私の旅でしばしば繰り返される経験は、興は別のものにつながる, which leads to another and so it goes. You may have a hunch about what these may add up to - but seldom a very clear picture or a plan. So get going - and 多くの人が頻繁に必要とするものから始める (preferably same logic, user experience and tool) at home and at work - and keep adding less frequently needed features. 学んだ教訓: 過剰な計画は危険です。 繰り返しの経済と信頼の経済は強力な手段です。 と what is more important than levers - in heavy lifting.

まず、について はしごとプラットフォームのメタフォーラム. はしごにはステップがあります(と呼ばれます ラング) - here new services that make it possible and interesting to take the next step. The two レール のような材料を使用して強くすることができます 信頼、習慣、一般的なツール、ビルダーとユーザーの利便性、生産性の向上、セキュリティ、法律、規模の経済、範囲の経済など。 材料は通常、多くのはしごで使用されるとさらに強化されます。

しばらくすると、 より高いプラットフォーム where you can start constructing new ladders to the next platform - and so it has gone - and continues to go.

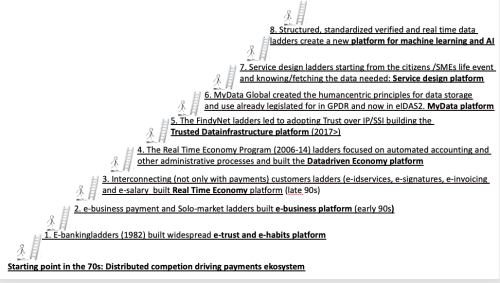

70 年代のフィンランドの出発点は、銀行間の激しい競争を促進する分散化され、標準化された支払いエコシステムでした。 強力な技術指向と標準化の伝統も助けになりました。

It was thus a rather natural step to use the telecom infrastructure for PC-banking services in the early 80s and gradually add all banking services to the menus - including e-signing of loans. These rather long e-banking ladders created a very important e-trust と e-habit (1st) プラットフォーム。 学んだ教訓: インターネットの前に行うことができます。 学んだ教訓: 繰り返しの経済、再利用の経済

This was the base for the next ladder - containing rungs like account-to-account real time e-commerce payments and the Solo-market place (connecting buyers and sellers). It built an e-Business(第2)プラットフォーム 90年代初頭。 レールには、電子バンキング、同じ支払い習慣、既存の支払いシステムを再利用する経済性によるコスト効率、支払いのリアルタイム配信、および商人の完全なリスク排除が含まれていました。 教訓: 再利用の経済性、リアルタイムの経済性

次のはしごはまた、顧客を相互接続しました 支払い以外の取引。 電子身分証明書、電子署名文書、電子請求、電子給与の構築などの手順 リアルタイム経済(第3)プラットフォーム 90年代後半。 銀行のログイン資格情報と、対話するサードパーティのために作成された信頼を再利用することは、ここで重要な成果でした. 今日、この銀行 ID サービスは、フィンランドでは成人 50 人あたり約 XNUMX 回使用されており、スウェーデンではさらに多い可能性があります。 学んだ教訓: Economy of trust, economy of reause, economy of scope. No state operated tool needed. e-banking has to be safe in any case. All banks should offer the bank codes also to unbanked - as long as they can be securely identitied.

電子インボイスは次のように始まりました 利便性の向上 as customers started to complain about having to feed in lengthy reference numbers. With e-invoicing a simple one-click acceptance was enabled for on due date payment. Then the state calculated that the full annual savings potential for incoming invoices would be 150m€, the municipalities arrived at the same 150m€ and the Federation for Industry to 2800m€. Even if some claimed that this is an understatement - on a European level it equals some 250bn - it for sure is big enough – especially as it should be a 単一市場をより単一にする主要な要素… 遅くとも企業のファクトウォレットで。 学んだ教訓: 利便性を向上させると、生産性が大幅に向上します。 銀行は、消費者の請求書、特に SME の請求書と支払い要求の送信の自然な配布者です。

このように、このはしごのレールとステップには、取引の両当事者にとって非常に強力なビジネスケースが含まれており、信頼と繰り返しの経済も含まれていました。

次のはしごは、官民のリアルタイム経済プログラム (2006-14) を使用して、EUscale での電子請求、会計の自動化、デジタル調達手順、給与管理、VAT 報告、および電子領収書を推進していました。 自動化だけでなく意思決定にもデータを使用することの生産性の側面が明らかになると、到達したレベルに名前が付けられました データドリブン エコノミー (4 番目) プラットフォーム。 教訓: T会計業界は、銀行と同じように変化を推進していません。 トラスト インフラストラクチャの一部として形成する時が来ました。

The work to drive progress on 4th platform took us to the vision of global e-invoicing. When sending payments to any bank customer in the world without the 25 000 or so banks having to sign contracts between themselves is possible - why not also sending invoices? This multilateral structure based on having to follow the rules related to being a member of the not-for-profit SWIFT cooperative should be reusable – and also allow non-banks to join for new services. It did not happen even if we managed to get both e-invoicing and the Real Time Economy on the EU-Commission agenda.

