wszechstronny

- konsument

- Finanse konsumenckie

- Konsumenci

- zawartość

- rdzeń

- Podstawowa działalność

- Stwórz

- kredyt

- Karta kredytowa

- Crowdfunding

- kryptowaluta

- dane

- Dni

- Dług

- dekada

- Zdecentralizowane

- Decyzje

- Kreowanie

- oprogramowania

- cyfrowy

- Zasoby cyfrowe

- dystrybuowane

- nie

- podczas

- łatwiej

- Gospodarczy

- Ekosystem

- Edukacja

- EMA

- zatrudnienie

- uprawniającej

- umożliwiając

- zaangażowany

- wzbogacać

- Cały

- wejście

- szacunkowa

- Eter (ETH)

- wydarzenia

- przykład

- Wyjaśniać

- Fico

- finansować

- budżetowy

- kondycja finansowa

- włączenie finansowe

- innowacje finansowe

- Instytucje finansowe

- usługi finansowe

- FINTECH

- Galaktyka Fintechowa

- fintechy

- pływ

- następujący

- W razie zamówieenia projektu

- od

- pełny

- Finansowanie

- możliwości finansowania

- Galaktyka

- generacja

- otrzymać

- Globalne

- Rząd

- wspaniały

- większy

- GV

- zdarzyć

- Wydarzenie

- Have

- Zdrowie

- słyszeć

- pomoc

- pomaga

- hi

- Jednak

- HP

- hr

- http

- HTTPS

- i

- ważny

- poprawy

- in

- Włącznie z

- włączenie

- Dochód

- przemysł

- Informacja

- Infrastruktura

- Innowacja

- Innowacyjny

- Insider

- spostrzeżenia

- instytucje

- Insurtech

- Inteligencja

- Wywiad

- inwestycja

- problemy

- IT

- iteracja

- Styczeń

- przystąpić

- podróż

- jpg

- Klawisz

- duży

- LAS

- Las Vegas

- Przywódcy

- prowadzący

- kredytodawców

- pożyczanie

- lewarowanie

- lubić

- Limity

- relacja na żywo

- Imprezy na żywo

- Kredyty

- od

- Partia

- zrobiony

- Mainstream

- robić

- i konserwacjami

- wiele

- March

- rynek

- dojrzały

- Maksymalna szerokość

- Może..

- Meetup

- członek

- Użytkownicy

- metoda

- milion

- model

- modele

- monitor

- jeszcze

- większość

- ruch

- NEO

- sieci

- Newsletter

- Następny

- więzy

- of

- oferta

- oferuje

- Oficer

- on

- Na żądanie

- Online

- koncepcja

- otwarta bankowość

- Szanse

- zewnętrzne

- własny

- płyta

- szczególnie

- wzmacniacz

- Przeszłość

- płatności

- peer to peer

- okresy

- profity

- osoba

- plato

- Analiza danych Platona

- PlatoDane

- Proszę

- przyjemność

- uprawnienia

- Zapobieganie

- Produkt

- Produkty

- Programowanie

- projektowanie

- własność

- zapewniać

- zapewnia

- że

- jakość

- Surowy

- surowe dane

- RE

- real

- w czasie rzeczywistym

- dane w czasie rzeczywistym

- niedawny

- zarejestrować

- Regtech

- raport

- Raporty

- zażądać

- Ryzyko

- Zarządzanie ryzykiem

- s

- Sektory

- Segmenty

- Usługi

- Sesja

- Share

- shared

- znak

- So

- kilka

- prędkość

- interesariusze

- Zarządzanie

- stres

- taki

- zrównoważone

- systemy

- TAG

- Brać

- że

- Połączenia

- ich

- Im

- Te

- myśl

- myśliciele

- tysiące

- bilety

- czas

- Tytuł

- do

- już dziś

- Żetony

- Toolbox

- narzędzia

- transakcja

- prawdziwy

- nowomodny

- us

- posługiwać się

- Użytkownicy

- VEGAS

- wibrujący

- Zobacz i wysłuchaj

- Wirtualny

- Odwiedzić

- poszukiwany

- tydzień

- w

- działa

- zefirnet