そのため、EU でも電子請求書サービス プロバイダー間の相互運用性を実現することがいかに面倒であるかを目の当たりにし、次の方法を模索し続けなければなりませんでした。

その後、はしごの新しい要素を見つけました – https://trustoverip.org と Self-Sovereign Identity www.Findy.fi ライフイベント駆動型のサービス設計、グローバル標準、汎用の相互運用可能なウォレット、e-IDAS2 法制などのラングを備えたはしご。 これにより、 信頼できるデータ インフラストラクチャ (5 番目) プラットフォーム。 学んだ教訓: 奇跡的なことが起こります

(2017 年に開始された) 非常に多くの方向で非常に多くの方法で構築されているはしごの簡単な説明は次のとおりです。

The data rights holder (see Digital Governance Act and GDPR art 20) has the right to know where her/his data is and get all of it – especially important is the identity building verified data – including identification credentials - in use. In practice it means getting it downloaded from the data source data wallet to her/his own factwallet (eIDAS IDwallet term is not as suitable as it may lead to thinking that the wallets only handling identification) and then have the right to choose which service provider is the best for solving the service needing at hand.

関係する 3 者が技術的に統合されている必要はありません。 国家インフラ層 (フィンディネット) DIDレイヤーを処理します. これにより、経済、リスク、犯罪、グレーエコノミーにおける摩擦の量が解消され、 プライバシーと利便性がどれだけ向上するかは信じられないほどです。

Findyコンソーシアムの立ち上げ時 https://mydata.org 設立された。 現在40カ国で運営されており、その人間中心のパラダイムは、個人と組織の間の信頼とバランスの取れた関係に基づいて個人データを共有することを目的としています. より良いサービスと生産性のためにデータ共有を実現し、それを正しくします。 MyData ははしごを構築しました MyData (6th) プラットフォーム

個人データの使用はすでに義務化されており、ウォレットとインフラストラクチャ (データ ハイウェイ)、および必要なガバナンスが提供されているため、サービス設計は市民または中小企業のコンテキスト (ライフ イベント) から開始する必要があります。 どのデータが必要なのか、どこにあるのか、どのようにアクセスできるのか (ウォレットからウォレットへ)、データの権利所有者は、目の前のニーズを解決するために誰がデータを使用できるかをどのように自由に選択できるのか (ユースケースは豊富です..)。 したがって、このプラットフォームは 新しいサービス デザイン (7th) プラットフォーム。

次のはしごは、構造化され、より標準化され、検証され、誕生時にリアルタイムで利用できるマイデータとビッグデータを提供します。 機械学習と AI の品質、エネルギー効率、透明性が大幅に向上することは容易に想像できます。 これは 機械学習と AI (8 番目) のプラットフォーム。

そして、次のはしごは確かにすでに建設されています。 これらのレールの素材は、以前のすべてのはしごおよびプラットフォームでテストされ、改善されています。 そのため、ジェネラリストが全体像を物語にすれば、専門家は作業を続けることができ、次のステップが現れても需要はそこにあります。

- SEO を活用したコンテンツと PR 配信。 今日増幅されます。

- Platoblockchain。 Web3メタバースインテリジェンス。 知識の増幅。 こちらからアクセスしてください。

- 情報源: https://www.finextra.com/blogposting/23508/my-e-journey---over-40-years-part-6-ladders-galore?utm_medium=rssfinextra&utm_source=finextrablogs

- 000

- 2017

- a

- 私たちについて

- 受け入れ

- アクセス

- 会計

- 達成

- 行為

- 管理

- 成人

- 議題

- AI

- 目指して

- すべて

- 既に

- 量

- &

- とインフラ

- 毎年恒例の

- 別の

- 現れる

- 宝品

- 側面

- オートメーション

- 利用できます

- 銀行

- バンキング

- 銀行

- ベース

- ベース

- さ

- BEST

- より良いです

- の間に

- ビッグ

- ビッグデータ

- 全体像

- Bo

- 両政党とも

- ビルダー

- 建物

- 内蔵

- ビジネス

- バイヤー

- 計算された

- 呼ばれます

- 場合

- 例

- 変化する

- 選択する

- 主張した

- クリア

- コンペ

- 接続する

- 構築

- consumer

- コンテキスト

- 続ける

- 契約

- 利便性

- 協同組合

- 企業

- 費用

- 可能性

- 国

- 作成した

- Credentials

- 犯罪

- 顧客

- Customers

- 危険な

- データ

- データ共有

- 日付

- 分権化された

- 決定

- 意思決定

- 配信する

- 配信

- 配達

- 需要

- 説明

- 設計

- DID

- デジタル

- ドキュメント

- ドライブ

- ドリブン

- 運転

- eコマース

- 早い

- 経済

- 効率

- 要素は

- 排除する

- 使用可能

- エネルギー

- エネルギー効率

- 十分な

- 等しいです

- 特に

- 設立

- 等

- エーテル(ETH)

- EU

- EU委員会

- 欧州言語

- さらに

- イベント

- 既存の

- 体験

- 専門家

- 特徴

- フェデレーション

- Finextra

- Finland

- 次

- フォワード

- 発見

- 頻繁に

- 摩擦

- から

- フル

- さらに

- GDPR

- 一般的用途

- 取得する

- 受け

- グローバル

- Go

- ゴエス

- 行く

- ガバナンス

- 徐々に

- ハンドル

- ハンドリング

- 起こる

- 持って

- 助けました

- こちら

- ハイ

- 高速道路

- 保有者

- ホーム

- 認定条件

- HTTPS

- 識別

- アイデンティティ

- 画像

- 重要

- 改善します

- 改善されました

- 改善

- 改善

- 改善

- in

- 含めて

- 入ってくる

- 個人

- 産業を変えます

- インフラ

- 統合された

- 相互作用

- 相互接続

- 興味深い

- インターネット

- 相互運用性(インターオペラビリティ)

- 相互運用可能な

- 関係する

- IT

- join

- 旅

- キープ

- 知っている

- はしご

- 遅く

- 最新の

- 層

- つながる

- リード

- 学んだ

- 学習

- 立法

- レッスン

- レッスン

- 教訓

- レベル

- 生活

- フェイスリフト

- ローン

- 長い

- 探して

- 機械

- 機械学習

- 製

- make

- 作成

- マネージド

- 義務的な

- 多くの

- 市場

- 大規模な

- 材料

- 手段

- メンバー

- 商人

- 他には?

- 多国間

- 自治体

- ナレラティブ

- ナチュラル

- 必要

- 必要とされる

- 必要

- 新作

- 次の

- 番号

- 提供

- ONE

- 運営

- オペレーティング

- 組織

- パラダイム

- 部

- パーティー

- 支払い

- 決済システム

- 支払い

- 人

- 個人的な

- 個人データ

- 画像

- 場所

- 計画

- プラットフォーム

- プラットフォーム

- プラトン

- プラトンデータインテリジェンス

- プラトデータ

- ポイント

- 可能

- 潜在的な

- 強力な

- 練習

- かなり

- 前

- プライバシー

- 手続き

- 生産性

- 演奏曲目

- 進捗

- プロバイダー

- プロバイダ

- 品質

- 根本的に

- レール

- リーチ

- 達した

- リアル

- への

- 関連する

- 関係

- 繰り返される

- リクエスト

- 再利用可能な

- 権利

- リスク

- リスク

- ルール

- 安全な

- 給与

- 同じ

- 貯蓄

- 規模

- スコープ

- しっかりと

- セキュリティ

- 販売

- 送信

- サービス

- サービスプロバイダー

- サービスプロバイダ

- サービス

- 形状

- シェアリング

- ショート

- すべき

- 符号

- 簡単な拡張で

- EMSの

- So

- 解決する

- 解決

- 一部

- ソース

- 規格

- start

- 開始

- 起動

- 都道府県

- 手順

- ステップ

- 強化する

- 強い

- 構造

- 構造化された

- 適当

- Sweden

- SWIFT

- 取る

- 取得

- テクノロジー

- 電気通信

- ステート

- 世界

- 自分自身

- 物事

- 考え

- 三番

- 第三者

- 時間

- <font style="vertical-align: inherit;">回数</font>

- 〜へ

- 今日

- ツール

- 豊富なツール群

- トランザクション

- 取引

- 信頼

- 一般的に

- 縛られていない

- us

- つかいます

- ユーザー

- 操作方法

- users

- 検証

- ビジョン

- 財布

- 財布

- この試験は

- which

- while

- 誰

- 意志

- 無し

- 目撃者

- 仕事

- ワーキング

- 世界

- でしょう

- 年

- ゼファーネット